by Chris Williams | Dec 8, 2025 | Blog

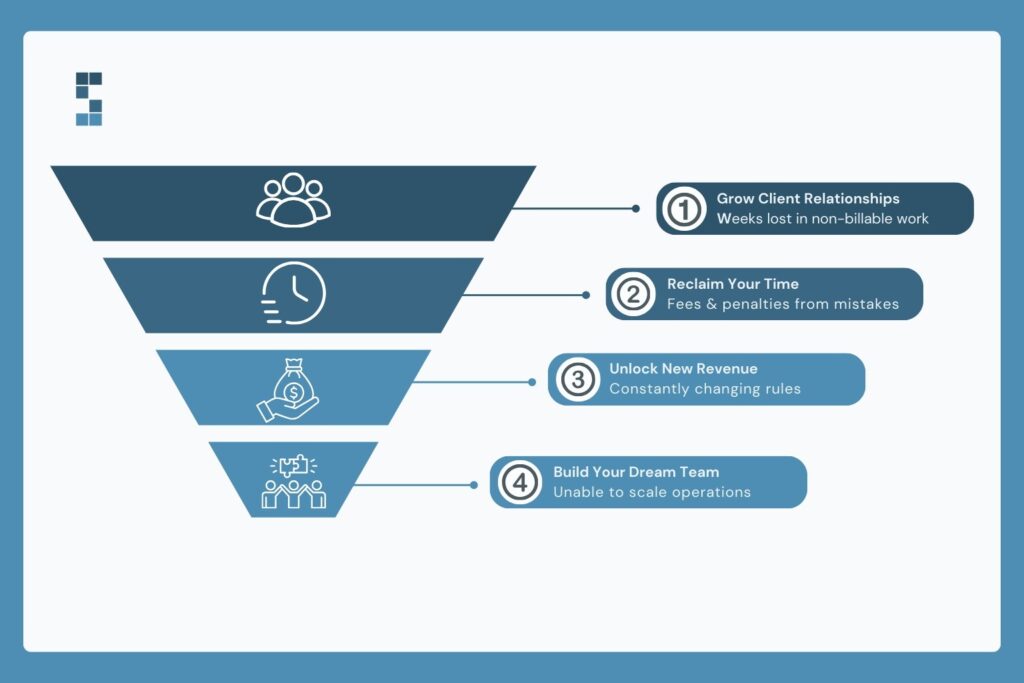

Marcus thought he’d cracked the code. By handling his consulting firm’s payroll himself instead of paying a service, he was saving $600 a month. Or so he believed. Then the IRS letter arrived.

Most of his payroll taxes had been filed incorrectly. The penalties alone hit $2,400. But that wasn’t the worst part. Fixing the mess required twenty hours of his time, plus another $1,800 in emergency accounting fees to untangle everything. His “$600 monthly savings” had just cost him nearly $5,000—in a single quarter.

Here’s what Marcus missed, and what most consulting firm owners miss when they calculate payroll costs: the price tag you see isn’t the price you actually pay. The real cost of DIY payroll lies in your time, your stress, your mistakes, and the opportunities you miss while you’re buried in tax forms instead of doing the work you actually get paid for.

Let’s walk through the real math—the kind that actually matters to your bottom line.

The Sticker Price Illusion

The appeal of DIY payroll seems obvious. You pay $50 per month for software, rather than $600-800 per week for a managed service. Quick calculation: you’re saving $550- $750 per month. Simple.

Except it’s not simple at all.

What gets left out of that calculation is your time. And if you’re billing clients at $200 an hour for consulting work, your time isn’t free—it’s expensive. Really expensive.

Processing payroll for a team of ten takes about three to four hours per pay period, including data entry, double-checking calculations, and running payroll. That’s eight hours monthly just for processing. Then add quarterly tax filings (another two hours each quarter), annual reconciliations (four hours), staying current on changing regulations (ongoing), and the inevitable troubleshooting when something doesn’t quite work right.

You’re looking at 80+ hours annually. At your $ 200-per-hour rate, that “free” labour just cost you $16,000.

And here’s the kicker—those are just the visible hours. They don’t include the fifteen-minute tasks that actually take an hour once you account for context switching, learning the software’s quirks, and tracking down missing information. One client told us he thought payroll took him “maybe twenty minutes” per session. When did he actually track it? Closer to ninety minutes once he included prep work, verification, and the emails to team members about missing timesheets.

What else could you accomplish with ten hours back each month? Win new clients. Develop that service offering you’ve been thinking about. Actually, take a weekend off without payroll anxiety.

The Hidden Cost Categories

Let’s break down what DIY payroll actually costs you. Four categories that most business owners miss entirely.

Time investment. We covered the basics above, but consider this: you’re not just processing payroll. You’re also handling new hire paperwork, termination documentation, benefits enrollment coordination, and fielding team questions about their paychecks. Every single pay period. It adds up to roughly 100 hours annually—equivalent to two and a half full work weeks you could spend on billable client work instead.

Error costs. This is where DIY payroll gets really expensive. IRS penalties for payroll tax mistakes average $845 per incident. State penalties stack on top. Incorrect withholding calculations require correction and often trigger additional penalties.

Here’s a real example: One System Six client discovered they’d been making a simple bookkeeping error that cost them $700 in unnecessary bank fees each month. That’s $8,400 annually from a single mistake they didn’t even know they were making. Another client brought on a freelance contractor to handle their books in 2014, and as Manish G. described it, “the job was just too much for this individual. Most of our payroll taxes were filed incorrectly, and there was no easy way for a non-expert to figure out how to solve that mess.”

When they let the contractor go, they had no one to process payroll, which put them “in a bind with our clients, vendors, and employees.” The cascade effect of payroll errors extends far beyond the immediate penalty—it damages relationships and creates operational chaos.

Compliance risk. Payroll tax regulations change constantly. Paid sick leave laws, minimum wage adjustments, and new reporting requirements—staying current requires ongoing attention. If you’re operating in multiple states (and most growing consulting firms are), you’re juggling different rules for each jurisdiction.

Miss a compliance deadline? You’re looking at automatic penalties plus interest. One consultant told us she nearly missed a major tax deadline because “nobody was properly tracking compliance requirements across their multi-state client base.” She caught it with three days to spare—pure luck, not system design.

Growth limitations. This might be the most expensive hidden cost of all. DIY payroll systems that work for five employees often can’t scale to fifteen. The complexity multiplies faster than most people expect.

We saw a strategy consulting firm pass on a $200,000 contract because their financial infrastructure couldn’t handle the project’s complexity. They needed detailed time tracking, milestone billing, and multi-phase budget management—and their current systems couldn’t deliver it. How do you calculate the cost of that missed opportunity? It’s not just the immediate $200,000 revenue loss. It’s the relationship, the referrals, the portfolio piece, and the team growth that the contract could have funded.

The Managed Service Investment

So what does professional payroll management actually cost—and what do you get?

For most consulting firms, managed payroll costs $400-800 per week, depending on team size and complexity. Let’s call it $600 per week, or $2,400 per month. That sounds like a lot compared to $50 DIY software, right?

But here’s what that investment includes: Multi-state payroll processing. All federal, state, and local tax filings. New hire onboarding paperwork. Termination documentation. Benefits administration coordination. Unlimited consultation when questions arise. Technology integration with your existing systems. And—this matters—an error guarantee.

Paul, who runs an investor-backed business, put it this way: “We just finished our 2022 audit, and the auditors found exactly zero errors by S6. Not only have they been mistake-free, but S6 has also been proactive at catching mistakes I’ve made or seeing challenges coming down the pike.”

Zero errors. In an entire year. Across hundreds of transactions.

Now let’s talk ROI. When you move to managed payroll, you reclaim fifteen to twenty hours monthly. At a $200 hourly billing rate, that’s $3,000-4,000 in recovered revenue potential. Every month. That’s $36,000-48,000 annually in time you can now spend on actual client work instead of tax forms.

Subtract your $2,400 monthly investment from your $3,000-$4,000 in reclaimed billable time. You’re coming out $600-1,600 ahead each month—before we even account for the errors you’re avoiding or the growth opportunities you can now pursue.

Betsy described the shift perfectly: “System Six has done wonders for my stress level to feel like this is all now taken care of with a professional partner.”

But what if you have a simple payroll? Just a few employees, straightforward salary structure, single state? Even “simple” payroll requires compliance with regulations, quarterly filings, year-end reconciliations, and new-hire paperwork. And here’s the thing about payroll—it never stays simple. You hire someone remote. You add a contractor. You expand to a new state. Suddenly, your “simple” payroll has sixteen different compliance requirements you need to track.

