by Chris Williams | Mar 2, 2026 | Blog

It was a Tuesday afternoon when Marcus realized something was wrong. Not catastrophically wrong — just the slow, expensive kind of wrong that’s easy to ignore. His office manager, Dana, had spent most of her morning re-entering last week’s expenses from a spreadsheet into QuickBooks. The same numbers, in a different place. Again.

“I could’ve sworn I already did this,” she told him. She had. Just somewhere else.

If that sounds familiar, you’re not alone. Manual data entry is one of those things that feels manageable in the moment but adds up to something significant over time. And for consulting firms — where every hour either generates revenue or doesn’t — the cost of manual bookkeeping errors and duplicated effort is real money walking out the door.

Here are seven manual data entry tasks quietly draining your team’s time, along with what automated data entry would look like as a replacement for each.

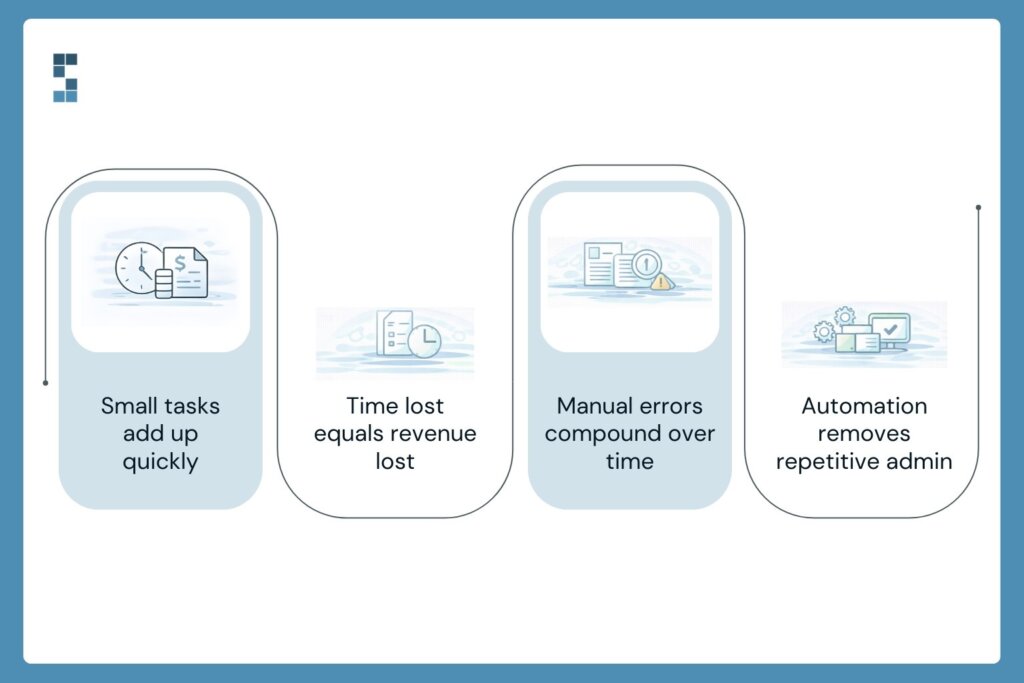

Why Manual Data Entry Is a Bigger Problem Than You Think

Most owners know they do some manual financial work. What they don’t know is how much. That “quick” Tuesday morning catch-up? It’s probably not 20 minutes. Track your team’s financial admin tasks for two weeks — every receipt entered, every invoice created, every bank statement cross-referenced — and most consulting firm owners discover they’re spending 15 to 20 hours a month on tasks that shouldn’t require a human at all.

At a typical consulting billing rate, that’s between $3,000 and $6,000 in lost productive capacity every single month. That’s before you factor in the cost of fixing manual bookkeeping errors, which have a frustrating way of multiplying through interconnected systems. One wrong categorization in October can still be causing headaches in March.

The fix isn’t a complete operational overhaul. It’s identifying the specific tasks where automation does a better job than a spreadsheet and a pair of tired eyes.

