The short answer: To close your books in three days instead of ten, make three changes. Reconcile bank and credit card accounts continuously instead of all at once at month-end. Automate transaction categorization and bill capture so data arrives clean. And run a fixed, repeatable close checklist every month. Most firms lose a full week each cycle to waiting on data, not to the workload itself, which is exactly what these three moves remove.

It’s the 9th of the month. Priya, who runs a 14-person strategy consulting firm, opens her laptop and sees the same thing she sees every month: a half-finished close, three reconciliations that don’t tie out, and an inbox full of “any update on last month’s numbers?” She wanted those numbers a week ago. So did her partners. The books are still days from being done.

Sound familiar? If your month-end close drags past the first week and bleeds into the second, you’re not alone. And you’re not stuck. A ten-day close isn’t a law of nature. It’s usually a pile of small, fixable habits that quietly add up. Let’s pull that pile apart and see what a three-day close actually takes.

Why does month-end close take so long?

Most owners blame the volume of transactions. More clients, more invoices, more stuff to reconcile. Makes sense on the surface. But that’s rarely the real culprit.

The real culprit is waiting. You’re waiting on a credit card statement. Waiting on a contractor to send a receipt. Waiting on yourself to remember what that $1,200 charge was for. Each “quick” wait feels harmless, but they stack. A close isn’t slow because the work is hard. It’s slow because the work keeps stopping and starting.

There’s a quieter cost too. Every manual touch is a chance for an error, and errors don’t stay put. A miscoded expense here, a transposed number there, and suddenly a report you’ve already sent to a partner is wrong. Now you’re not just doing the work; you’re redoing it, and having the awkward conversation that comes with it. The close stretches not because there’s more to do, but because so much of it gets done twice.

Here’s the math that should bother you. If your close takes ten days and you’re spending even a couple of hours a day chasing loose ends, that’s a full work week every single month spent assembling a picture of the past. Twelve weeks a year. Three months of someone’s time, gone, to find out what already happened. And by the time those numbers land, they’re stale. You can’t steer a business looking in a rearview mirror that’s a week and a half behind.

How do you close the books faster? Three moves

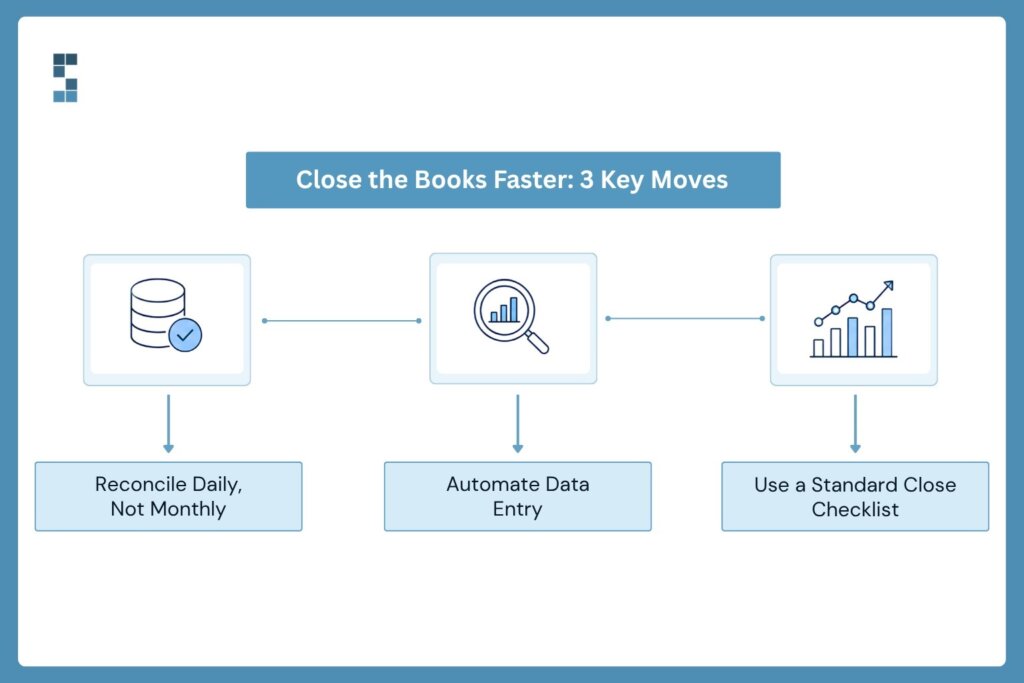

So how do you go from ten days to three? You stop treating the close as one giant event at the end of the month and start treating it as something that’s mostly already done before the month even ends. Three moves get you there.

First, reconcile as you go, not all at once. Waiting until the 1st to reconcile a month of transactions is like waiting until April to open every envelope marked “taxes.” Instead, connect your bank and credit card feeds so transactions flow in daily and get categorized as they happen. When the month ends, there’s almost nothing left to sort. The work is spread thin across thirty days instead of crammed into three.

Second, kill the manual data entry. Every number you type by hand is a number you might fudge, and a number someone has to double-check later. Automated categorization, bill capture, and direct integrations between your tools mean the data shows up clean and connected. One consulting firm we work with watched its month-end shrink from five to seven days down to less than a day after automating transaction processing and reporting. Same team. Same client load. The bottleneck wasn’t the people. It was the manual handoffs between them.

Third, build a real close checklist and run it like clockwork. Not a sticky note. A repeatable sequence: bank recs, credit card recs, payroll, accruals, review, report. When everyone knows the order and owns their piece, nothing falls through, and nobody’s left guessing what’s done. The close becomes a routine, not a scramble.

What does a faster close actually buy you?

Let’s be honest about why this matters. A faster close isn’t about bragging that your books are tidy. It’s about what you can do once they are.

