by Chris Williams | Aug 3, 2026 | Blog

Before I bought System Six, I had to answer this question with my own money. I was leaving a private equity career to acquire a bookkeeping firm with an SBA loan and a personal guarantee. If AI was about to automate bookkeeping away, I was about to make the worst financial decision of my life.

So I did what buyers do: I went deep. I studied the AI bookkeeping startups. I talked to investors in some of the best-funded ones. And I bought the human bookkeeping firm anyway. Several years in, with revenue up every year since, here is the honest version of what I learned — including the parts that should worry some bookkeepers.

Everyone asks this question. I asked it during diligence.

The question is not hype-driven; it is rational. Bookkeeping looks like exactly the kind of work AI should eat: repetitive, rules-based, digital. And a wave of venture-backed startups raised hundreds of millions of dollars saying precisely that.

What I found when I looked under the hood was different from the marketing.

What happened to the ‘AI bookkeeping’ wave

The cautionary tale is ScaleFactor, a startup that raised roughly $100M claiming AI-powered bookkeeping.

It’s a good story that went down in flames, because they were telling everybody they were AI — and then all the investors realized this isn’t AI, it’s offshore resources plus some tech. And they shut down.

Chris Williams, Acquiring Minds

And it was not just one bad actor. During diligence I talked to people close to the biggest names in the category:

Pilot and Bench and Botkeeper… if you talk to them as part of diligence — I talked to some investors in those businesses — they’re like: yeah, it’s tech-enabled. It’s not full AI yet, because it’s just more complicated than people thought it was.

Chris Williams, Acquiring Minds

Several firms that launched as ‘AI for bookkeeping’ quietly pivoted to API integrations, some automation, and offshore labor doing the rest. The pattern repeated after the podcast was recorded, too. [UPDATE: add 2024-2026 developments here — e.g., Bench’s abrupt December 2024 shutdown and acquisition, and the current state of AI bookkeeping tools — verify facts before publish.]

What AI actually does well in bookkeeping

Here is the part that should worry bad bookkeepers: the routine layer really is getting automated, and I said so before I owned the firm.

The very basic reconciliation work or transaction coding — where you’re basically taking credit card transactions and putting them to the right account in your QuickBooks file — that’s already getting somewhat automated. That will continue to get further automated.

Chris Williams, Acquiring Minds

That prediction held. Today, automation and AI handle a meaningful share of transaction categorization, bank-feed matching, receipt capture, and anomaly flagging — and we use those tools aggressively inside our own workflows. [UPDATE: name the current tools/AI capabilities System Six uses in 2026.] If a provider is doing all of this by hand, you are paying for inefficiency.

What AI still does not do is the part clients actually pay for:

- Judgment calls: how to treat an unusual transaction, when something in the books signals a real business problem, what accrual treatment fits a messy contract.

- Accountability: someone whose name is on the work, who fixes it when a bank feed silently breaks or a payroll filing bounces.

- The advisor relationship: explaining what the numbers mean and what to do about them, in a conversation, with context about your business.

The bet I made: automation moves, humans judge

When I decided to buy, this was the thesis I hung my hat on:

At the end of the day, does the client want to deal with a robot, or somebody in an offshore capacity — or do they want to deal with a trusted advisor, US-based? That’s where we’re hanging our hat… There still has to be a person for the judgment-call stuff, and also just to be the adviser to the client. I don’t think that will ever get automated away.

Chris Williams, Acquiring Minds

Notice what the bet was not. It was not that AI would fail — it was that AI would commoditize the bottom of the market while making great humans more valuable. Clients who want the cheapest, lowest-touch service will increasingly be served by software, and that is fine. Clients who want someone to take real ownership of their finance function — bookkeeping plus payroll, bill pay, invoicing, and a controller-level second opinion — want a human team that uses the best tools, not a tool with no human behind it.

We priced and positioned the firm accordingly: higher service, higher value, deliberately not chasing the cheapest clients. Years later, that segmentation is exactly how the market has split. [UPDATE: add a current proof point — client growth, retention rate, or a client quote.]

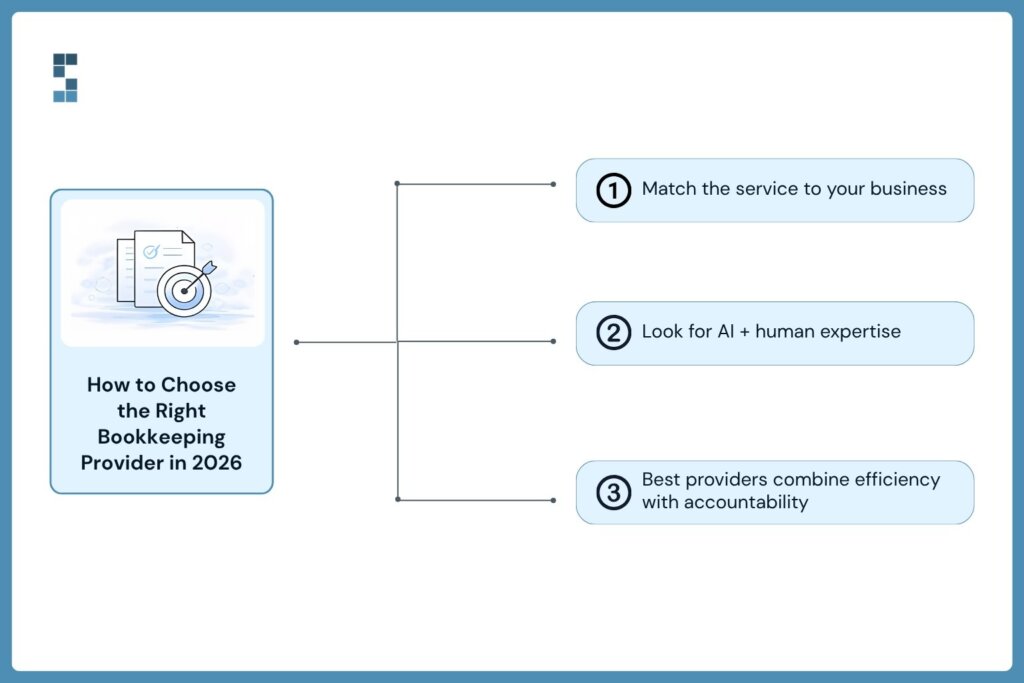

What this means if you’re choosing a bookkeeping provider in 2026

Whether you should use an AI-first service or a human team depends on what your books are to you:

- If your business is simple — low transaction volume, cash basis, no payroll complexity — an AI-first or software-only service is a legitimate, cheap option. Go in with eyes open about support when something breaks.

- If you run decisions off your financials, have payroll and bill pay, or answer to a lender or investors, you want humans with AI leverage: the automation catches the routine, a named team catches what the automation misses.

- Ask any provider the ScaleFactor question: what exactly does your AI do, and who checks its work? A confident provider will answer specifically. A marketing-driven one will repeat the word AI.

Frequently asked questions

Will AI replace bookkeepers?

It is replacing the routine layer — transaction coding, reconciliation matching, receipt capture — and it will keep absorbing more. It is not replacing judgment, accountability, or the advisor relationship. Bookkeepers who refuse to use AI will be replaced by bookkeepers who use it well.

Is AI bookkeeping accurate?

For clean, high-volume, repetitive transactions, quite accurate. The failure mode is silent errors on unusual items: miscategorized transactions that compound for months because no one with context reviewed them. That is why the working model is AI plus human review, not AI alone.

What happened to ScaleFactor?

It raised roughly $100M claiming AI-powered bookkeeping, and shut down in 2020 after it became clear the ‘AI’ was largely offshore accountants plus some tech. It remains the category’s cautionary tale about marketing outrunning capability.