The 7 Tasks Worth Eliminating

1. Re-entering bank transactions

This is the granddaddy of all manual data entry tasks. Someone logs into the bank portal, downloads a statement, or scrolls through transactions, and types them into the accounting software one by one. It’s mind-numbing, time-consuming, and completely unnecessary. Bank feed integrations automatically pull transactions directly into QuickBooks or Xero. The human job shifts from data entry to review — a five-minute scan instead of an hour of typing.

2. Logging expenses from receipts

The old workflow: photograph the receipt, email it to yourself, open the accounting software, and manually enter the vendor, amount, date, and category. Modern OCR-based tools do all of this automatically from a photo. They extract the data, suggest a category, and flag anything that looks unusual. One System Six client cut their expense processing time from 4 hours a month to about 15 minutes of review.

3. Creating and sending invoices

For consulting firms, invoicing often means pulling hours from a time-tracking tool, building an invoice from scratch (or a template), double-checking the math, and sending it off. Every month. For every client. Template automation systems tied directly to your time-tracking software generate invoices automatically based on logged hours or project milestones. They send on schedule, track opens, and flag when payments haven’t been made.

4. Tracking invoice payment status

There’s a particular kind of Friday afternoon energy that goes into manually checking which clients have paid and which haven’t, then drafting polite but firm follow-up emails. Automated accounts receivable tools handle this entirely — monitoring payment status, sending reminders at intervals you set, and escalating when an invoice crosses a threshold. Your team stops chasing and starts reviewing.

5. Entering contractor hours for payroll and 1099s

If you use contractors (and most consulting firms do), someone is probably copying hours from a project management tool into a payroll system by hand—every pay cycle. Direct integrations between tools like Harvest or Toggl and payroll platforms eliminate this step. Hours sync automatically, reducing both the time burden and the risk of a payment error that makes for an uncomfortable conversation.

6. Updating cash flow spreadsheets

The classic consulting firm spreadsheet: a rolling cash flow projection that someone refreshes every week by pulling numbers from three different places and pasting them in. It’s valuable information locked inside a labor-intensive process. Live-connected financial dashboards pull the same data automatically and update in real time. You get the visibility without the Sunday night maintenance session.

7. Month-end reconciliation catch-up

When manual data entry has been the process all month, month-end reconciliation becomes an archaeological dig. You’re not just reconciling accounts — you’re hunting for the source of every discrepancy that accumulated during 30 days of human data entry. Automated transaction matching, combined with continuous reconciliation through the month, means there’s no backlog to excavate. Errors get caught the day they happen, not three weeks later.

