Maria thought she’d checked every box when she launched her consulting practice. Business license? Done. EIN from the IRS? Check. Liability insurance? Sorted. She even remembered to file her assumed name certificate with the county.

She hadn’t heard about the Corporate Transparency Act.

Neither have most small business owners. And that’s a problem, because this federal law—which took effect January 1, 2024—requires most U.S. companies to file beneficial ownership information with the federal government. Miss the deadline, and you’re looking at penalties up to $500 per day. Let it slide too long, and you could face criminal charges.

Don’t panic. This isn’t as complicated as it sounds. But it does require your attention, and the clock’s already ticking.

What the Corporate Transparency Act Actually Is

Here’s the deal in plain English: The Corporate Transparency Act requires most companies to report who actually owns and controls them. We’re talking names, addresses, dates of birth, and ID numbers for anyone who owns 25% or more of your business or exercises substantial control over it.

Why? The law aims to combat money laundering, tax evasion, and other financial crimes committed through anonymous shell companies. Think drug cartels and international fraud rings hiding behind layers of LLCs.

What does that have to do with your 5-person consulting firm? More than you’d think. The law casts a wide net. It doesn’t distinguish between a legitimate professional services company and a suspicious offshore entity. If you’re incorporated or formed as an LLC, you’re required to file.

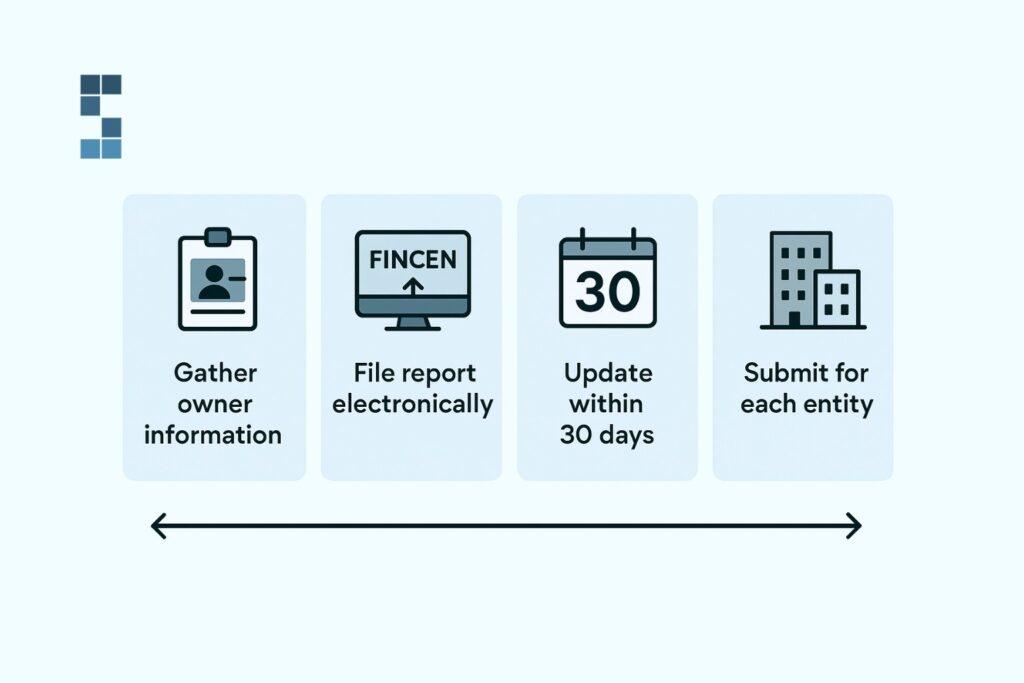

The requirements break down like this: existing companies formed before 2024 have until January 1, 2025, to file their initial report. Companies formed in 2024 get 90 days from formation. New companies formed after January 1, 2025, get just 30 days. The report goes to FinCEN—the Financial Crimes Enforcement Network, part of the U.S. Treasury Department.

So what actually counts as a “beneficial owner”? Anyone who owns 25% or more of your company, or anyone who exercises substantial control. That second part trips people up. If you’re the CEO making all the strategic decisions, but you only own 15%? You’re still a beneficial owner. If you’re a senior officer who could hire or fire the CEO? Beneficial owner.

Who This Actually Affects (and the Exemptions You Should Know)

Let’s start with the default position: you’re probably required to file.