Making the Decision

Here’s how to figure out which approach makes the most financial sense for your specific situation.

Ask yourself these five questions:

- What’s your effective hourly rate for billable work?

- How many hours monthly do you currently spend on payroll (track it honestly for one month)?

- How confident are you in multi-state compliance as you grow?

- What’s the cost if you make a single mistake?

- What would you actually do with fifteen hours back each month?

Now do the real math. Multiply your hours by your hourly rate. Add your error risk (even one mistake annually averages $845). Factor in the growth opportunities you’re missing because you’re stuck in administrative tasks instead of business development.

Compare that total to your managed service investment.

Most consulting firms discover the managed approach pays for itself three to four times over. And that’s before accounting for peace of mind, which turns out to be worth more than most people expect.

What Your Business Could Look Like

Marcus eventually switched to managed payroll. The decision cost him $650 monthly—but gave him back twelve hours, eliminated the 3 AM worry about whether he’d filed correctly, and freed him to take on two new clients he’d previously had to decline. His “savings” from DIY payroll had actually been costing him roughly $40,000 annually in lost opportunity.

The question isn’t whether you can do your own payroll. You’re intelligent, capable, and perfectly able to figure out tax forms. The question is whether you should, given what that choice costs you in time, risk, and opportunity.

Track your actual payroll hours for the next month. Include everything—data entry, research, troubleshooting, verification, and tax filing preparation. Calculate what those hours would be worth if you spent them on client work instead. Then ask yourself: Is DIY payroll actually the cost-effective choice?

What would your business look like if payroll were handled—correctly, completely, and automatically—while you focused on what you actually get paid to do?

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps consulting firms streamline their financial operations. We specialise in providing technology-driven financial management solutions that enable owners to focus on growing their businesses without worrying about payroll, compliance, or cash flow. Our team of 35+ professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. with a 9.5/10 NPS score. Learn more at www.systemsix.com.

by Chris Williams | Nov 24, 2025 | Blog

Sarah checks her phone at 2 am. Again. The email notification glows in the darkness—payroll processing tomorrow, and she’s lying there doing mental math. Three big projects wrapping up this month, invoices going out next week, and payments probably 30 days after that. Maybe 45. Will the timing work? She’s got twelve consultants counting on her, and honestly, she’s not sure.

Here’s the thing: Sarah’s firm is busy. Really busy. Her team’s booked solid through next quarter. But busy doesn’t mean healthy, and revenue doesn’t always mean cash. Most consulting firms track the big numbers—total revenue, total expenses, what’s in the bank right now. But those numbers are like checking your destination on a map without looking at the route. You know where you want to end up, but you’ve got no idea if you’re about to drive off a cliff.

What consulting firms actually need are the metrics that work like vital signs—the ones that tell you what’s happening right now and what’s about to happen next. Think of monthly metrics as your firm’s pulse, blood pressure, and temperature all rolled into one dashboard. They don’t just show you where you’ve been. They show you where you’re headed in time to do something about it.

Why Monthly Matters (More Than You Think)

There’s a paradox at the heart of consulting businesses. You can feel swamped with work and still be heading toward a cash crisis. You can have a full pipeline and terrible margins. You can be growing revenue while profitability circles the drain.

The culprit? Timing gaps. What happens this month doesn’t show up in your bank account for 30, 60, or sometimes 90 days. That project you’re grinding on right now? The one keeping your team busy nights and weekends? You won’t see that money for at least a month after you finish the invoice and wait for payment. By the time you realize a problem exists, you’re already deep in it.

One System Six client discovered their utilization rate was actually 60%—despite everyone feeling overwhelmed. Turns out, their team was spending enormous chunks of time on internal meetings, administrative tasks, and “staying busy” rather than billing hours. They felt busy because they were. They just weren’t busy with the right things. Monthly tracking caught this pattern early enough to fix it before it became a hiring problem, a pricing problem, and eventually a survival problem.

Here’s what annual reports can’t do: they can’t warn you. They’re like finding out you had the flu last February. Interesting, sure. Useful? Not so much. Monthly metrics are different. They catch trends when you can still steer. They show you the storm clouds before the rain hits.

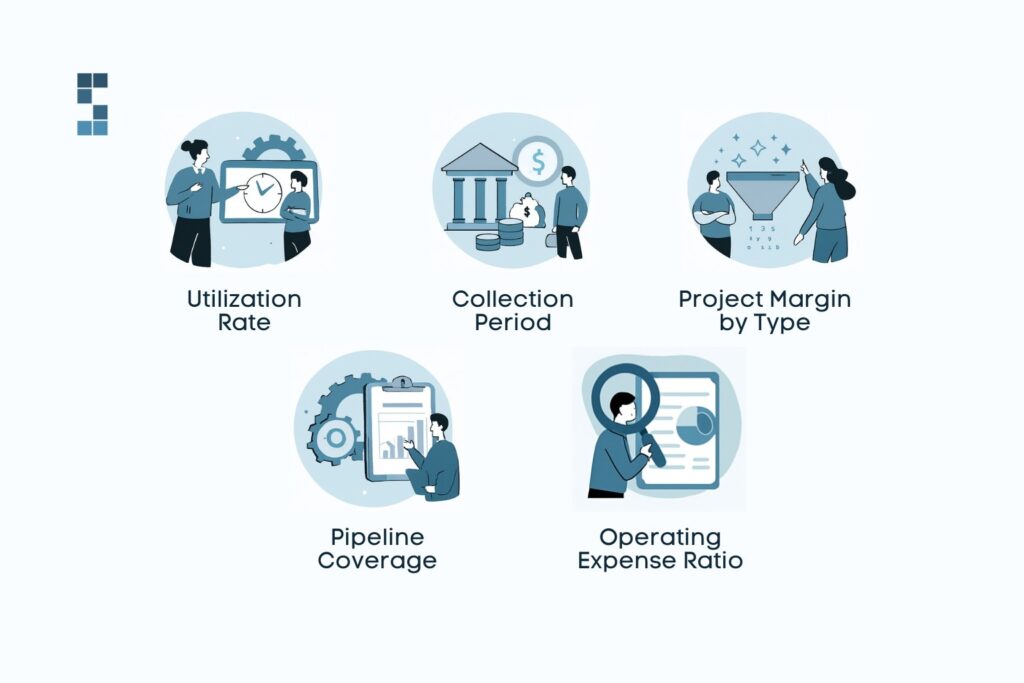

The Five Monthly Metrics That Actually Matter

Not all metrics deserve your attention. Some are vanity numbers that make you feel good without telling you anything useful. Others are so granular they bury the signal in noise. These five hit the sweet spot—they’re simple to track, hard to game, and they tell you what you actually need to know.

Utilization Rate: Are You Actually Selling Your Inventory?

Your utilization rate is simple math: billable hours divided by available hours. But it’s anything but simple in what it reveals. For consulting firms, time is inventory. You can’t stockpile it. You can’t carry it forward. Every hour that passes without being billed is revenue that vanishes forever.

Good looks like 70-80% for most consulting firms. Higher than that, and you risk burnout and zero capacity for growth. Lower than that and you’re not converting your team’s availability into revenue. The real value shows up in the trend. When you slip from 75% to 65% over three months, you’ve got a problem forming. Maybe your pipeline’s thinning. Maybe your pricing’s off, and projects are taking longer than they should. Perhaps you’re overstaffed for current demand. The metric doesn’t tell you what’s wrong—it just tells you to look closer, right now, while you can still fix it.

Collection Period: The Silent Cash Flow Killer

This one’s measured in days from invoice to payment, and it creeps up on you like moss on a tree. Thirty days become 35, then 40, then 45. Before you notice, you’re essentially acting as your clients’ bank, financing their operations with your own cash flow.

The pattern’s predictable: clients push payment. You don’t want to be “that vendor” who nags about money. So you wait. They pay eventually. But “eventually” means you’re covering payroll, contractor payments, and operating expenses out of pocket while your clients hold onto their cash. One consulting firm owner partnered with System Six and watched their average collection period drop from 45 days to 22. “Our cash flow transformed overnight,” they said. Not because their clients suddenly became more ethical—but because automated reminders and better invoicing discipline changed the game.