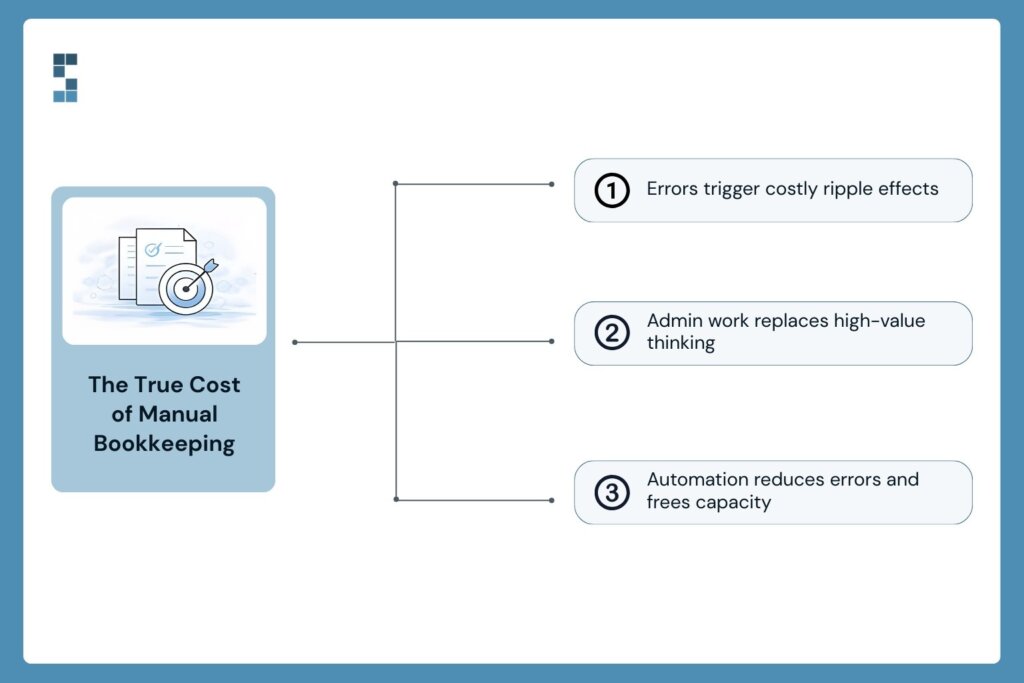

What This Actually Costs You

Let’s talk about the real price tag. It’s not just the hours spent doing these tasks — it’s the hours spent fixing what goes wrong because of them. Manual bookkeeping errors have a genuinely frustrating compounding quality. A miskeyed amount in a client invoice creates a billing discrepancy. That discrepancy requires an awkward conversation. That conversation takes time and erodes trust. All of it traces back to someone entering a number by hand when they didn’t need to.

There’s also the opportunity cost. When Dana spends her Tuesday morning on data re-entry, she’s not doing the work that actually requires her judgment — the analysis, the follow-up, the things Marcus hired her to do.

“I have told people that hiring them was the best decision I made at the start of the business. They have crushed it. We just finished our 2022 audit, and the auditors found exactly 0 errors by S6. Not only have they been mistake-free, but S6 has also been proactive at catching mistakes I’ve made and asking me the right questions to keep the books updated. — Paul”

Zero errors in an audit. That’s what happens when automated systems replace manual entry and a professional team reviews rather than re-enters.

What would your team do with 10 extra hours a month?

The Shift From Re-entering to Reviewing

Marcus made some changes. Dana still works with the financials every week — but now she’s reviewing what the system already captured, not rebuilding it from scratch. She catches the occasional miscategorized transaction. She flags an invoice that went out to the wrong contact. She actually has time to pull a project profitability report and bring it to Marcus before the client debrief.

That’s the shift automation makes possible. It doesn’t replace judgment. It removes the grunt work so judgment can actually happen.

Automated data entry isn’t about fancy software or a technology overhaul. It’s about connecting the systems you probably already use — your bank, your time tracker, your project management tool — so data flows automatically instead of being carried by hand from one place to another.

System Six helps consulting firms set up workflows exactly like these. Fixed weekly pricing, no long-term contracts, and a team that already knows consulting firm finances inside and out. If you’re curious how many hours your firm is losing to manual entry, let’s find out together.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Feb 23, 2026 | Blog

It’s Sunday night. Again.

The laptop casts a pale glow across your kitchen table. Your QuickBooks tab is open next to a cold cup of coffee and a stack of receipts you’ve been meaning to deal with since Wednesday. Meanwhile, your family is somewhere in the next room without you. You’re categorizing expenses. Manually. One. By. One.

If that scene is a little too familiar, here’s a question worth sitting with: what if you could automate that entire pile of work — the invoicing, the expense capture, the follow-up emails, the payment alerts — without writing a single line of code?

That’s not a hypothetical. It’s what Zapier does. And consulting firm owners are quietly using it right now to reclaim hours every week that used to disappear into financial admin.

This post breaks down five Zapier accounting workflows worth setting up this week — and why getting them right is the difference between working smarter and just adding complexity to your plate.