Are services like Pilot actually AI?

They are tech-enabled human services: software handles integrations and automation, people do the judgment work. That is not a criticism — it is the model that works. The distinction matters when a provider’s pricing or marketing implies no humans are needed.

Should I use an AI bookkeeping service or a human team?

Simple books and tight budget: AI-first is viable. Real complexity — payroll, bill pay, accrual, investor reporting — get a human team that uses AI for leverage. The cost difference buys you someone accountable when it matters.

Talk to a human team that uses AI properly

We are not anti-AI — we are anti-unaccountable. Our team automates everything worth automating and puts a named, US-based human behind every judgment call. If you want to see exactly where AI fits in your books and where it should not, book an intro call and we will walk you through it with your own numbers.

Book an intro call with System Six.

by Chris Williams | Jul 27, 2026 | Blog

Most explanations of a quality of earnings report are written by firms that sell them, for an audience they assume already knows the vocabulary. I came to this from the other direction. I spent years in private equity reading QoE reports, then spent a year as a searcher trying to buy a company with my own money on the line, and then actually bought one. I have been the person staring at a seller’s adjusted EBITDA wondering which add-backs were real, with an exclusivity window burning down and a lender asking for third-party validation. Three times now, since we’ve done two add-on acquisitions.

So this guide covers what a quality of earnings report actually is, what’s inside one, what it costs, how long it takes, and how to choose who does yours, written the way I wish someone had written it for me before my first deal.

What a quality of earnings report is (and is not)

A quality of earnings report, or QoE for short, is an independent analysis of a company’s financial performance, built for one purpose: a transaction. If you are asking what QoE means in finance, it is this: a third-party examination of whether the earnings a seller is showing you are real, recurring, and transferable to a new owner.

Those three words carry the whole engagement. Real means the revenue and expenses tie to cash or correct accrual concepts, not to optimistic bookkeeping. Recurring means the EBITDA you are paying a multiple on will keep showing up after close, rather than being propped up by one-time projects, a COVID bump, or a customer that just churned. Transferable means the earnings don’t walk out the door with the seller: they aren’t dependent on the owner’s relationships, below-market rent from a building the seller keeps, below-market wages or benefits, missing PTO accruals, and so on. Will the earnings the seller is showing you actually show up in Month 1?

A QoE is just as defined by what it is not. It is not an audit: no legal opinion is issued, and it does not certify GAAP compliance, but it will certainly look for inconsistencies. Just know it can’t catch everything. If you don’t trust your seller, don’t rely on your QoE to 100% protect you. It is not a valuation; it will not tell you what the business is worth, though it gives you the corrected earnings number you apply your multiple to. And it is not a guarantee; it is a diligence tool that converts “trust me” into schedules you can verify.

In the lower middle market, where most sellers have never had audited statements and the books are kept on a cash basis by a part-time bookkeeper, the QoE is usually the first time anyone has rigorously tested the numbers at all. That is exactly why buyers, lenders, and investors insist on it. And if anyone you are working with is not insisting on it, you may want to consider how good of a partner they really are.

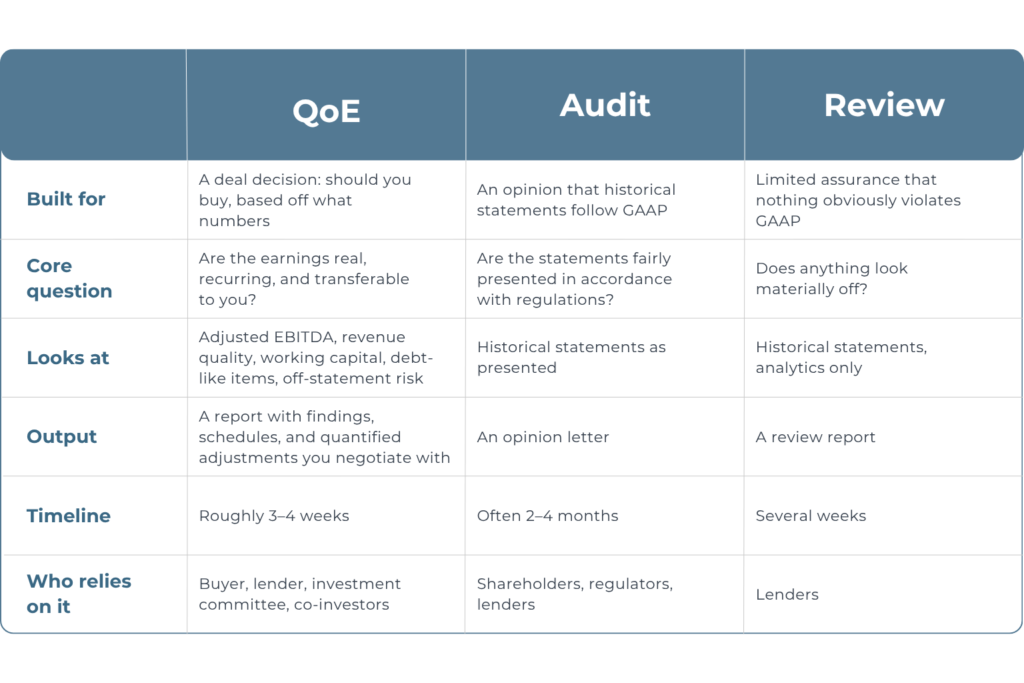

QoE vs. audit vs. review: what’s actually different

This is the most common point of confusion, so let me be precise. An audit answers: do these historical financial statements fairly present the company’s position under GAAP? A review is a lighter version of the same question. A quality of earnings analysis answers a different question entirely: can you, the buyer, rely on these earnings to price and finance this deal? The practical implication: an audit can be clean and the deal can still be terrible. Audited statements can fairly present earnings that are entirely dependent on one customer, stuffed with owner expenses, or about to fall off a cliff. The QoE exists to catch precisely the things an audit is not designed to look for. If a seller tells you “we have audited financials, you don’t need a QoE,” that is a misunderstanding at best.

The practical implication: an audit can be clean and the deal can still be terrible. Audited statements can fairly present earnings that are entirely dependent on one customer, stuffed with owner expenses, or about to fall off a cliff. The QoE exists to catch precisely the things an audit is not designed to look for. If a seller tells you “we have audited financials, you don’t need a QoE,” that is a misunderstanding at best.

What’s inside a QoE report, section by section

A good quality of earnings report follows a recognizable anatomy. Here is what each section does and why you should care about it.