Project Margin by Type: Not All Revenue Is Good Revenue

This metric takes your revenue and subtracts everything—direct costs, contractor fees, and crucially, that allocated overhead everyone forgets about. Partner time. Coordination calls. Proposal development. All of it. Then you break it down by service line or project type.

What you discover can be shocking. That showcase project you love talking about at networking events? The one with the impressive brand-name client? It might be breaking even once you factor in all the oversight time and scope creep. Meanwhile, those mid-sized projects you barely mention might be printing money. Jamie, an IT consultant, had this exact revelation: “We realized our technology implementation services were far more profitable than our strategic assessments. We reorganized our marketing to emphasize implementation and grew that service line by 40% within six months.”

The insight’s only available if you’re tracking project margins monthly. Annually, the patterns blur together. Monthly, they jump out at you in time to adjust your business development focus.

Pipeline Coverage: Today’s Prospects Are Next Quarter’s Payroll

Pipeline coverage asks a simple question: Do you have enough qualified opportunities to hit your revenue targets three months from now? The math’s straightforward—take your qualified pipeline, divide it by your monthly revenue target, and multiply by your close rate. You want 3x coverage because not everything closes.

This metric’s your early warning system for feast-and-famine cycles. When coverage drops below 2x, you know you need to invest in business development now, not later when panic sets in. When it climbs above 4x, you’ve got breathing room to focus on delivery and operations. One System Six client put it perfectly: “Instead of reactive hiring when we’re already drowning in work, we now can see three months ahead when we’ll need additional capacity in specific practice areas.”

Operating Expense Ratio: Are You Scaling or Just Getting Busier?

Divide your fixed costs by revenue. For most consulting firms, healthy looks like 40-60%. This metric tells you whether you’re scaling efficiently or just layering on overhead as fast as you’re adding revenue.

The ratio should decrease as you grow. That’s what scaling means—spreading fixed costs across more revenue. If your ratio’s climbing, you’re adding expensive overhead faster than you’re growing revenue. You’re building a more complex business without becoming more profitable. Monthly tracking catches this before it becomes structural.

From Spreadsheet Chaos to Dashboard Clarity

Here’s how it used to work: Saturday morning, pot of coffee, laptop open on the kitchen table. Pull data from your time tracking system. Export from QuickBooks. Wrestle it all into Excel. Build formulas. Cross-check numbers. Fix errors. By Sunday afternoon, you’d have an already outdated report and a weekend you’d never get back.

“Our financial reporting used to take 3-4 days each month,” a consulting firm owner shared after partnering with System Six. “Now it’s largely automated, providing real-time insights through dashboards we can check anytime.”

That’s the transformation. You stop compiling and start reviewing. Your time-tracking, project management, accounting system, and CRM all automatically feed into one dashboard. Monday morning, fifteen minutes, you know exactly where you stand. Utilization’s trending down? You see it. Collection period creeping up? There it is. Project margins shifting? Clear as day.

It’s like the difference between manually calculating your car’s fuel efficiency with pen and paper versus glancing at the dashboard. At the same time, you drive: the same information, but a completely different experience.

And here’s what nobody talks about: the psychological shift. “Good financial reporting didn’t just improve our profitability—it reduced our stress,” another consulting owner explained. “Instead of lying awake wondering if we’re making the right decisions, we now know where we stand and are headed.”

That’s worth more than the time savings. That’s worth more than the improved margins. That’s the difference between hoping your business is healthy and knowing it is.

Getting Started Without the Overwhelm

You don’t need to track everything on day one. Start with the two metrics that address your biggest worry right now, if you’re anxious about cash: track the collection period and pipeline coverage. If you’re worried about profitability, focus on project margins and utilization rate.

Master those for a month. Get comfortable with the rhythms, the patterns, what normal looks like for your firm. Then add complexity gradually. The goal isn’t a perfect measurement system—it’s a useful one.

Set up automated data feeds so you’re reviewing insights, not hunting for numbers across five different systems. Make Monday morning your metric ritual. Fifteen minutes, coffee in hand, dashboard open. What’s trending up, what’s trending down, what needs attention this week?

These aren’t just numbers on a screen. They’re your early warning system. They’re your strategic compass. They’re the difference between reactive scrambling and confident decision-making. Many consulting firms outsource this entire setup and ongoing tracking because it’s faster, more reliable, and, frankly, more cost-effective. After all, they’d rather spend their time on client work than building financial dashboards.

Your Financial Pulse, Strong and Steady

You can’t manage what you don’t measure. But you also don’t need to measure everything. These five metrics—utilization rate, collection period, project margin, pipeline coverage, and operating expense ratio—give you the visibility to make confident decisions instead of hopeful guesses.

“System Six has done wonders for my stress level,” one client told us. That’s what clarity does. It turns 2 am anxiety into Monday morning confidence. It turns scattered data into strategic insight. It turns “I hope we’re okay” into “I know exactly where we stand.”

What would change in your consulting firm if you had complete clarity on these five metrics every Monday morning? What decisions would you make differently? What problems would you catch early? What opportunities would you spot before your competitors?

Maybe it’s worth exploring whether automated financial tracking could give you back your weekends and your peace of mind. Your firm’s already generating all this data. The question is whether you’re using it to get ahead—or just falling further behind.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm specializing in consulting and professional service businesses. Our team of 40+ professionals brings an average of 10+ years of accounting experience to every client relationship, serving over 175 companies across the U.S. We operate on a fixed weekly fee model with no long-term contracts because we believe in earning your business through consistent value delivery. Learn more at www.systemsix.com.

by Chris Williams | Nov 17, 2025 | Blog

You budgeted $800 for bookkeeping this month. The invoice says $1,847.

Your bookkeeper spent extra time reconciling Q4, tracking down missing receipts, and preparing for tax season. All legitimate work. All billable hours. And all completely unpredictable when you were planning your monthly cash flow.

Sound familiar?

Most consulting firm owners don’t realize their “affordable” hourly bookkeeper might actually be costing them more than predictable subscription pricing—not just in dollars, but in stress, time, and strategic opportunity. I’ve watched dozens of consulting firms struggle with this exact decision, and here’s what I’ve learned: the pricing model you choose affects way more than your monthly costs.

Let’s break down what each model actually costs you, what the invoices don’t tell you, and how to calculate which one makes sense for your firm.

The Real Difference Between Hourly and Subscription Pricing

Here’s how hourly bookkeeping typically works. You pay somewhere between $30 and $300 per hour, depending on your bookkeeper’s expertise and your location. Sounds straightforward, right?

But here’s the catch. You’re not paying for results—you’re paying for time spent. More transactions this month? Higher bill. Complicated reconciliation? Higher bill. Does your bookkeeper need to learn your new project management software? You’re paying for their education.

One strategy consultant told me he spent every Monday morning sorting through the previous week’s transactions. “That’s half a day I wasn’t spending with clients or developing new business,” he said. “It was costing me a new client every quarter.” When he finally looked at his bookkeeper’s hours, he realized he was also paying them to figure out the mess he’d created over the weekend.

Subscription pricing flips this model entirely. You pay a fixed weekly or monthly fee based on your business’s complexity—not the hours it takes. At System Six, that typically runs $300-$800 per week, depending on firm size. But here’s what stays the same: whether it’s a simple month or a complex quarter-end, your cost remains the same.

The psychological shift is massive. With hourly pricing, you’re buying time. With subscription pricing, you’re buying outcomes. You stop thinking “Should I bother my bookkeeper with this question?” and start thinking “What financial insights do I need to grow my business?”

What the Invoice Doesn’t Tell You

Let’s talk about costs that never appear on your bookkeeping invoice but still drain your bank account.

First, there’s scope creep—every “just a quick question” email. Every phone call is to clarify a transaction—every follow-up about a vendor payment. With hourly pricing, all of that gets metered. You learn to ration your communication, which means you make decisions without complete information. How much does that cost you?

Then there’s the learning curve premium. When you pay hourly, you’re literally paying your bookkeeper to figure out your business. They need to understand your revenue model, project structures, contractor relationships, and multi-state compliance requirements. That’s not a quick conversation—that’s months of discovery billed by the hour.

Here’s a real example that illustrates the hidden costs. One System Six client discovered they’d been making a simple bookkeeping error that was costing them $700 in unnecessary bank fees each month. That single mistake was eating $8,400 annually—way more than the difference between hourly and subscription pricing.

But the highest hidden cost? Your time.