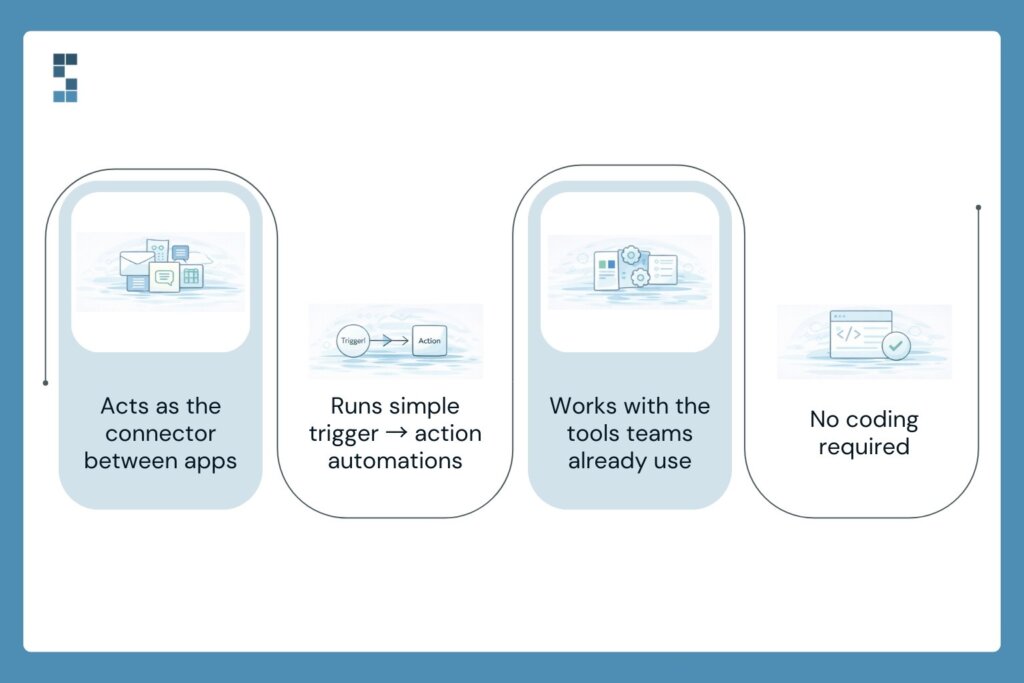

What Zapier Actually Does (And Why You Don’t Need IT to Use It)

Think of Zapier as a relay runner between your apps. One app finishes its leg — say, a new client signs a proposal in your CRM — and Zapier immediately hands the baton to the next one, triggering an invoice in QuickBooks before you’ve even looked up from your desk.

Each automation is called a “Zap,” and every Zap works the same way: a trigger happens in one app, which kicks off an action in another. No code. No developer. No IT ticket filed and forgotten.

The apps Zapier connects include pretty much everything a consulting firm already runs on — QuickBooks, Xero, Stripe, HubSpot, Gmail, Slack, Google Sheets, Asana, ClickUp. If your team uses it, there’s a good chance Zapier can connect it.

The setup is point-and-click. You pick a trigger. You pick an action. You test it. You turn it on. That’s it. Most Zaps take less than 15 minutes to build the first time, and once they’re running, they run quietly in the background — no check-ins required.

5 Zapier Accounting Workflows Worth Setting Up This Week

Let’s get specific. Here are the five workflows that deliver the most immediate time savings for consulting firms — what each one does, why it matters, and how it works at a high level.

1. Auto-Create Invoices When a Project Is Signed

Trigger: New deal marked “Closed Won” in HubSpot (or your CRM of choice). Action: Invoice automatically generated in QuickBooks with the client name, project details, and amount pre-filled.

Why it matters: Most consulting firms create invoices manually after every engagement kicks off. That’s a 10–15 minute task that happens dozens of times a year. This Zap makes it instant. The invoice exists before you’ve finished the kick-off call.

2. Capture and Log Expense Receipts Automatically

Trigger: Receipt arrives in Gmail (forwarded from a team member or vendor). Action: Expense automatically created and categorized in QuickBooks.

Why it matters: Lost receipts and delayed expense entry are two of the most common bookkeeping headaches for growing firms. This Zap catches them the moment they hit your inbox — no spreadsheet, no shoebox, no Monday morning archaeology required.

3. Get Instant Payment Alerts When Clients Pay

Trigger: Payment received in Stripe or PayPal. Action: Slack notification sent to you (and/or your bookkeeper) with the client name and amount.

Why it matters: Cash flow visibility matters, especially when you’re managing multiple client engagements simultaneously. Instead of logging into your payment processor to check on a deposit, you just look at Slack. Done.