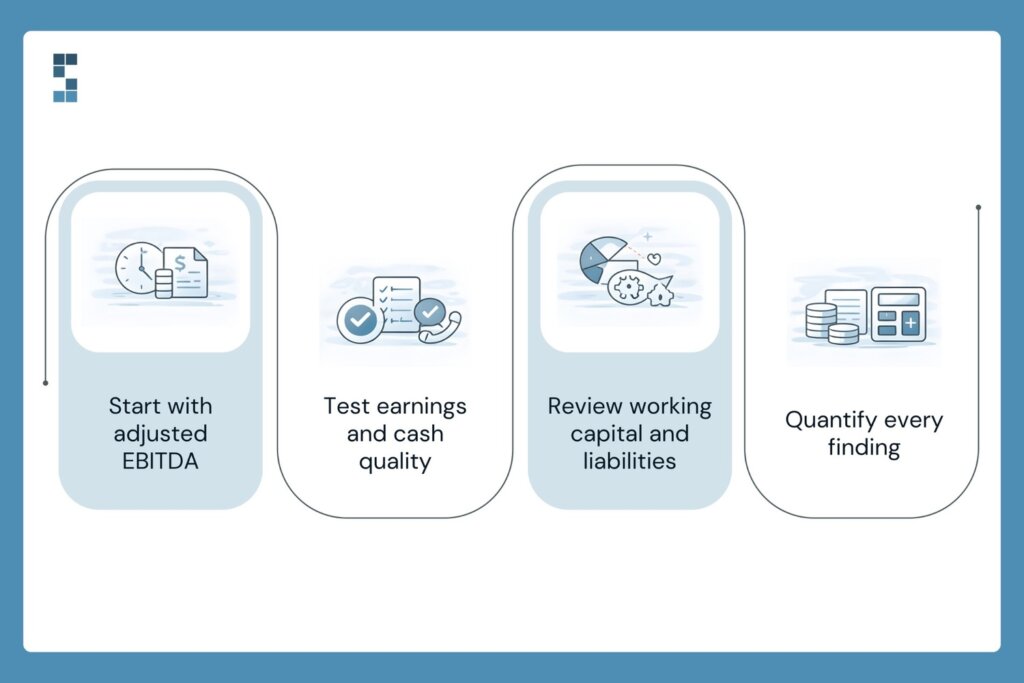

Executive summary. The first two pages should lead with the answer: here is reported EBITDA, here is what we think true adjusted EBITDA is, here is the bridge between them, and here are the findings that should change how you think about price and terms. If a provider buries the conclusion on page 40, that tells you who the report was really written for.

The EBITDA bridge and adjustments schedule. This is the heart of the report: a line-by-line walk from reported EBITDA to adjusted EBITDA. Every seller’s add-back gets tested. Owner compensation is normalized to market rate, personal expenses run through the business get flagged, one-time legal or moving costs get isolated, and related-party rent gets marked to market. Some adjustments cut in your favor; plenty cut against the seller’s number. On a 4–7x multiple, every dollar of EBITDA that doesn’t survive scrutiny is four to seven dollars of purchase price.

Revenue quality and customer analysis. Recurring versus one-time revenue, customer concentration, cohort and retention trends, pricing versus volume growth. A company growing entirely through price increases on a shrinking customer base looks identical to a healthy grower on the P&L summary, and completely different here.

Proof of cash. The analysis ties reported revenue and earnings back to actual bank activity. For lower-middle-market companies with unaudited, cash-basis books, this is the single most important credibility test in the report. If earnings can’t be traced to the bank, nothing else in the data room matters.

Net working capital analysis. The report establishes what normal working capital looks like across the trailing twelve months, which becomes the basis for the NWC peg, the target that determines whether you get a credit or write another check at close. Buyers consistently underestimate this section; the peg quietly moves real dollars. I can’t overstate enough how important this is. I’ve seen too many buyers buy a decent business but then come to really struggle as they come into a cash crunch from oversights related to QoE.

Debt and debt-like items. Beyond the obvious bank debt: deferred revenue, unpaid payroll taxes, customer deposits, accrued PTO, pending sales-tax exposure. These are dollar-for-dollar price reductions hiding in the balance sheet, and sellers rarely volunteer them.

Findings and considerations. The issues that don’t fit a schedule: GAAP departures, related-party entanglements, off-balance-sheet liabilities, accounting changes that flatter the trend. Each finding should be quantified where possible; a finding without a dollar figure is an anecdote, not a negotiating position.

Who actually needs a quality of earnings report

The short answer: anyone buying a business with their own money or someone else’s, and anyone whose capital depends on the deal being what the seller says it is.

Buyers, from individual searchers to independent sponsors to funds. If you are acquiring a company in the lower middle market, the QoE is your primary defense against overpaying. You are typically buying unaudited books, and you are personally guaranteeing debt or investing the bulk of your net worth. I have watched findings from diligence reprice deals by full turns of EBITDA. The report pays for itself the first time it finds something, and it almost always finds something. The QoE often does double duty: it protects you, and it is the trust instrument that makes your deal credible to family offices and co-investors who weren’t in the room. An LP-ready report from a recognized provider travels with the deal.

Lenders. SBA lenders, senior lenders, and private credit funds increasingly require an independent QoE before committing financing, particularly when the borrower is a first-time buyer. The bank is underwriting the same earnings you are; they want third-party validation, not the seller’s spreadsheet.

Sellers, sometimes. Sell-side QoE exists. Owners commission one before going to market to find the problems first and defend their number. This guide is written for the buy side, but if you are a seller reading this: every issue covered here will be found eventually. Better that you find it.

What a quality of earnings report costs

Pricing follows scope, deal size, and the state of the seller’s books, but the market clusters into three tiers.

- Focused-scope QoE / QoE Lite: roughly $10,000–$20,000 for smaller deals (<$5M). A concentrated look at proof of cash, the major add-backs, and the obvious risks. Appropriate for smaller deals and first-pass screening. There are services below $10,000, but my advice is to shy away from those. This is for many the most important financial decision of your life, or Top 3 (marriage, house, business acquisition). Don’t skimp on the very work that may save you from blowing it all up.

- Full-scope QoE from a boutique or regional firm: roughly $25,000–$50,000 for typical lower-middle-market deals. The full anatomy described above, sized to the complexity of the business.

- National and Big-4 firms: $100,000+, with the work frequently performed by junior staff under a recognizable brand. For LMM deals, you are often paying for a logo your lender doesn’t actually require. You shouldn’t be spending this much.

Two pricing structures exist: fixed-fee and hourly. Push hard for fixed-fee. Diligence on a messy company expands to fill whatever budget is available, and an hourly engagement puts the timeline risk and the cost risk on you simultaneously. A provider who has seen enough LMM books can scope fixed-fee with confidence; reluctance to do so is information.

One more framing that matters: on a $5M deal at 5x, a $35,000 QoE is 0.7% of purchase price. A single disallowed add-back of $50,000 in EBITDA moves price by $250,000. The asymmetry is the whole argument.

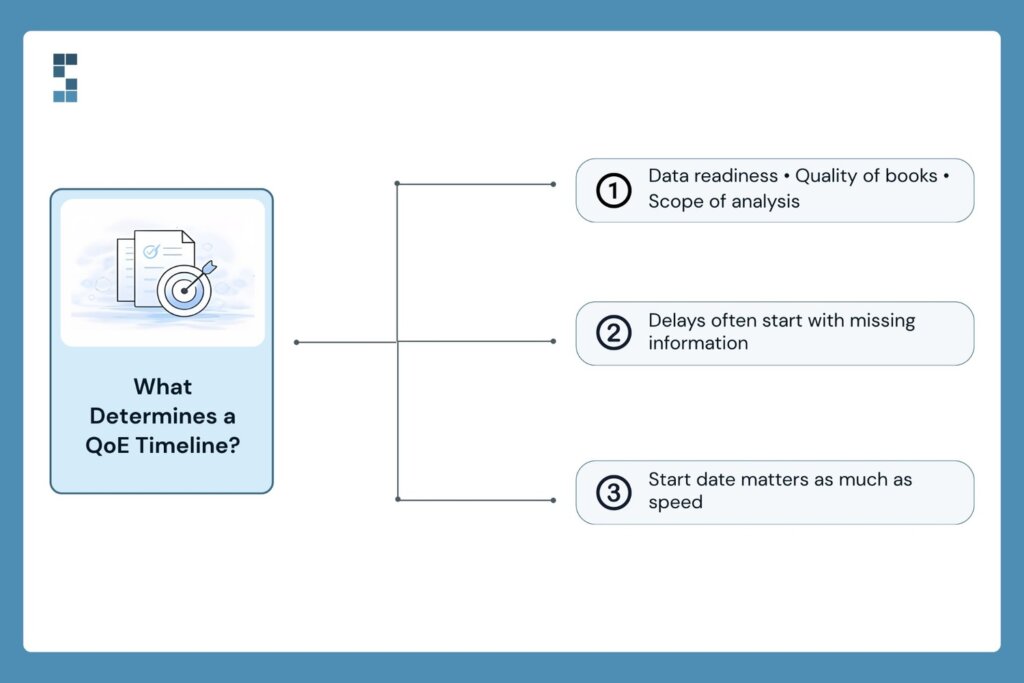

How long a QoE takes

The honest range is three to four weeks from data delivery to draft report for a typical lower-middle-market deal, with three things driving where you land in that range.