Most consulting firm owners spend 15-20 hours monthly on financial administration. At typical consulting rates of $200-500 per hour, that represents $3,000-10,000 monthly in lost billable opportunity. Mark, who runs an environmental consulting firm, reclaimed 10+ hours weekly after switching to automated subscription services. His firm grew 40% the following year. Same team. Same expertise. Just way less time categorizing expenses on Sunday nights.

And speaking of Sunday nights—let’s talk about the mental bandwidth drain. There’s this background anxiety that comes with unpredictable costs. You can’t confidently forecast your financial management expenses. You hesitate before calling your bookkeeper. You make decisions in a fog of incomplete information.

As Betsy, who runs an investor-backed business, put it: “System Six has done wonders for my stress level to feel like this is all now taken care of with a professional partner.”

That peace of mind doesn’t show up on any invoice. But it absolutely affects your bottom line.

When Hourly Pricing Actually Makes Sense

Look, I’m not here to tell you subscription pricing works for everyone. It doesn’t.

Hourly pricing can make perfect sense for one-time projects—historical cleanup, system migration, special audit preparation. If you need eight hours of work once and you’re done, paying hourly is straightforward and cost-effective.

It can also work for genuinely simple businesses. If you’re a solo consultant with few transactions and only need 2-3 hours monthly, an hourly rate might be your best bet. Some seasonal companies with dramatically different needs month to month might also benefit from the flexibility.

And if you’re doing most of the work yourself and only need spot help? Hourly can work fine.

But here’s the reality check most consulting firms miss: you’re probably more complex than you think. Project-based revenue? That’s complex. Multi-state operations? Complex. Contractor management? Complex. Growth aspirations that require investor reporting? Definitely complex.

I’ve watched consulting firm owners convince themselves they’re simple because they want to save on bookkeeping costs. Then they hit a growth inflection point and realize their “affordable” hourly bookkeeper can’t scale with them. The transition costs way more than if they’d just started with the right model from the beginning.

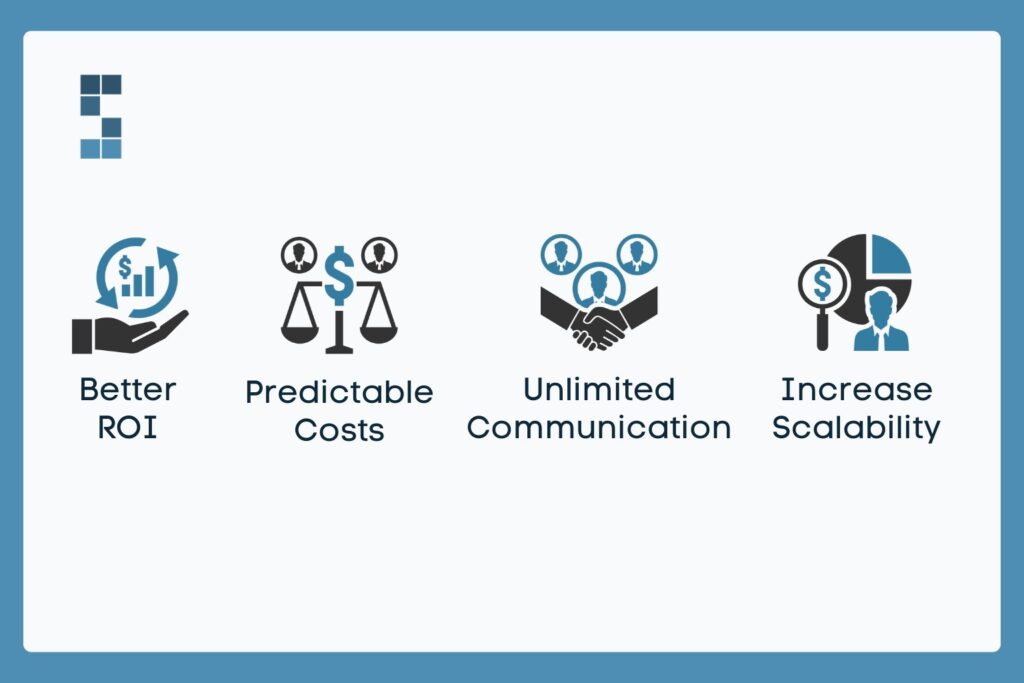

The Subscription Advantage: Predictability Meets Performance

Here’s where subscription pricing really shines for growing consulting firms.

Budget certainty changes everything. You know your costs 12 months in advance—no surprise bills during busy seasons. Your cash flow forecasting actually works. One client told us, “For any internal NPS tracking, please mark us down as an 11/10. Your team is awesome, proactive, and exactly what we need.”

But the real advantage is unlimited communication. You stop watching the meter. You ask the questions you need to ask. Strategic advisory becomes included, not billed separately. Your bookkeeper transforms from a vendor you’re afraid to bother into a true partner invested in your success.

And then there’s scalability. Your business grows from $2M to $8M—your transaction volume triples. You add multi-state payroll. With hourly pricing, your costs explode. With subscription pricing? They stay predictable because the model was designed to scale with you.

The ROI is measurable. System Six’s consulting clients typically see 300%+ first-year returns, with payback periods of just 2-3 months. They reclaim 15-20 hours monthly for billable work. One strategy consulting firm was spending 20 hours monthly on financial administration. At their owner’s $ 200-per-hour rate, that represented $4,000 in monthly opportunity cost. After implementing automated subscription systems, they reduced this to 3 hours per month—a $600 time investment.

The math is straightforward. They saved $3,400 per month in recovered billable time while paying $800 monthly for the system. That’s a 325% return on investment before you even consider error prevention or growth opportunities.

And the results speak for themselves: 9.5/10 NPS score across 175+ clients, 90%+ retention rate among consulting firms. These aren’t companies sticking around because they’re locked into contracts—System Six operates on a fixed weekly fee with no long-term commitments. They stay because the value is undeniable.

Run Your Own Numbers

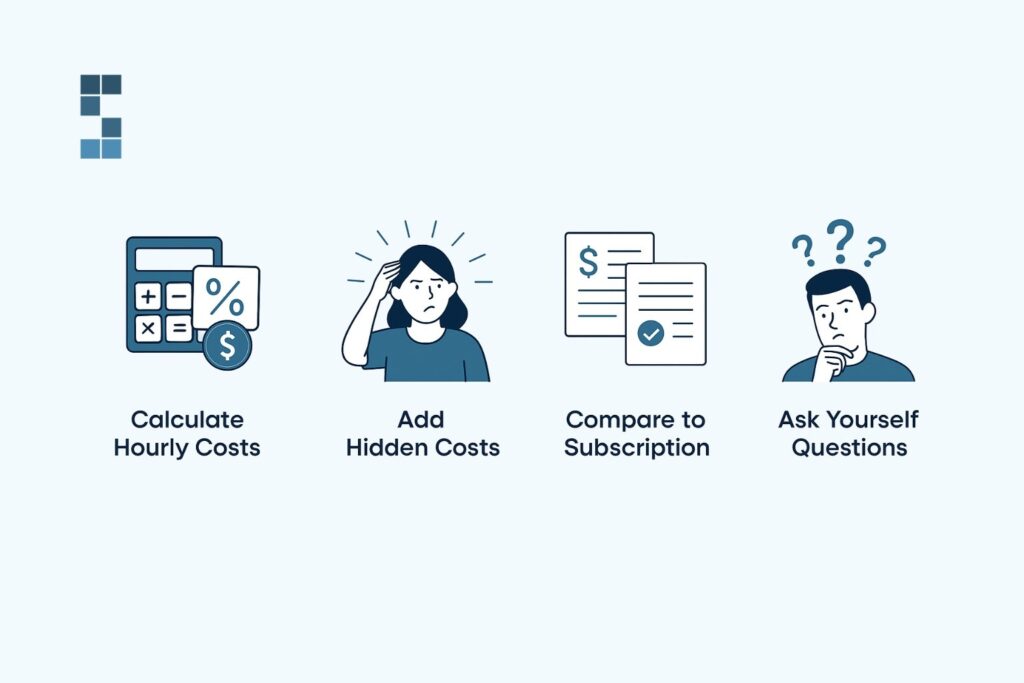

Ready to figure out which model actually costs you less? Start here.

Calculate your actual hourly costs over the last 12 months. Add up all the bookkeeping invoices and divide by 12. Don’t forget those surprise bills from quarter-end or tax season. That’s your real monthly average.

Now add the hidden costs. How many hours did you spend on financial tasks last month? Multiply that by your effective hourly rate. Add any costs from errors, missed deadlines, or cash flow issues. Be honest about what those Sunday nights cost you in family time and mental health.