Most small consulting firms fall under this law. LLCs, S-Corps, C-Corps—doesn’t matter. Single-member LLC operating from your home office? Still counts. Three-partner consulting firm with $2 million in revenue? Definitely counts. That boutique strategy practice you launched last year? Yep.

“I’m just a solopreneur” doesn’t exempt you. “We’re too small to matter” won’t save you either.

Wrong on both counts.

The exemptions exist, but they’re designed for a different type of company. Large operating companies with more than 20 full-time U.S. employees, more than $5 million in gross receipts, and a physical office in the United States get a pass. Certain regulated entities—banks, insurance companies, and accounting firms registered with the PCAOB—are exempt too.

Notice who’s missing from that list? Most consultants, advisors, coaches, and professional services firms. Even successful ones. You could be running a thriving $10 million consulting practice with 18 employees and still need to file, because you don’t quite hit that 20-employee threshold.

Here’s a real-world example: You’re running a 3-person strategy consultancy structured as an LLC. You own 60%, your business partner owns 30%, and you gave your first employee 10% as an equity incentive. You both need to report—you and your partner are clearly beneficial owners. Your employee probably doesn’t meet the threshold, since they’re under 25% and don’t exercise substantial control. But you’ll want to verify that, because “substantial control” can be subjective.

What You Need to Do (The Actual Action Steps)

Time’s ticking. For companies formed before 2024, you’ve got until January 1, 2025. That’s not as far away as it feels.

Start by gathering information for each beneficial owner. You’ll need their full legal name (exactly as it appears on their ID), complete address, date of birth, and a government-issued ID. A driver’s license or passport works. You’ll need a clear image or PDF of that ID, too—something readable that shows the ID number.

Then you file electronically through FinCEN’s system—no filing fee, which is a small silver lining. The actual filing takes 30-45 minutes once you’ve gathered everything. It’s not the filing that’s hard—it’s knowing you need to do it in the first place.

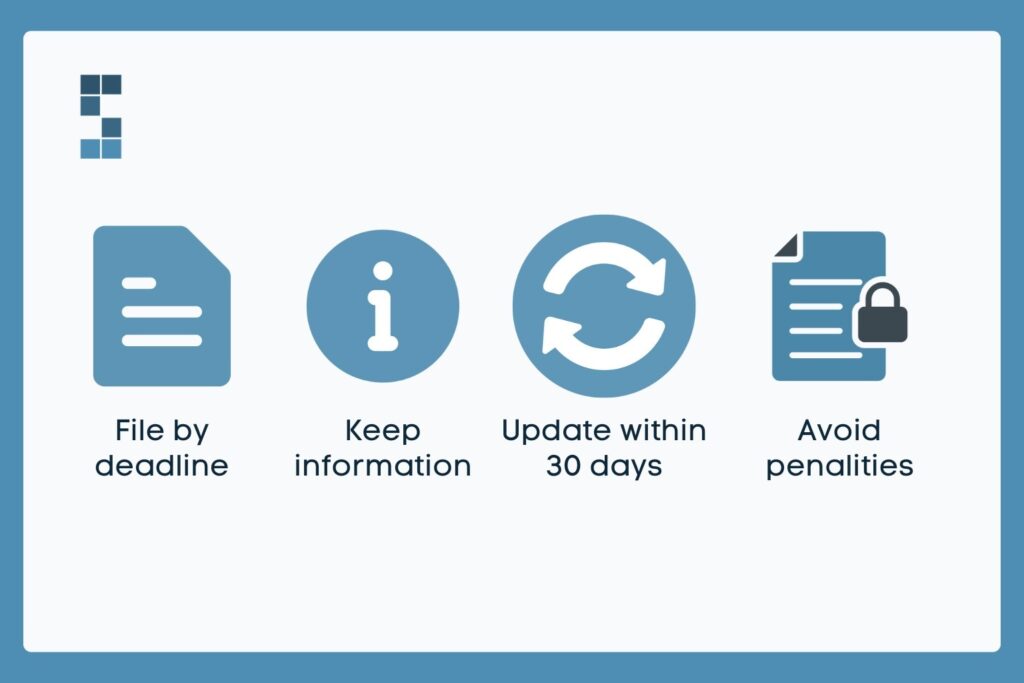

Here’s where it gets tricky: you need to keep this information current. Change your address? You’ve got 30 days to update your filing. Bring in a new partner? Thirty days. Does the existing partner sell their stake? Same 30-day window. Miss that deadline and you’re back to penalty territory.