First, data readiness. The clock starts when the seller delivers the day-one request list: financial statements, trial balances, bank statements, customer-level revenue, payroll detail. A seller who takes three weeks to produce bank statements adds three weeks to your timeline. Get the request list to the seller the day the LOI is signed. Make sure it’s only the most important things you request. Don’t kill the deal immediately with a massive, overwhelming diligence list.

Second, the state of the books. Clean accrual books in QuickBooks Online move fast. Cash-basis books with commingled personal expenses and an inventory number nobody believes move slower, because the team is reconstructing reality before they can analyze it.

Third, scope. A QoE Lite engagement can land inside ten business days; a full-scope analysis of a multi-entity company with deferred revenue takes the full month.

The reason timeline matters so much: most LOIs grant 60–90 days of exclusivity, and financing, legal, and confirmatory diligence all queue behind the QoE. A provider who quotes six to eight weeks because of staffing backlog is consuming your negotiating window. Ask about the start date, not just the duration. A fast team that can’t start for a month is slower than a steady one that starts Monday.

QoE Lite vs. full-scope: which one you actually need

A QoE Lite covers the kill-shot questions: does cash tie out, are the major add-backs real, is there a customer concentration or revenue-quality problem severe enough to walk away from, and some simple working capital analysis. It is the right tool when the deal is small, the books are simple, or you want a cheap early answer before committing to full diligence.

Full scope adds the complete working capital analysis, debt-like items inventory, detailed revenue cohorts, and quantified findings: the material you need to negotiate the peg, size an escrow, and satisfy a lender or investment committee. If you are using bank debt outside SBA, raising outside capital, or paying anything above a small-deal multiple, full scope is often where you will need to be.

A sensible pattern for cost-conscious buyers: start QoE Lite, with a pre-agreed upgrade path to full scope if the deal survives the first pass and if the deal is large enough. QoE Lite will work well for many deals.

Good providers will structure the engagement that way and credit the QoE Lite work against the full-scope fee. We scope this way deliberately. It puts the diligence spend where the deal risk actually is.

How to choose a QoE provider

Bookkeeping taught me that low barriers to entry produce enormous quality variance, and transaction diligence is no different. Six criteria separate providers who protect buyers from providers who produce shelf documents.

- Who does the work? The industry’s open secret is partner-sold, analyst-delivered: a partner wins the engagement and a rotating bench of juniors performs it. Ask exactly who will touch your deal, and whether the person in the sales call will be in the workpapers.

- Lower-middle-market fluency. A team calibrated on $500M companies will misread a $4M one, flagging normal owner-operator behavior as chaos while missing the actual LMM risks: payroll-tax exposure, related-party rent, cash revenue leakage.

- The sample-report test. Ask for a redacted sample before engaging. You are looking for an executive summary that leads with the answer, quantified findings, and schedules a lender can use. If the sample reads like a compliance document, your report will too.

- Defensibility under scrutiny. Your report will be attacked, by the seller’s accountant disputing adjustments and by your lender’s credit committee testing assumptions. Ask the provider how their adjustments have held up in retrades and whether lenders have accepted their reports without re-work.

- Fixed fee and a real timeline commitment. Scope, fee, and start date in writing. You are buying certainty inside an exclusivity window; a provider unwilling to commit to either is reserving the right to consume your deal clock.

- A relationship, not a transaction. The best diligence engagements are conversations: findings surfaced as they emerge, not detonated in a final readout. You want a partner who picks up the phone when the seller’s CFO says something odd on a Tuesday. This is the difference between white-glove diligence and a PDF.

Notice what is not on the list: brand prestige. In the lower middle market, lenders and investment committees care that the work is independent, rigorous, and legible, not that it carries a Big-4 logo and a Big-4 invoice.

Frequently asked questions

What is QoE in finance?

QoE stands for quality of earnings: an independent analysis, performed during M&A diligence, of whether a company’s reported earnings are accurate, sustainable, and transferable to a buyer. The deliverable is a quality of earnings report.

What does a quality of earnings report show?

A bridge from reported to adjusted EBITDA, tested add-backs, revenue and customer quality, proof that earnings tie to bank activity, normalized working capital, debt-like items, and quantified findings that affect price and deal terms.

Is a QoE the same as an audit?

No. An audit issues an opinion on whether historical statements follow GAAP. A QoE evaluates whether the earnings are real, recurring, and transferable for a transaction. Audited financials do not eliminate the need for a QoE.

How much does a quality of earnings report cost?

Typically $10,000–$20,000 for a QoE Lite scope and $25,000–$50,000 for full scope from a boutique firm in the lower middle market; national firms run substantially higher. Fixed-fee pricing is preferable to hourly.

How long does a QoE take?

Generally three to four weeks from receipt of complete data, depending on scope and the condition of the seller’s books. Seller responsiveness is the biggest variable.

Who pays for the QoE in an acquisition?

The party that commissions it. Buy-side QoE is paid by the buyer and is the buyer’s work product; sell-side QoE is commissioned and paid for by the seller before going to market.

Do lenders require a quality of earnings report?

Increasingly, yes: SBA lenders, senior lenders, and private credit funds commonly require an independent QoE as a condition of financing, especially for first-time buyers and deals above roughly $1M in EBITDA.

Talk to the people who will actually do the work

If you are heading into diligence, don’t start with a sales pitch. Start with the deal. Bring us the CIM or the seller’s P&L, and we will tell you what we see, what we would scope, exactly who would do the work, and what it would cost as a fixed fee. If a QoE Lite pass is all the deal needs, that is what we will recommend.

Book a diligence scoping call with System Six.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Jul 20, 2026 | Blog

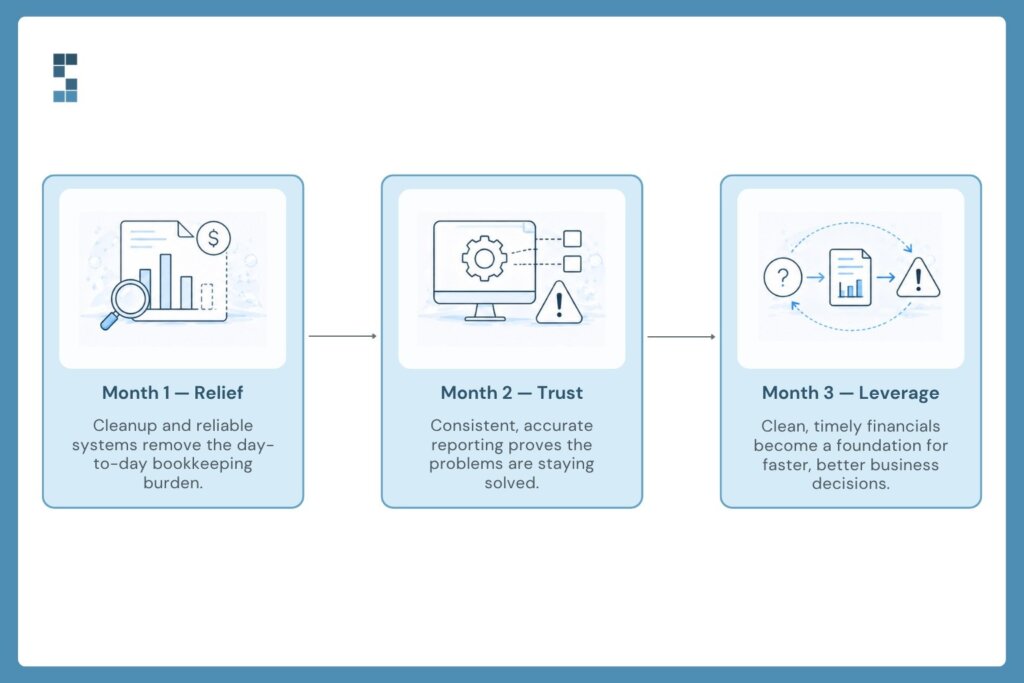

The short answer: The first 90 days with a new bookkeeping provider follow a recognizable arc. Month one brings relief as the backlog clears and someone else owns the books. Month two brings trust, as the numbers start arriving on time and proving accurate. Month three brings a shift in how you use your books, from checking the past to steering the business. Clients typically report a 70 to 80 percent reduction in administrative time within 90 days, and many say the service pays for itself in that window on time savings alone.