Compare that total to subscription pricing. What would a fixed monthly fee run? What services are included? Are there communication limits? Is strategic guidance part of the package?

Finally, ask yourself the hard questions. How often do you hold back from calling your bookkeeper because you’re worried about the cost? What client work could you complete with 15-20 extra hours each month? What does cash flow unpredictability cost you in stress and missed opportunities?

The answers might surprise you.

The Bottom Line on Pricing Models

Here’s what I want you to understand: this isn’t really about which model is cheaper on paper. It’s about which delivers better ROI for your specific situation.

For consulting firms generating $1M-$20 in revenue, subscription pricing typically delivers lower total cost AND better outcomes. The predictability alone is worth the investment. The unlimited communication changes how you use financial information. The scalability means you’re not switching systems every time you hit a growth milestone.

But don’t take my word for it. Calculate your actual all-in costs over the last 12 months. Include your time, your stress, your lost opportunities. Then compare that reality to what subscription pricing would actually run.

The question isn’t whether you can afford subscription pricing. It’s whether you can afford to keep losing billable hours and sleep to financial administration.

If you’re spending more than 10 hours monthly on financial tasks, it might be time to reconsider your pricing model. The fixed weekly fee model was explicitly designed for consulting firms tired of unpredictable costs and weekend bookkeeping sessions because you became a consultant to solve complex client problems—not to become an amateur accountant wrestling with reconciliations on Sunday nights.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm specializing in consulting and professional service businesses. Our team of 40+ professionals brings an average of 10+ years of accounting experience to every client relationship, serving over 175 companies across the U.S. We operate on a fixed weekly fee model with no long-term contracts because we believe in earning your business through consistent value delivery. Learn more at www.systemsix.com.

by Chris Williams | Nov 10, 2025 | Blog

Sarah almost missed the most significant opportunity of her consulting career.

A potential client wanted to sign a six-month retainer worth $180,000—a dream project. Perfect fit. But Sarah couldn’t say yes. Why? She had no idea if she could actually afford to hire the two consultants she’d need to deliver the work. Her financials were two months behind, her cash flow was a mystery, and her “forecasting” consisted of hoping things worked out.

The client went elsewhere.

Here’s the thing—Sarah’s brilliant at helping her clients navigate complex strategy decisions. She can spot market trends six months before they hit. But when it comes to her own firm’s finances? She’s flying blind. And she’s not alone.

You didn’t start your consulting firm to become a financial expert. You started it because you’re exceptional at what you do. But here’s the uncomfortable truth: 2025 is separating consultants who understand their numbers from those who are just really good at what they do. The finance landscape is shifting faster than ever, and the firms that adapt will thrive while others struggle.

Let me show you the seven trends that are reshaping consulting finance right now—and more importantly, what you can actually do about them.

AI-Powered Financial Forecasting Replaces Gut Feelings

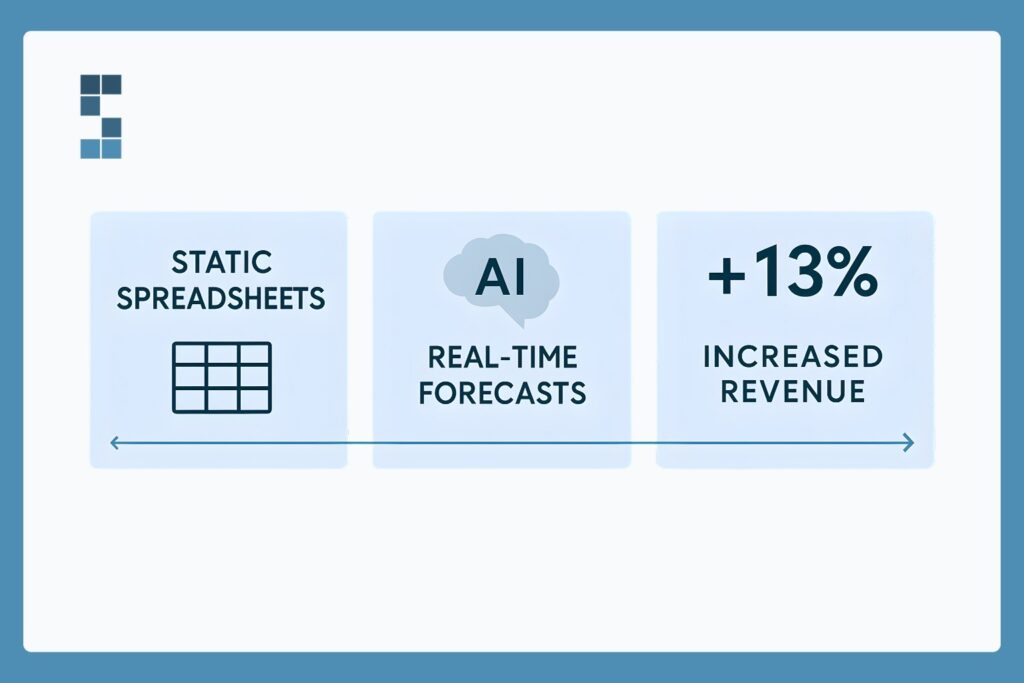

Spreadsheets are dead.

Okay, that’s dramatic. But the annual budget spreadsheet you labored over last December? It was outdated by February. The consulting business moves too fast for static yearly projections. You land a new client, a project gets delayed, someone quits—suddenly, your carefully crafted budget is fiction.

AI and automation are transforming forecasting from annual guesswork to realtime visibility. Instead of asking “What did we think would happen this year?” you can now ask “What’s likely to happen over the next thirteen weeks based on everything happening right now?”

Vincent D., who runs a consulting firm in Bellevue, worked with his finance team to develop a cash forecasting tool that integrates with his accounting system. The result? As he puts it, the tool “significantly improves the speed and accuracy of our forecasting process.” His team went from spending hours manually updating projections to having them refresh automatically.

Companies using AI for predictive analytics are seeing up to 13% increases in revenue. Why? Because they can see opportunities and risks before they fully materialize.

How to prepare: Start with basic automated cash flow tracking. You don’t need to forecast five years out—begin with a simple thirteen-week cash flow projection that updates monthly. Focus on accuracy over sophistication.

Realtime Financial Dashboards Become Non-Negotiable

When was the last time you actually knew your realtime cash position?

Most consultants wait until the month-end to find out how they’re doing. But month-end reports are like reading yesterday’s weather forecast—interesting, but not particularly useful for making decisions today.

The shift is toward continuous visibility. Alecia K. from Seattle had an emotional reaction when she first saw realtime financial reporting. She describes seeing “projected cashflow integrated with realtime QuickBooks” and admits, “I had tears come to my eyes.” That’s the power of actually seeing what’s happening with your money in real time.

Think about it. You can check your firm’s cash position from your phone between client meetings. You can see which invoices are overdue, which projects are most profitable, and whether you’re on track for the quarter—all updated continuously as transactions occur.

How to prepare: Implement cloud-based systems that connect your bank accounts, invoicing, and expenses. Start with basic dashboards showing cash position, accounts receivable aging, and profitability trends before building out more complex analytics.

Project-Level Profitability Tracking Goes Mainstream

Here’s a question that should be easy to answer: Which of your clients actually makes you money?

Lots of consultants can’t answer that. They know their overall revenue and that they’re profitable, but they don’t know that Client A is highly profitable. At the same time, Client B barely breaks even after accounting for all the hours and complexity involved.

The shift is from overall revenue tracking to project-level economics. When you can see profitability by project, client, or service line, everything changes. You start saying yes to the right opportunities and no to the wrong ones.

One consulting firm owner shared that after gaining this visibility, his firm grew 40% the following year while maintaining the exact administrative headcount. He could finally see which types of projects to pursue and which to avoid.

How to prepare: Integrate your time tracking system with your financial software. Even basic project-level tracking reveals patterns you’ve been missing. Start by categorizing revenue and direct costs by project, then gradually add sophistication.

Cash Flow Management Trumps Revenue Growth

Revenue is vanity. Cash flow is sanity.

You can be profitable on paper and still fail if you can’t make payroll. The consulting business is particularly vulnerable to this because there’s often a lag between delivering work and getting paid. You’ve got salaries going out every two weeks while client payments trickle in on Net 30 or Net 60 terms.

Shane B., who owns a dental office in Tacoma, talks about how his financial partner helped him “focus on the business, all the while trusting things taking place on the back-end.” That peace of mind comes from knowing your cash flow is actively managed, not just hoped for.