4. Send Automated Follow-Ups on Overdue Invoices

Trigger: Invoice status in QuickBooks passes X days without payment. Action: Personalized follow-up email sent automatically from your Gmail.

Why it matters: Chasing late payments is awkward, time-consuming, and easy to let slide. This Zap does it for you — politely, consistently, and on schedule. Your cash flow improves. Your discomfort goes down. Everybody wins.

5. Trigger Your Monthly Close Checklist Automatically

Trigger: A recurring calendar event fires on the first of every month. Action: A monthly close checklist task is automatically created in Asana, ClickUp, or your project management tool of choice.

Why it matters: Month-end close tasks get missed because they live in someone’s memory or a sticky note. This Zap turns your close process into a reliable, repeatable system that kicks off without anyone having to remember.

The Real Math: What This Time Is Actually Worth

Here’s the number most consulting firm owners don’t want to look at directly: the typical owner spends 15–20 hours a month on financial administration. At a conservative billing rate of $250 an hour, that’s $3,750 to $5,000 worth of capacity consumed by manual tasks every single month.

Every month. That’s not a rounding error. That’s a client.

The consulting firm owners who’ve made the shift to automation see this clearly in hindsight. Mark, a management consultant who worked with System Six to overhaul his firm’s financial processes, put it simply: “We’ve grown 40% this year because I can focus on clients instead of paperwork.” Three new client relationships. Because the time was finally there to build them.

That’s not a coincidence. That’s what recaptured time does when it gets pointed at the right work.

No-code automation finance tools like Zapier don’t just save minutes — they free up the kind of focused attention that actually moves a business forward. The kind you can’t access when you’re knee-deep in expense categorization on a Sunday night.

The Catch — And How to Avoid It

Here’s the part nobody’s going to put in a Zapier tutorial.

Automation amplifies whatever’s already there. If your underlying data is messy — duplicate vendors, inconsistent expense categories, a chart of accounts that grew organically and now looks like a bowl of spaghetti — Zapier will move that mess faster and into more places. You’ll have automated chaos instead of manual chaos. Different problem, same headache.

The other common mistake is setting up Zaps without error notifications. A Zap fails silently. Data doesn’t transfer. Nobody knows. Three weeks later, your books are off and you’re not sure when it started.

This is where financial expertise matters just as much as the tech. The Zapier accounting workflows themselves are simple. Getting the foundation right — clean data, well-structured accounts, proper triggers — that’s where the real work is. And it’s work worth doing with someone who knows what they’re looking at.

Manish G., a Seattle-based business owner, described his experience with System Six this way: “They take on the entire setup, and effectively act as consultants until your accounting operations are running like a well-oiled machine. Then, they handle all ongoing issues.” That’s the goal — not just automating your current process, but making sure what you’re automating is worth running at speed.

What Would You Do With 10 Extra Hours?

Go back to that Sunday night for a second. Same kitchen table, same cold coffee, same receipts.

Now imagine it differently. The invoices are already generated. The expenses are already logged. The overdue payment reminder went out Thursday without you touching it. And your monthly close checklist appeared in Asana this morning, on its own, right on schedule.

You’re in the other room. With your family. Not because you finished early. Because there was nothing left to finish.

That’s what good Zapier accounting workflows actually look like in practice — not a flashy tech demo, but a quieter Sunday night and a Monday morning spent on the work that actually requires you.

The tools to build this exist today. Most are free to try. The question isn’t whether you should automate — it’s whether you can afford to keep doing it the manual way.

If you’re ready to get your financial workflows built right from the start, System Six helps consulting firms design and implement automation strategies that actually stick — clean data, correct integrations, and ongoing support from a team that knows consulting firm finances inside and out. With 35+ team members, 175+ clients, and a 9.5/10 NPS score, we’ve done this before.