Wesley signed the engagement letter and then, for about a week, quietly wondered if he’d just made an expensive mistake. He’d heard the pitch. Clean books, time back, clarity. But he’d heard pitches before. What he actually wanted to know was simpler and harder to get: what does this look like in three months, from someone who isn’t selling me anything?

Fair question. Marketing copy tells you what a service promises. Clients tell you what it delivers. So instead of another list of features, here’s the honest arc of the first 90 days, built from what System Six clients have actually said about it. Some of it is what you’d expect. Some of it isn’t. And the most interesting part, the thing almost nobody anticipates, doesn’t show up until month three.

What happens in the first 30 days?

Month one is about relief, and it arrives faster than most people expect.

The first thing that happens is that the backlog stops being yours. Someone else takes over the monthly bookkeeping and reconciliation, cleans up the errors sitting in your existing data, and gets automated workflows running for payables, receivables, and payroll. You get secure, cloud-based access so you can actually see your own numbers without asking anyone. Most of this happens without much input from you, which is itself a novelty if you’ve been the bottleneck for years.

What clients describe in this window is less about spreadsheets and more about their nervous systems. Betsy, who runs an investor-backed business, said System Six had done wonders for her stress level, that it finally felt like this was all taken care of with a professional partner. That’s month one. Not a dashboard. A dropped weight. The mental background process that had been running for years — are the books okay, did I miss something — finally switches off.

Is everything perfect by day 30? No. You’re still learning each other’s rhythms, and the cleanup often turns up things nobody knew were wrong. But the direction of travel is obvious immediately, and that’s what makes the first month feel like a decision you got right.

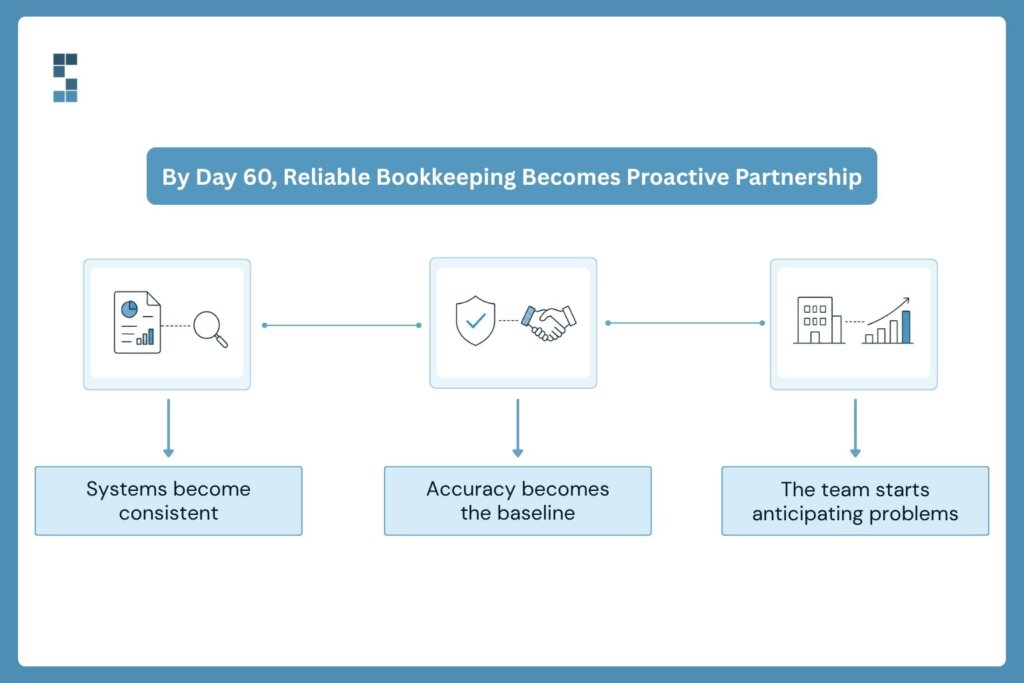

What changes by day 60?

Month two is where relief hardens into trust, and trust is a different thing entirely. Relief is emotional. Trust is earned, repeatedly, by numbers that show up on time and turn out to be right.

By this point the systems built in month one are running. Bank feeds flow automatically, categorization follows rules tuned to your business, and reporting arrives with current data instead of last quarter’s. The close gets faster. The reports stop being a thing you chase and start being a thing that appears.

But here’s what clients actually talk about at the 60-day mark, and it’s rarely the software. It’s the behavior of the people. Marcus, who works with the team on an investor-backed business, said he feels he’s in good hands and especially appreciates how they’re inquisitive, ask follow-on questions, and look around corners. John put it even more bluntly, telling the team to mark him down as an 11 out of 10 on any internal satisfaction tracking, calling the team awesome and proactive and exactly what he needed.

Notice what both of those are describing. Not accuracy, which they take as table stakes by now, but anticipation. The difference between a bookkeeper who records what happened and a partner who notices what’s about to happen. That’s the month-two revelation for most clients: they hired someone to keep the books and got someone who watches the road ahead.

There’s an external signal that tends to land around this point too, and it carries unusual weight. One client mentioned that System Six had been recommended by their CPA as the best firm in the business for a company their size. Think about why that matters. Your CPA has no incentive to flatter your bookkeeper; if anything, sloppy books make their job harder and their fees higher. When the person who has to work downstream of your bookkeeping vouches for it, that’s a professional endorsement rather than a marketing claim. By day 60 you’re usually not the only one who has noticed things got better.

What does month three look like?

Month three is when the relationship changes character, and this is the part people don’t see coming.

For the first two months, you use your books to answer questions about the past. What did we spend? Did that client pay? By day 90 something flips. The numbers are current and reliable enough that you start using them to make decisions about the future. Which service line deserves more attention. Whether you can afford the next hire. Whether that big opportunity is actually as profitable as it looks. Orlan described System Six as their secret weapon when it comes to getting their finances in order, and “secret weapon” is a telling phrase. Nobody calls a bookkeeper a weapon. They call a competitive advantage a weapon.

The numbers back up the vibe shift. Clients typically see a 70 to 80 percent reduction in administrative time within 90 days, and the automation work often pays for itself inside 60 to 90 days on recovered time alone. But the more interesting result is what people do with that capacity. Trevor, looking back over the first year, simply said his firm was in a much better place than it had been twelve months earlier because of the improvements made to their bookkeeping process. That’s the quiet compounding: fix the foundation, and everything built on it gets steadier.

And there’s a trust dividend that shows up at the far end. Paul told the team that hiring them was the best decision he made at the start of his business, and that after their 2022 audit the auditors found exactly zero errors. Not only had the team been mistake-free, he said, they’d been proactive about catching his mistakes and spotting challenges coming down the road. An auditor finding nothing is the most boring possible outcome, and boring, when it comes to your books, is the entire point.