Cash flow is like oxygen for your business—you don’t think about it until it’s gone. And by then, it’s usually too late.

The firms winning in 2025 are building strategic cash flow forecasting that looks 12 to 18 months ahead. They’re modeling scenarios for growth investments, seasonal fluctuations, and hiring decisions to ensure they never face unpleasant surprises.

How to prepare: Build a rolling 12-month cash flow model that accounts for your payment timing patterns. Factor in seasonal variations—many clients pay more slowly during holidays or summer. Create decision triggers based on cash position.

Automated Financial Operations Free Up Strategic Time

You didn’t start your consulting firm to categorize expenses.

But how much time did you spend on financial admin last month? Entering transactions, chasing invoices, categorizing expenses, and reconciling accounts. Add it up. Now multiply that by your billable rate. That’s your opportunity cost.

The automation revolution is here, and it’s transforming everything from manual entry to AI-powered transaction processing. Firms are reclaiming 15 to 20 hours per month that were previously lost to administrative tasks. That’s time redirected to billable work, business development, or—radical thought—your actual life.

Paul, who runs an investor-backed business, raves about his financial team being “proactive at catching mistakes I’ve made” and notes that auditors found “exactly zero errors.” Zero. That’s the difference between manual processes and automated systems with expert oversight.

How to prepare: Start by automating the most painful tasks first. Bill pay, invoicing, and expense categorization offer immediate returns. Don’t try to automate everything at once—master one system before adding complexity.

Multi-State Compliance Complexity Increases

Remember when everyone worked in one office and compliance was straightforward?

Remote work changed everything. Now you might have consultants in five different states, clients in ten others, and suddenly you’re navigating a multi-state tax nightmare. Nexus rules, contractor classification, remote payroll compliance—get any of it wrong and it’s expensive.

The number of full-time independent consultants grew to 27.7 million in 2024, and many consulting firms are hiring across state lines without understanding the compliance implications. Each state has different rules about when you need to withhold taxes, pay unemployment insurance, and register your business.

Julie R., whose company works with a sophisticated accounting team, praises them for being “attentive to the smallest details around our complex accounting needs.” That attention to detail isn’t optional anymore—it’s essential for avoiding costly mistakes.

How to prepare: Audit your current compliance exposure. Where are your team members located? Where are your clients? Do you have nexus in states where you’re not registered? Consider working with specialists who understand the specific compliance issues in consulting.

Financial Advisory Replaces Basic Bookkeeping

Consultants don’t need bookkeepers anymore. They need strategic financial partners.

The evolution is from recording transactions to providing CFO-level insights. You need someone who can help you make decisions about hiring, pricing, expansion, and investment—not just someone who can tell you what happened last month.

Here’s a weird connection: What do beehives and modern consulting firms have in common? Both need strategic intelligence flowing from the front lines to leadership. Bees constantly communicate about threats and opportunities. Your financial systems should do the same.

JT C. captures this perfectly when he describes his financial team providing “an outside view, a 35,000-foot look at what you’re doing that isn’t possible from the inside out.” He reflects that if he’d made the switch sooner, his “business outcomes would have been SUBSTANTIALLY DIFFERENT.”

That’s the shift. Financial management isn’t about compliance and accuracy anymore—though those remain essential. It’s about gaining a strategic advantage through better visibility and more intelligent decisions.

How to prepare: Look for financial partners who understand the challenges of consulting. They should speak your language, understand your business model, and provide insights that help you grow—not just accurate books.

What Happens Next

These seven trends aren’t isolated developments. They’re interconnected shifts toward data-driven financial management that reward firms able to see around corners.

Remember Sarah from the beginning? She didn’t make that mistake twice. She implemented realtime financial dashboards, built rolling forecasts, and automated her financial operations. Six months later, an even bigger opportunity came along—and this time, she said yes immediately. She knew exactly where her cash flow stood, what she could afford to hire, and how the project would impact her bottom line.

That’s what 2025 rewards: consultants who bring the same strategic clarity to their own finances that they provide to clients.

Here’s what you can do this week. Track your time on financial tasks for the next seven days. Every minute spent categorizing transactions, updating spreadsheets, or chasing down numbers. Calculate what that time costs at your billable rate. Then identify your most prominent financial blind spot—the question about your business you can’t easily answer.

Start there.

What could your firm achieve if you had the same financial clarity you provide to your clients? The consulting landscape in 2025 rewards those who can see opportunities before they fully materialize and make confident decisions backed by real data.

Your finances shouldn’t be a mystery. They should be your competitive advantage.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 35 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. From accurate bookkeeping to cash flow forecasting, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Nov 3, 2025 | Blog

Maria thought she’d checked every box when she launched her consulting practice. Business license? Done. EIN from the IRS? Check. Liability insurance? Sorted. She even remembered to file her assumed name certificate with the county.

She hadn’t heard about the Corporate Transparency Act.

Neither have most small business owners. And that’s a problem, because this federal law—which took effect January 1, 2024—requires most U.S. companies to file beneficial ownership information with the federal government. Miss the deadline, and you’re looking at penalties up to $500 per day. Let it slide too long, and you could face criminal charges.

Don’t panic. This isn’t as complicated as it sounds. But it does require your attention, and the clock’s already ticking.

What the Corporate Transparency Act Actually Is

Here’s the deal in plain English: The Corporate Transparency Act requires most companies to report who actually owns and controls them. We’re talking names, addresses, dates of birth, and ID numbers for anyone who owns 25% or more of your business or exercises substantial control over it.

Why? The law aims to combat money laundering, tax evasion, and other financial crimes committed through anonymous shell companies. Think drug cartels and international fraud rings hiding behind layers of LLCs.

What does that have to do with your 5-person consulting firm? More than you’d think. The law casts a wide net. It doesn’t distinguish between a legitimate professional services company and a suspicious offshore entity. If you’re incorporated or formed as an LLC, you’re required to file.

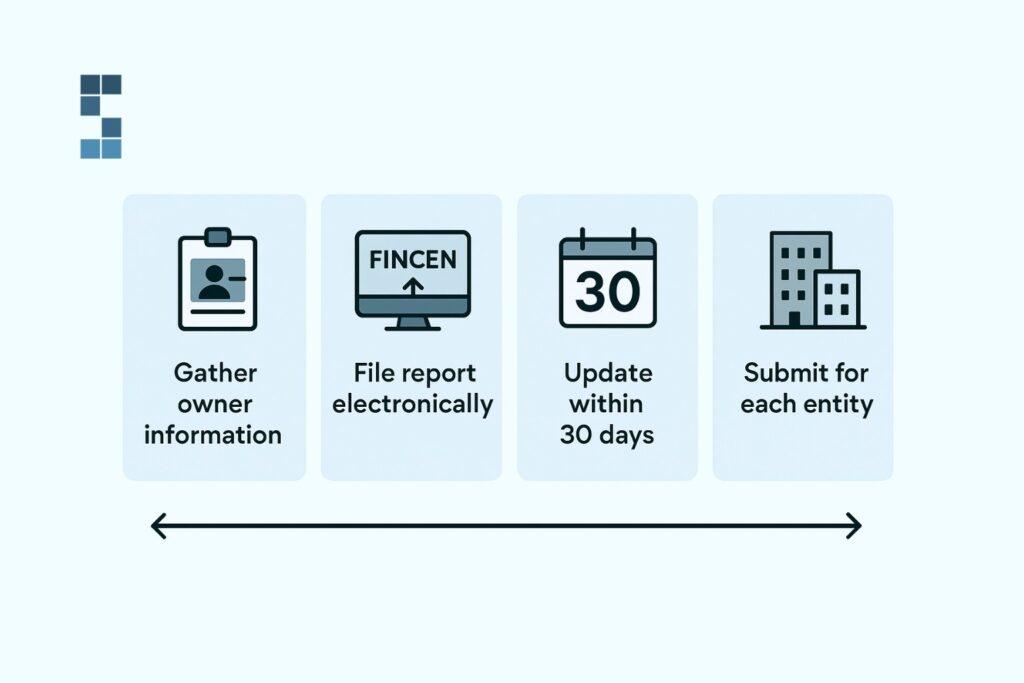

The requirements break down like this: existing companies formed before 2024 have until January 1, 2025, to file their initial report. Companies formed in 2024 get 90 days from formation. New companies formed after January 1, 2025, get just 30 days. The report goes to FinCEN—the Financial Crimes Enforcement Network, part of the U.S. Treasury Department.