Reach out to start the conversation. Your Sunday nights are worth it.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Feb 16, 2026 | Blog

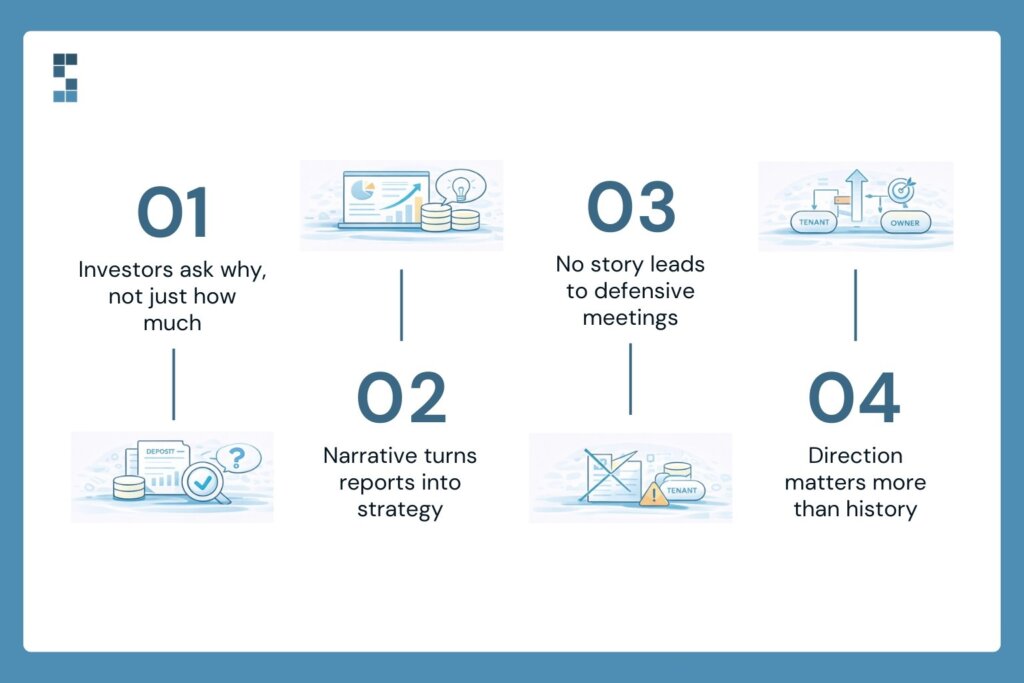

Picture this. You’re sitting across from a prospective investor. Your consulting firm has a strong team, happy clients, and a growing pipeline. Everything feels right. Then they ask to see your financials.

You slide a basic profit-and-loss statement across the table. It’s accurate. The numbers add up. But within seconds, you can feel the energy drain from the room. Their eyes glaze over. The conversation shifts from “when can we start?” to “we’ll be in touch.”

The problem wasn’t your numbers. It was the absence of a story around them.

Financial storytelling—the art of turning raw data into a narrative that investors actually care about—is one of the most overlooked tools in a consulting firm owner’s toolkit. And it’s not about spin or exaggeration. It’s about context, clarity, and confidence. Firms that master this skill don’t just attract capital. They build the kind of professional reputation that opens doors for years to come.

Your Numbers Already Have a Story. You’re Just Not Telling It.

Here’s the thing most consulting firm owners get wrong about financial reports: they treat them like a homework assignment. Something to check off the list. Accurate? Yes. Useful to an investor? Not even close.

Raw numbers without narrative are like a novel with no plot. You’ve got characters and settings, but no one knows what’s happening or why they should care. An investor doesn’t just want to know that your revenue grew 18% last year. They want to know why it grew, whether that growth is repeatable, and what you’re doing to sustain it.

That’s what financial storytelling is. It’s the difference between a spreadsheet that lists figures and a report that paints a trajectory—one that shows where you’ve been, where you are, and where you’re confidently heading next.

And here’s what happens when the story is missing. Poor financial reporting undermines investor confidence. Board meetings become defensive exercises instead of strategic planning sessions. You spend the whole conversation explaining your numbers rather than discussing your vision.

When was the last time you looked at your own reports through an investor’s eyes? If the answer makes you uncomfortable, you’re not alone. Most consulting firms produce basic P&Ls that don’t support the kind of conversations investors want to have.

What Actually Goes Into an Investor-Ready Report

So what separates a report that gets filed away from one that gets an investor to lean forward in their chair? It comes down to a handful of elements that most firms overlook.