What the pattern tells you

Read those experiences together and a shape emerges. Relief, then trust, then leverage. Month one takes the weight off. Month two proves the weight stays off. Month three turns clean books into better decisions.

It’s worth saying that not every relationship is identical. Firms arriving with messier books spend more of month one on cleanup. Firms already on solid systems move faster. But the sequence holds, because it’s less about the software than about what it takes for a person to stop worrying about something. You have to feel the burden lift, then watch it stay lifted, before you’ll start building on top of it.

That pattern is also why the strongest proof isn’t a statistic — it’s the fact that clients keep saying it out loud. Over half of System Six’s new clients each year come by referral, and existing clients rate the firm an average 9.5 out of 10 when asked whether they’d recommend it. Mari, after working with the team, described being impressed by how knowledgeable, thorough, thoughtful, and detailed they were. People don’t refer competence. They refer relief.

So back to Wesley’s question, the one worth asking before you sign anything. Not “what does this service promise?” but “what will I actually be feeling in three months?” Based on what clients say: lighter in month one, confident in month two, and by month three, a little annoyed you didn’t do it sooner.

Frequently asked questions

How long does it take to see results from a new bookkeeping provider?

Relief usually comes within the first 30 days, once the backlog is cleared and someone else owns the monthly bookkeeping and reconciliation. Measurable results follow quickly after: clients typically report a 70 to 80 percent reduction in administrative time within 90 days. Firms arriving with messier books spend more of the first month on cleanup, but the overall arc holds.

What results do bookkeeping clients actually report?

The most common reported outcomes are reduced administrative time, faster and more reliable monthly reporting, and significantly lower stress. Clients frequently highlight proactive service, being asked the right questions and having problems caught early, as much as they highlight accuracy. One client reported an external audit that found zero errors in the firm’s work.

How quickly does outsourced bookkeeping pay for itself?

For many firms, within 60 to 90 days on recovered time alone, before counting avoided errors or penalties. The payback comes from owner and staff hours redirected away from manual financial administration and back into billable or growth work. Firms with larger administrative burdens before the switch tend to see the fastest payback.

What should I expect in the first 90 days with a new provider?

Expect a three-stage arc. The first month centers on cleanup, system setup, and immediate relief from the administrative load. The second month builds trust as reporting becomes timely and accurate and the team starts flagging issues proactively. By the third month, most clients shift from using their books to review the past to using them to make forward-looking decisions about hiring, pricing, and growth.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Jul 13, 2026 | Blog

The short answer: Switching bookkeeping providers takes about 30 days and moves through four weekly stages. Week one is handoff and access: gather your logins, statements, and prior books. Week two is cleanup and migration, where the new provider corrects errors and sets up your chart of accounts. Week three is parallel running, where old and new overlap so nothing drops. Week four is go-live, with the new provider fully owning your books. Handled well, the switch happens quietly in the background while you keep working, and you never miss a payroll run or a close.

Grace had wanted to fire her bookkeeper for six months before she actually did it. The reports were late, the numbers felt shaky, and every question turned into a three-day email chain. But she kept stalling, and the reason was always the same fear: what if switching is worse than staying? What if payroll breaks mid-transition, or half her financial history vanishes into some export that never quite imports? So she white-knuckled it with a provider she’d already outgrown, held hostage by the dread of the move itself.

If that’s you, take a breath. Changing financial providers isn’t the cliff-jump it feels like from the edge. Done properly, it’s a calm, staged 30-day handoff where the new team does the heavy lifting and your day-to-day barely flinches. The fear isn’t irrational; plenty of switches have gone badly, but bad switches almost always come from having no plan. So here’s the plan: four weeks, four stages, and a smooth landing.

Why does switching bookkeeping providers feel so risky?

Let’s name the fear before we dismantle it, because pretending it isn’t there doesn’t help. What actually keeps owners with a provider they’ve outgrown?

Three things, mostly. First, continuity: your books are the financial memory of your business, and the thought of a gap, a missing month, a payroll that doesn’t run, feels genuinely dangerous. Second, the hassle: you assume switching means hours you don’t have, digging up logins and re-explaining your whole operation to strangers. Third, the sunk-cost pull: you’ve invested time getting this provider up to speed, and starting over feels like setting that on fire.

Here’s the reframe. Every one of those fears is really a fear of doing it without a system. A gap only happens if nobody plans the overlap. The hassle only balloons if there’s no clear checklist of what to hand over. And the sunk cost? That’s money already spent, and clinging to a provider that produces late, shaky numbers keeps spending it. The right question isn’t “what did I invest to get here?” It’s “What is staying here costing me every month?” Once you’ve got a real plan, the danger drains out of the whole thing. So let’s walk the four weeks.

And that second question deserves a real answer, because the cost of staying is easy to underestimate. Late reports mean you’re making decisions on old information or no information. Shaky numbers mean every figure carries a little asterisk of doubt, so you double-check things you shouldn’t have to and hesitate on moves you should make with confidence. The three-day email chains are hours of your month, quietly gone. None of that shows up as a line item, which is exactly why it’s so easy to tolerate for another quarter, and another. The fear of switching is loud and immediate; the cost of not switching is silent and ongoing. That asymmetry is the trap, and naming it is how you climb out.

What are the four stages of a smooth bookkeeping transition?

Week one is handoff and access. This is the gather-everything week, and it’s lighter than you’d think. You pull together the essentials: logins to your accounting software, recent bank and credit card statements, payroll records, and access to your existing books. A good incoming provider hands you a simple checklist so you’re not guessing what matters. Your job here is mostly to open doors, not to do the work. The new team takes it from there.

Week two is cleanup and migration. Now the new provider goes to work under the hood, and this is where a good one earns their fee immediately. They review your existing books, clean up errors the old setup left behind, and build a proper chart of accounts tuned to how your business actually runs. If you’re already on QuickBooks Online, this moves fast, sometimes fast enough to compress the whole timeline. This cleanup step is quietly one of the biggest wins of switching: you don’t just get a new bookkeeper, you get your history straightened out on the way in.

Week three is parallel running. This is the stage that kills the continuity fear. For a short window, the new system runs alongside the old one instead of flipping a switch and hoping. Transactions get processed in the new setup, reconciliations get checked against the prior books, and everyone confirms the numbers tie out before anything is turned off. Nothing gets dropped because nothing is ever unsupported. The overlap is the safety net.

It’s worth sitting on why this stage matters so much, because it’s the single thing that separates a smooth switch from a scary one. Most horror stories about changing providers, the vanished month, the payroll that bounced, the reports that didn’t reconcile, trace back to a hard cutover: someone turned the old system off before proving the new one was ready. Parallel running makes that failure mode impossible by design. You’re not trusting a promise that everything transferred correctly; you’re watching it transfer correctly, in real time, with the old books still there to check against. By the time the overlap ends, the new setup has already been doing the job for a couple of weeks. Go-live isn’t a leap of faith. It’s a formality.

Week four is go-live and ownership. The new provider takes full control. Bank feeds flow in automatically, categorization runs on rules built for your business, and reporting switches on with current data. The old provider is thanked and released. You wake up on day 30 with clean books, a team that answers questions the same day, and the quiet realization that the thing you dreaded for months just… happened, in the background, while you ran your business.