So what actually counts as a “beneficial owner”? Anyone who owns 25% or more of your company, or anyone who exercises substantial control. That second part trips people up. If you’re the CEO making all the strategic decisions, but you only own 15%? You’re still a beneficial owner. If you’re a senior officer who could hire or fire the CEO? Beneficial owner.

Who This Actually Affects (and the Exemptions You Should Know)

Let’s start with the default position: you’re probably required to file.

Most small consulting firms fall under this law. LLCs, S-Corps, C-Corps—doesn’t matter. Single-member LLC operating from your home office? Still counts. Three-partner consulting firm with $2 million in revenue? Definitely counts. That boutique strategy practice you launched last year? Yep.

“I’m just a solopreneur” doesn’t exempt you. “We’re too small to matter” won’t save you either.

Wrong on both counts.

The exemptions exist, but they’re designed for a different type of company. Large operating companies with more than 20 full-time U.S. employees, more than $5 million in gross receipts, and a physical office in the United States get a pass. Certain regulated entities—banks, insurance companies, and accounting firms registered with the PCAOB—are exempt too.

Notice who’s missing from that list? Most consultants, advisors, coaches, and professional services firms. Even successful ones. You could be running a thriving $10 million consulting practice with 18 employees and still need to file, because you don’t quite hit that 20-employee threshold.

Here’s a real-world example: You’re running a 3-person strategy consultancy structured as an LLC. You own 60%, your business partner owns 30%, and you gave your first employee 10% as an equity incentive. You both need to report—you and your partner are clearly beneficial owners. Your employee probably doesn’t meet the threshold, since they’re under 25% and don’t exercise substantial control. But you’ll want to verify that, because “substantial control” can be subjective.

What You Need to Do (The Actual Action Steps)

Time’s ticking. For companies formed before 2024, you’ve got until January 1, 2025. That’s not as far away as it feels.

Start by gathering information for each beneficial owner. You’ll need their full legal name (exactly as it appears on their ID), complete address, date of birth, and a government-issued ID. A driver’s license or passport works. You’ll need a clear image or PDF of that ID, too—something readable that shows the ID number.

Then you file electronically through FinCEN’s system—no filing fee, which is a small silver lining. The actual filing takes 30-45 minutes once you’ve gathered everything. It’s not the filing that’s hard—it’s knowing you need to do it in the first place.

Here’s where it gets tricky: you need to keep this information current. Change your address? You’ve got 30 days to update your filing. Bring in a new partner? Thirty days. Does the existing partner sell their stake? Same 30-day window. Miss that deadline and you’re back to penalty territory.

The complexity multiplies if you’ve got multiple entities. Holding company that owns your operating company? You’re filing for both. Consulting firm with a separate LLC for your coaching business? Two filings. Each entity needs its own report, and each needs to be kept current.

This is where lots of consulting firm owners realize their time is better spent elsewhere. One System Six client put it perfectly: “System Six handles everything so professionally that I never worry about the financial side anymore.” That includes staying on top of compliance requirements like these—the kind that can sneak up on you if you’re focused on serving clients and growing your practice.

What Happens If You Don’t Comply

The stakes are real.

Civil penalties start at $500 per day. Miss the deadline by a week? That’s $3,500. Miss it by a month? Over $15,000. And it keeps climbing until you file.

But it gets worse. Criminal penalties can hit $10,000 in fines and up to two years in prison for willful violations. The government didn’t add criminal penalties for fun. They want compliance, and they’ve given themselves serious enforcement teeth.

“I didn’t know about it” won’t protect you. The law doesn’t care whether you heard about the requirement. It cares whether you filed. And “willful” means you knew about the requirement and ignored it. Once you finish reading this article, you know. The clock starts now.

Beyond the direct penalties, there’s practical fallout to consider. Banks are increasingly asking for this information during account opening or loan applications. Investors want to verify beneficial ownership before they write checks. Even routine business transactions can hit snags if you’re not compliant.

Think of it less like filing taxes and more like keeping your business license current. It’s not an annual thing you can batch with your year-end accounting. It’s ongoing, and it requires attention whenever ownership or control changes.

This isn’t meant to scare you. It’s intended to inform you. The actual filing isn’t difficult—it’s straightforward if you’ve got your documents organized. What trips people up is either not knowing about it until they’re past the deadline or knowing about it but putting it off until it becomes a crisis.

How to Handle This Without It Consuming Your Life

Here’s the reality check: you didn’t start a consulting practice to become a compliance expert.

Your time is worth somewhere between $200 and $500 per hour, depending on your specialty and client base. Spend five hours figuring out FinCEN’s filing system, tracking down documents, and stress-testing whether someone qualifies as a beneficial owner. You’ve just donated $1,000 to $2,500 in opportunity cost to the federal government.

You’ve got options.

The DIY approach makes sense if your structure is simple. Single-member LLC with no plans to bring in partners? The filing is straightforward once you know what you’re doing. Budget 2-3 hours to gather documents and complete the filing, plus time to set calendar reminders for any future updates you might need.

But if you’ve got multiple entities, complex ownership structures, or you want the peace of mind that comes from knowing it’s handled correctly? That’s when you bring in professional support.

Good financial partners handle this kind of compliance work as part of their service. As one environmental consulting firm owner noted after working with System Six: “We serve businesses across dozens of service industries and understand the unique requirements for licensing, bonding, prevailing wage, and other industry-specific compliance needs.”

The Corporate Transparency Act joins that list of industry-specific requirements that someone needs to track—the question is whether that someone should be you or a professional who’s already monitoring compliance changes across their entire client base.

Think about it this way: you wouldn’t tell your clients to DIY their strategy work, would you? You’d point out that while they technically could figure it out themselves, their time is better spent on their core business, while you handle the strategic thinking. The same logic applies to your own business operations.

The peace of mind factor is real. One search fund operator put it this way: “System Six has done wonders for my stress level to feel like this is all now taken care of with a professional partner.” That’s the goal—getting compliance requirements off your mental load so you can focus on what you’re actually good at.

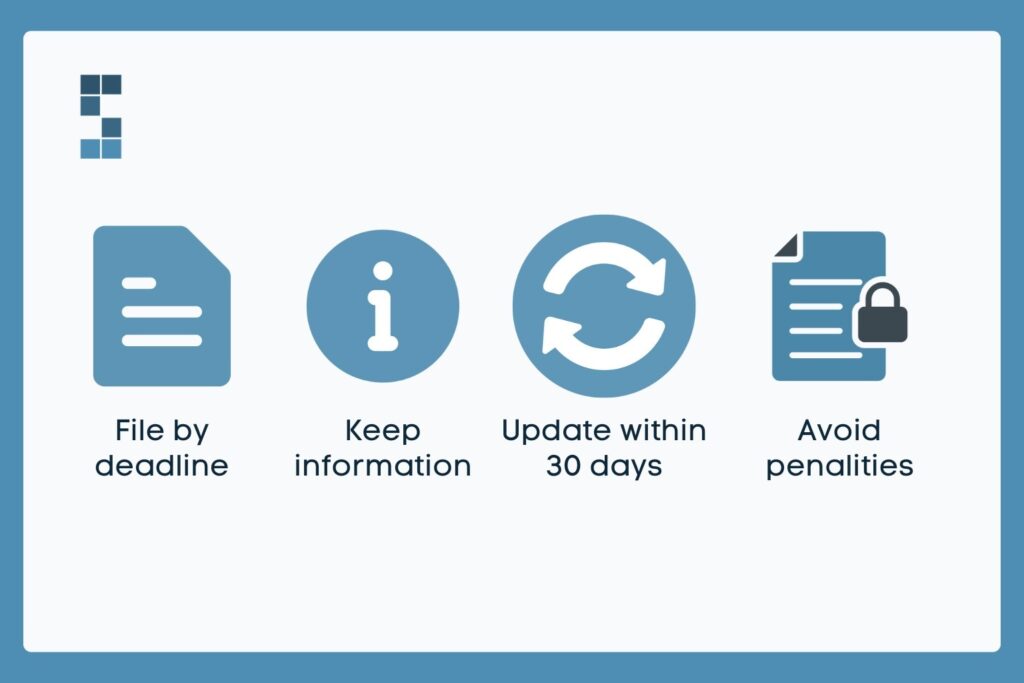

Don’t Let This Derail Your Practice

The Corporate Transparency Act is here. It’s real. It affects you. But it’s also manageable—if you handle it.