When your numbers land on day three instead of day ten, you make decisions while they’re still fresh. You see a project’s margin slipping, and you adjust pricing before you bid the next one, not three months later when the damage is done. You spot a cash crunch coming, and you plan for it instead of reacting to it. You walk into partner meetings with answers, not apologies.

Think about what that fresh visibility unlocks. A firm that can see project profitability in near real time stops guessing about which engagements are worth chasing. It leans into the profitable ones and quietly retires the ones bleeding margin. One environmental consulting practice did exactly that and lifted its average project margin by 22 percent, simply because it could finally see, clearly and quickly, where the money was actually being made. That clarity didn’t come from working harder. It came from closing faster.

This is the difference between bookkeeping that records history and financial operations that actually drive the business forward. One of System Six’s clients, Paul, put it plainly after a clean audit: not only had the team been mistake-free, they’d been proactive about catching problems before they grew. That’s what a tight close feels like from the inside. You stop bracing for surprises. As Betsy, who runs an investor-backed business, described it, having a professional partner handle this did wonders for her stress level. The numbers just get taken care of, on time, every time.

And the time you win back isn’t trivial. Owners who reclaim that lost week put it straight back into client work and growth. It’s why over half of System Six’s new clients each year come from referrals, and why existing clients hand the firm an average 9.5 out of 10 when asked if they’d recommend it. People don’t refer a bookkeeper. They refer the feeling of not having to think about this anymore.

Start Small, Win Fast

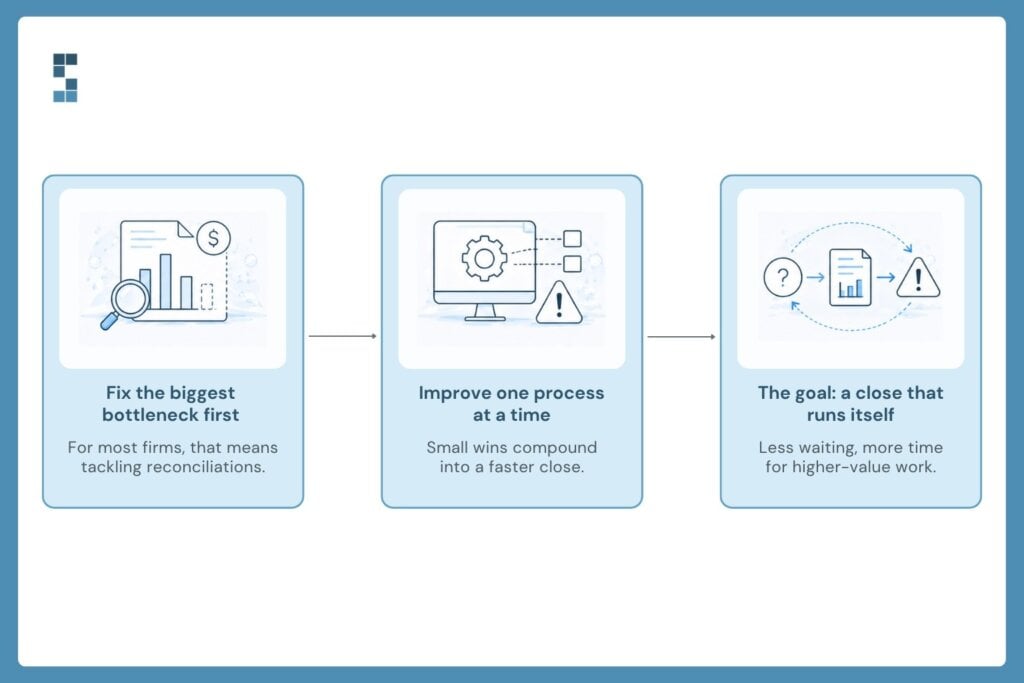

You don’t have to overhaul everything next Monday. Pick the single biggest source of waiting in your current close and fix that one thing first. For most firms, it’s the reconciliation pile, so start there. Connect your feeds, automate the categorization, and watch how much lighter the 1st of the month feels.

Then build from there. Master one piece, prove it works, and add the next. Before long, the close that used to swallow ten days quietly wraps in three, and you barely notice it happening. That’s the goal: not a heroic monthly sprint, but a close so smooth it almost closes itself.

So here’s the question worth sitting with. If you got that week back every single month, three full months a year, what would you actually do with it? Because right now, that time isn’t lost to the work itself. It’s lost to the waiting. And waiting is the one thing you can fix.

Frequently asked questions

How long should a month-end close take?

For a small consulting or professional services firm, a healthy month-end close lands in three to five business days. Many firms take eight to ten, but the gap usually comes from manual, start-and-stop work rather than transaction volume. With continuous reconciliation and automation, a three-day close is realistic for most firms under 50 employees.

What causes a slow month-end close?

The biggest cause is waiting on data: bank and credit card statements, missing receipts, and unremembered charges. Manual data entry adds a second drag, because every hand-keyed number invites an error that someone has to find and fix later. The close stretches not because there’s more to do, but because the work keeps stopping and so much of it gets done twice.

How can a small consulting firm speed up its close?

Start with the single biggest source of waiting, which for most firms is reconciliation. Connect your bank and credit card feeds so transactions flow in and get categorized daily. Then automate bill capture and reporting, and run a fixed close checklist each month so nothing falls through. Fix one bottleneck, prove it works, and add the next.

Does outsourcing bookkeeping make the close faster?

It can, when the partner runs continuous reconciliation and automated workflows rather than just replicating your manual process. System Six clients have cut month-end from five to seven days down to less than a day after automating transaction processing and reporting, keeping the same team and client load. The bottleneck is rarely the people; it’s the manual handoffs between them.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.