The complexity multiplies if you’ve got multiple entities. Holding company that owns your operating company? You’re filing for both. Consulting firm with a separate LLC for your coaching business? Two filings. Each entity needs its own report, and each needs to be kept current.

This is where lots of consulting firm owners realize their time is better spent elsewhere. One System Six client put it perfectly: “System Six handles everything so professionally that I never worry about the financial side anymore.” That includes staying on top of compliance requirements like these—the kind that can sneak up on you if you’re focused on serving clients and growing your practice.

What Happens If You Don’t Comply

The stakes are real.

Civil penalties start at $500 per day. Miss the deadline by a week? That’s $3,500. Miss it by a month? Over $15,000. And it keeps climbing until you file.

But it gets worse. Criminal penalties can hit $10,000 in fines and up to two years in prison for willful violations. The government didn’t add criminal penalties for fun. They want compliance, and they’ve given themselves serious enforcement teeth.

“I didn’t know about it” won’t protect you. The law doesn’t care whether you heard about the requirement. It cares whether you filed. And “willful” means you knew about the requirement and ignored it. Once you finish reading this article, you know. The clock starts now.

Beyond the direct penalties, there’s practical fallout to consider. Banks are increasingly asking for this information during account opening or loan applications. Investors want to verify beneficial ownership before they write checks. Even routine business transactions can hit snags if you’re not compliant.

Think of it less like filing taxes and more like keeping your business license current. It’s not an annual thing you can batch with your year-end accounting. It’s ongoing, and it requires attention whenever ownership or control changes.

This isn’t meant to scare you. It’s intended to inform you. The actual filing isn’t difficult—it’s straightforward if you’ve got your documents organized. What trips people up is either not knowing about it until they’re past the deadline or knowing about it but putting it off until it becomes a crisis.

How to Handle This Without It Consuming Your Life

Here’s the reality check: you didn’t start a consulting practice to become a compliance expert.

Your time is worth somewhere between $200 and $500 per hour, depending on your specialty and client base. Spend five hours figuring out FinCEN’s filing system, tracking down documents, and stress-testing whether someone qualifies as a beneficial owner. You’ve just donated $1,000 to $2,500 in opportunity cost to the federal government.

You’ve got options.

The DIY approach makes sense if your structure is simple. Single-member LLC with no plans to bring in partners? The filing is straightforward once you know what you’re doing. Budget 2-3 hours to gather documents and complete the filing, plus time to set calendar reminders for any future updates you might need.

But if you’ve got multiple entities, complex ownership structures, or you want the peace of mind that comes from knowing it’s handled correctly? That’s when you bring in professional support.

Good financial partners handle this kind of compliance work as part of their service. As one environmental consulting firm owner noted after working with System Six: “We serve businesses across dozens of service industries and understand the unique requirements for licensing, bonding, prevailing wage, and other industry-specific compliance needs.”

The Corporate Transparency Act joins that list of industry-specific requirements that someone needs to track—the question is whether that someone should be you or a professional who’s already monitoring compliance changes across their entire client base.

Think about it this way: you wouldn’t tell your clients to DIY their strategy work, would you? You’d point out that while they technically could figure it out themselves, their time is better spent on their core business, while you handle the strategic thinking. The same logic applies to your own business operations.

The peace of mind factor is real. One search fund operator put it this way: “System Six has done wonders for my stress level to feel like this is all now taken care of with a professional partner.” That’s the goal—getting compliance requirements off your mental load so you can focus on what you’re actually good at.

Don’t Let This Derail Your Practice

The Corporate Transparency Act is here. It’s real. It affects you. But it’s also manageable—if you handle it.

File by the deadline. Keep your information current. Update within 30 days when ownership or control changes. Do those three things and you’re fine. Skip them and you’re looking at penalties that start steep and get worse.

Whether you tackle this yourself or bring in professional help, please don’t ignore it. The cost of non-compliance is real, and it’s not worth the risk.

If you’re running a consulting firm or professional services practice and you’re wondering how this fits into your broader compliance picture—or if you’d like to stop spending your weekends figuring out federal filing requirements—that’s precisely the kind of problem firms like System Six solve every day. Over 175 service businesses trust them to handle these details so they can focus on serving clients instead of decoding government regulations.

Do you need to file, or want to make sure you’re handling this correctly? Don’t wait until the deadline is looming. The January 1, 2025, cutoff for existing companies will arrive faster than you think.

And Maria? She filed hers last month. She’s sleeping better now.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, allowing owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance issues. Our team of over 35 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. From accurate bookkeeping to cash flow forecasting, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.