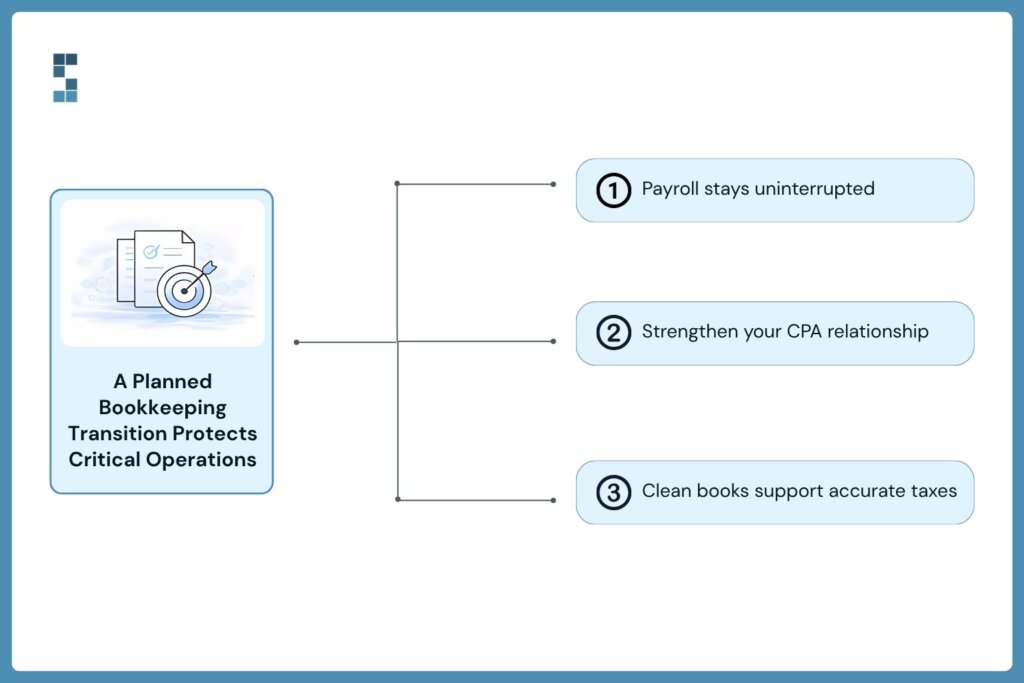

Will switching disrupt payroll, taxes, or my CPA relationship?

This is the practical worry underneath the big fear, so let’s hit it head-on. The three things owners guard most, payroll, taxes, and their CPA relationship, are exactly the things a staged transition is built to protect.

Payroll is precisely why week three exists. You never move payroll cold; you run it through the overlap until it’s confirmed clean, so your team gets paid on time throughout. Taxes stay safe because the cleanup in week two produces organized, accurate books, which is what your tax preparer actually wants. And your CPA relationship doesn’t just survive the switch, it usually improves, because a good bookkeeping provider coordinates directly with your tax preparer and hands them clean books that make their job easier and often reduce their fees. Many CPAs specifically ask their clients to work with a provider like this for exactly that reason. Switching your bookkeeper doesn’t threaten these relationships. It reinforces them.

Make the call before another month leaks away.

If you’ve been stalling like Grace, here’s the one move that matters: separate the decision from the dread. You already know whether your current provider is serving you. The only thing holding you back is the imagined chaos of the switch, and now you can see it isn’t chaos, it’s a checklist. Four weeks, mostly handled for you, with an overlap that guarantees nothing breaks.

Most firms are fully up and running with a new provider within about four weeks, faster if the books are already in decent shape. That’s the whole cost of escaping late reports and shaky numbers: roughly one month of a well-run process, most of it invisible to your day. This is the kind of onboarding System Six runs for the consulting firms, search funds, and growing businesses it serves: cleanup, migration, and a clean handoff, with the overlap that keeps payroll and reporting steady the entire way. It’s part of why over half of new clients come by referral, and why existing ones rate the firm an average of 9.5 out of 10. People refer to the relief of a switch that turned out to be painless.

So here’s the question worth answering honestly. If the switch itself is only 30 mostly-hands-off days, what exactly are you waiting for, and what is that wait costing you? The provider you’ve outgrown isn’t getting better. But the path to a better one is shorter and smoother than the fear has been telling you. Start the clock.

Frequently asked questions

How long does it take to switch bookkeeping providers?

Most firms are fully operational with a new provider within about four weeks. The timeline covers handoff and access, cleanup and migration, a parallel-running overlap, and go-live. If your books are already on QuickBooks Online and in reasonable shape, the process can often be compressed to two or three weeks.

Will I lose my financial history when I change providers?

No, not with a staged transition. Your existing books and records are gathered during the handoff week and migrated into the new setup, so your history moves with you rather than disappearing. The parallel-running stage adds a safety net: the new system runs alongside the old one, and the numbers are confirmed to tie out before anything is turned off.

Will switching bookkeepers disrupt my payroll?

It shouldn’t, because the overlap stage specifically protects payroll. Rather than moving payroll cold, a good transition runs it through the new system alongside the old until it’s confirmed clean, so your team keeps getting paid on time throughout the switch. Payroll continuity is one of the main reasons the transition is staged over several weeks instead of being flipped all at once.

Can a new bookkeeper work with my existing CPA?

Yes, and it usually makes the relationship better. A good bookkeeping provider coordinates directly with your tax preparer and delivers organized, accurate books that make their job easier and can reduce their fees. Many CPAs specifically request that their clients work with a dedicated bookkeeping provider for exactly this reason.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Jul 6, 2026 | Blog

There’s a lot of advice about how to buy a business. There’s much less about the part nobody can rehearse: the first year of actually owning one. I went through a self-funded search in 2020. In July 2021, I closed on System Six, an outsourced accounting and bookkeeping firm — a roughly 18-person business doing about $2.5M in revenue and just over $1M in EBITDA, financed through a typical self-funded SBA loan, a seller note, and some investor capital. About fourteen months in, I sat down to talk honestly about what had actually happened. This is that account — what the transition really looked like, what I’d tell my 2020 self, and where a new owner should put their attention first.

The numbers, fourteen months in — and why the margin going down is fine

Start with the scoreboard, because it isn’t as clean as the pitch decks suggest. We went from about 18 people to roughly 30, and from $2.5M to somewhere around $3.6–3.7M in revenue. But EBITDA did not grow in lockstep — it was up maybe 10% in a year when revenue was up 25–30%.

That gap surprises new owners, and it shouldn’t. When you’re accelerating growth, your margin compresses on purpose. We hired ahead of the revenue, added a management layer, and put more of everyone’s time — including mine — into running and building the business rather than just doing the work. If you buy a small company and your margin holds perfectly flat while you grow, you’re probably under-investing in the thing that lets you grow next year.

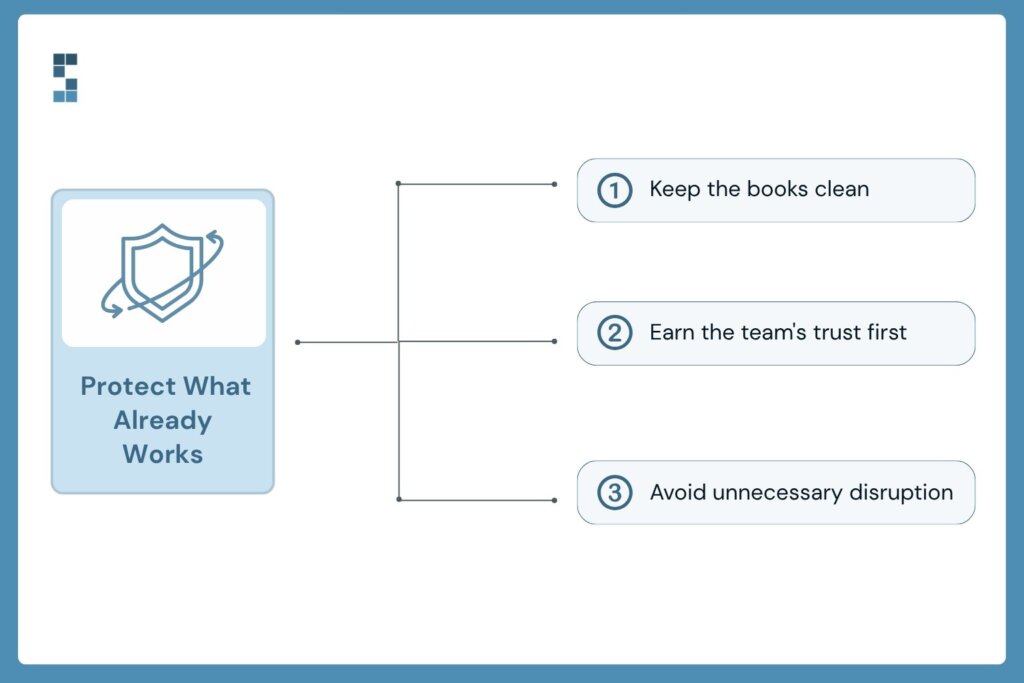

The first thing I protected: don’t break the books — or the team

The single biggest risk in the early months isn’t strategy. It’s that you, the new owner, quietly break something that was working. For us, that meant two priorities above everything else.