File by the deadline. Keep your information current. Update within 30 days when ownership or control changes. Do those three things and you’re fine. Skip them and you’re looking at penalties that start steep and get worse.

Whether you tackle this yourself or bring in professional help, please don’t ignore it. The cost of non-compliance is real, and it’s not worth the risk.

If you’re running a consulting firm or professional services practice and you’re wondering how this fits into your broader compliance picture—or if you’d like to stop spending your weekends figuring out federal filing requirements—that’s precisely the kind of problem firms like System Six solve every day. Over 175 service businesses trust them to handle these details so they can focus on serving clients instead of decoding government regulations.

Do you need to file, or want to make sure you’re handling this correctly? Don’t wait until the deadline is looming. The January 1, 2025, cutoff for existing companies will arrive faster than you think.

And Maria? She filed hers last month. She’s sleeping better now.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, allowing owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance issues. Our team of over 35 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. From accurate bookkeeping to cash flow forecasting, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Oct 22, 2025 | Blog

Sarah stared at the proposal in front of her, calculator in hand. The automated cash flow system would cost her consulting firm $800 per month. That seemed like much money.

But then she started thinking about last month. She’d spent an entire Sunday reconciling accounts because three client payments got misallocated. Her project manager had wasted half a day tracking down expense receipts. And they’d nearly missed a tax deadline.

What Sarah was experiencing is the ROI confusion that costs businesses thousands in hidden expenses every year. She was focused on that $800 monthly fee while completely missing the expensive chaos her “free” system was creating.

Here’s what most business owners don’t realize: ROI isn’t just about what you spend. It’s about what you gain, what you save, and what you avoid losing. When you understand this distinction, the math becomes crystal clear.

The Real Cost of “Free”

Here’s the truth: your manual system isn’t free.

If you’re spending 15 hours monthly on financial tasks—invoicing, reconciling, tracking expenses, chasing payments—and your effective hourly rate is $200, you’re looking at $3,000 monthly in hidden costs. That’s $36,000 annually, just in your time.

But it gets worse.

One business owner discovered he was paying $700 in unnecessary bank fees each month because poor cash flow tracking led him to trigger overdraft fees repeatedly. That’s $8,400 annually—enough to pay for sophisticated tools and still come out ahead.

Then there are the error costs. Late payment penalties. Compliance fines. Client relationships were damaged due to inconsistent billing. These aren’t theoretical—they’re real money walking out your door.

And we haven’t even touched on the mental load. Those Sunday nights reconciling accounts. The background anxiety about whether you’re missing something. The constant switching between “business owner” mode and “amateur accountant” mode.

Your “free” system often costs three to five times as much as professional solutions. You can’t see it on your bank statement.

The Three-Part ROI Framework

ROI isn’t just what you spend. It’s what you gain, save, and avoid losing.

Part 1: Direct Cost Savings

This is time and labor you get back. Mark runs an environmental consulting firm. Before automation, he spent 12-15 hours weekly on financial tasks. After implementing automated transaction categorization and real-time dashboards, he reclaimed 10+ hours every week.

His firm grew 40% the following year while maintaining the exact administrative headcount.

“Working with System Six to automate our finances changed everything,” Mark shares. “Now I can pull up real-time insights from my phone between client meetings. We’ve grown significantly because I can focus on clients instead of paperwork.”

Part 2: Risk Mitigation Value

What do you save by avoiding penalties, errors, and missed opportunities? Automated systems catch things you’d forget. They track compliance deadlines systematically. They reconcile accounts daily rather than monthly, catching mistakes when they’re minor rather than catastrophic.

“System Six has done wonders for my stress level,” one client told us. “They’ve created automated systems that track every deadline and requirement. I no longer worry about compliance—it’s all handled automatically.”

No more late fees. No more scrambling at tax time. No more discovering errors three months after they happened.

Part 3: Growth Enablement Value

This is the big one. Better financial systems don’t just improve efficiency—they unlock revenue opportunities.

Elena runs a 12-person strategy consulting practice. Before automation, the month-end close took 5-7 days, and financial reports were perpetually outdated. After implementing full automation, the month-end dropped to less than a day.

But the real magic? Elena’s team gained clear visibility into project profitability, leading to a 22% increase in average project margin. Cash flow forecasting improved, allowing strategic hiring ahead of demand.

“The clarity we gained gave us the confidence to open a second office and hire three new consultants,” Elena reports. “We knew exactly which project types to pursue and had the cash flow visibility to make these moves confidently.”

One extra client meeting per week, enabled by automation, can translate into tens of thousands of dollars in additional annual revenue.

Your DIY ROI Worksheet

Let’s make this real. Grab a calculator.

Step 1: Calculate Your Current Hidden Costs

Track your time for one week. How many hours are you spending on financial tasks? Multiply that by four to get monthly hours. Then multiply by your effective hourly rate.

Example: 4 hours weekly × 4 weeks = 16 hours monthly × $200/hour = $3,200 in opportunity cost.

Now add up recent error costs from the last three months. Bank fees. Late penalties. That invoice you forgot to send. Divide by three for your monthly average.

Step 2: Project Your Savings

Automation typically reduces time spent on financial tasks by 70-80%. So if you’re spending 16 hours monthly now, you’d drop to about 3-4 hours, mostly reviewing automated reports.

You’d save 12 hours monthly. At $200/hour, that’s $2,400 in reclaimed time.

Most businesses see errors drop 80-90% with automation. If you’re averaging $500 in monthly error costs, reduce them to under $100.

Cash flow improvement? Automated invoicing typically reduces average payment time by 15-25 days. If you’re carrying $50,000 in receivables and your cost of capital is 6%, shaving 20 days off payment time saves roughly $165 monthly.

Step 3: Consider Costs

Setup typically ranges from a few hundred to a couple of thousand dollars. Monthly costs for automation tools and services usually range from $400 to $800 for small- to mid-sized businesses, covering bookkeeping, automation, reporting, and advisory support.

Step 4: Calculate Break-Even

Simple formula: Total One-Time Investment ÷ Monthly Net Savings = Months to Payback.

Real numbers: Say you invest $2,000 in setup and pay $800 monthly. Your monthly savings total $2,900 ($2,400 in time + $400 in error reduction + $165 in cash flow improvement minus $800 in fees = $2,165 net monthly benefit).

Your one-time costs pay back in less than one month. After that, you’re $2,165 ahead every single month.

Industry benchmark? Most firms hit break-even within 2-3 months.

Step 5: Factor in the Multiplier

What could you do with 12-15 extra hours monthly? Land one additional client quarterly? That could represent $50,000 to $100,000 in annual revenue growth.

As one business owner told us: “We’ve grown 40% this year because I can focus on clients instead of paperwork.”

Real Numbers from Real Businesses

Typical investment runs $400-$800 per week. Expected first-year ROI? Most businesses see returns of 300-500% through reclaimed time, improved efficiency, better decision-making, reduced compliance costs, and accelerated growth.

Payback period averages 2-3 months. Time reclaimed typically runs 15-20 hours per month.

Elena’s strategy firm went from struggling with a 5-7 day month-end close to opening a second office. The financial clarity didn’t just improve operations—it enabled growth that wouldn’t have been possible before.

The investment becomes self-sustaining within months, then generates profits for years.

The Decision Framework

Still on the fence?

What’s your current pain level? If you’re spending Sundays on bookkeeping and stressed about missed deadlines—that’s a signal. Your manual system is costing you more than money.

What’s your growth ambition? You can’t scale on manual systems. At some point, administrative burden becomes a constraint on growth.

What’s the cost of inaction? Every month you delay, you miss strategic opportunities. That $3,000 monthly in wasted time? That’s $36,000 in annual income you’re leaving on the table.

The question isn’t whether you can afford to automate. It’s whether you can afford not to.

Your Next Move

You didn’t become a business owner to spend weekends wrestling with reconciliations. You started your business to solve problems, serve clients, and build something meaningful.

Automation doesn’t just save time and money. It gives you back your weekends and lets you focus on what you do best.

What would you do with an extra 15-20 hours each month? Successful business owners already know the answer. They’d grow their business.

Start simple. Track your time for one week. Write down every hour you spend on financial tasks. Calculate what those hours cost. Add up recent error costs. Look at the total.

The numbers will speak for themselves.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, allowing owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance issues. Our team of over 35 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. From accurate bookkeeping to cash flow forecasting, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

Page 6 of 17« First«...45678...»Last »