First, the financials. We are a bookkeeping firm, so this is on-brand, but it’s true for any acquisition: your clean books are how you know whether anything else you’re doing is working. A messy transition that corrupts your numbers blinds you for a year. Keep the close running on time from month one.

Second, the people. I’d spent real time before the deal with the seller and his family, and it was obvious how much they cared about the team they’d built. My job in the first six months wasn’t to remake the place — it was to earn the team’s trust and keep the culture that made the business worth buying. Changes came later and slowly.

Self-funded SBA vs traditional search fund: what I’d tell my 2020 self

I came out of business school oriented toward a traditional search fund, and ended up doing a self-funded SBA deal instead. Fourteen months in, I’m glad I did — and I have two reflections for anyone choosing a path now.

The first is about optionality. Finding a genuinely good business to buy is hard, and anything that increases your odds of getting a deal done is worth a lot:

To the extent you can keep your options open by self-funding and allowing yourself to buy a smaller business, which is what I did, use an SBA loan… it just increases the chances that you’re going to buy a business.

Chris Williams — Acquiring Minds

The second is a counterweight: don’t let “self-funded” trap you into thinking small. If you can find a bigger business, the economics and the way you spend your time as CEO both improve. I recommend staying self-funded for optionality and keeping your eyes open for larger [$3–5M EBITDA] businesses if one appears. You’ll own a smaller slice, but a bigger, faster-scaling business can be the better outcome.

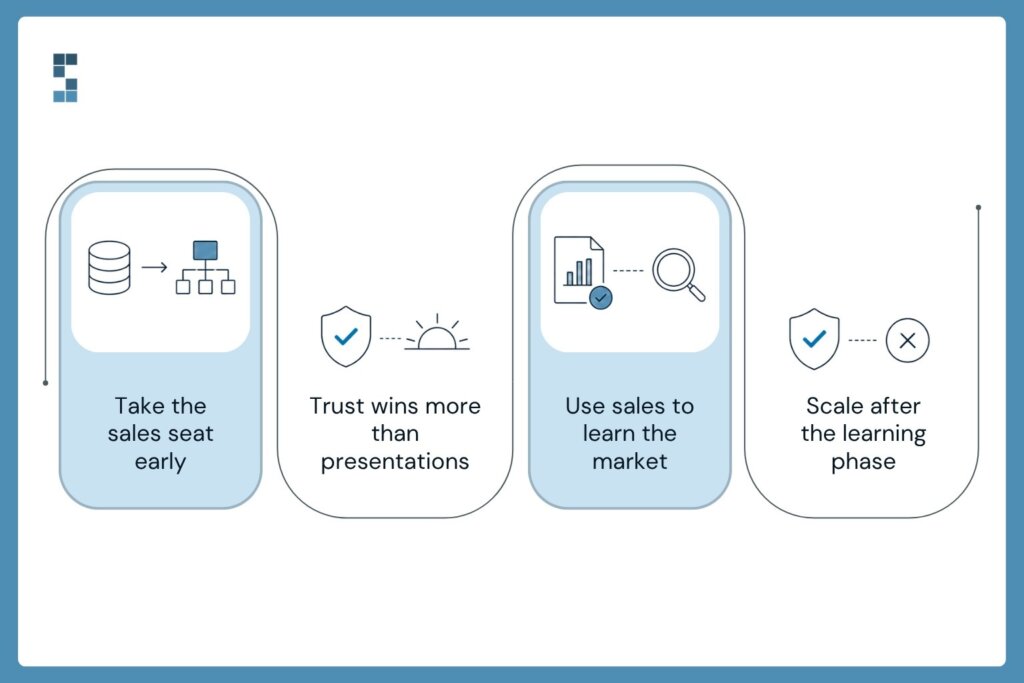

Inheriting the sales seat

Here’s the transition I underestimated most. The seller, John, was a natural salesman, and sales were his engine. I am not naturally inclined toward sales, and on close, that engine became my job.

There’s no clever shortcut I can offer — the answer was reps. I did about 75 sales calls in my first six months as owner, and well over a hundred the following year. What I learned is that our sale isn’t a hard technical demo; it’s a trust-building exercise:

We are really purchased based on trust and how much competence we can demonstrate through our sales process, which is really two touch points. I do a discovery call, and then we gain access to somebody’s books. We dig through it. Our team asks some questions.

Chris Williams — Acquiring Minds

That’s also a hint about how the service should feel later: if you win the deal by demonstrating competence on someone’s actual books, you’ve set the expectation that you’ll keep doing exactly that once they’re a client. The longer-term goal is to build a sales function that isn’t just the CEO — but in year one, founder-led selling is how you learn what your buyers actually need.

Hiring turned out to be the real constraint.

Most people assume the bottleneck in a service business is demand. For us, it was the opposite. The market was strong, and growth was sitting right in front of us; what gated it was our ability to bring the right people on board.

A business like ours, we can only grow as much as we can bring great people onto the team.

Chris Williams — Acquiring Minds

That reframed how I think about scaling. The top of the funnel that matters most isn’t leads — it’s hiring. And you can’t simply hire the leadership team you’ll need at 60 people when you’re sitting at 30; they’d be underutilized and bored. The move that actually worked was promoting from within: our team lead, Kelly, stepped into a Head of People role, growing into the seat as the company grew into needing it. Building the org one well-coached promotion at a time beats hiring a finished structure off the shelf.

The searcher niche found us.

One unexpected gift of the first year: being a former searcher turned into a real channel. Other people who’d just bought businesses wanted a books partner who understood what they were going through — and they tended to be larger, more sophisticated clients.

We have 15 or so search-acquired businesses we’re now serving; they’re larger and are pushing our average customer size up. More of them are accrual-based, which we can handle where others can’t.

Chris Williams — Acquiring Minds

Investors became an asset in the same period — not as bosses, but as a sounding board. I don’t have to give them control to get the benefit of their perspective: I want to treat them like they’re my board. And we’ve had board meetings every quarter. The meetings I prepared real materials for were the ones that pulled me up out of the day-to-day and made me think about the business strategically. If you take on investor capital, use it that way.

What year one actually teaches you

If I compress fourteen months into a few sentences: protect the books and the people before you change anything; expect margin to dip while you invest in growth; get your reps in on sales even if it isn’t your strength; and treat hiring as the real ceiling on how fast you can grow. None of it is glamorous, and all of it compounds.

If you’ve just bought a business — or you’re close — the highest-leverage thing you can do in the first 90 days is make sure your financials stay clean while everything else is in motion. That’s the one area where a mistake quietly costs you the whole year.

Page 1 of 1412345...10...»Last »