First, variance analysis. This is the “what changed and why” layer. Did your margins dip last quarter? A basic report shows the dip. An investor-ready report explains it—maybe you invested in a new hire who’s already billing at full capacity, or you expanded into a new market that hasn’t matured yet. Context transforms a red flag into a strategic decision.

Second, KPI tracking is tied to actual goals. Investors want to see that you’re measuring the things that matter—not just revenue and expenses, but utilization rates, client retention, project profitability, and pipeline health. These are the vital signs of a consulting business, and they tell a much richer story than a top-line number ever could.

Third, cash flow forecasting. Nothing signals forward thinking like a 12- or 18-month cash flow projection. It tells investors you’re not just reacting to what’s in front of you—you’re planning for what’s around the corner.

And finally, strategic commentary. This is where the real storytelling lives. Brief narratives alongside the numbers that connect the dots: here’s what we did, here’s what happened, and here’s what we’re doing next. It’s the difference between handing someone a map and actually walking them through the territory.

One client put it this way after transforming their reporting: “We just finished our audit, and the auditors found exactly zero errors. Not only have they been mistake-free, but they’ve also been proactive at catching mistakes I’ve made and seeing challenges coming down the pike.” That kind of precision isn’t just nice to have. It’s the foundation on which financial storytelling is built. You can’t tell a compelling story if the underlying data is shaky.

And here’s something worth noting: investor-ready reports aren’t just for firms chasing outside capital. They sharpen your own decision-making. They reinforce your professional reputation with clients, partners, and lenders. They reduce the financial anxiety that keeps firm owners up at night, wondering whether they’re making the right calls.

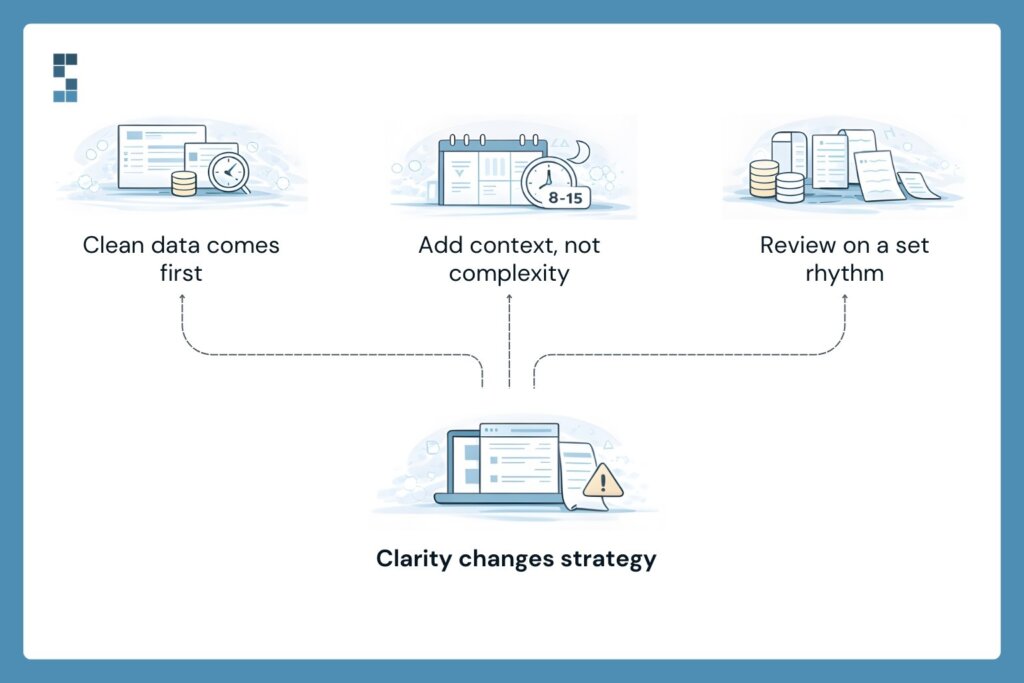

How to Start Telling Your Financial Story Today

The good news? You don’t need to become a CFO overnight. But you do need to start somewhere. And the place to start is simpler than you might think.

Get the foundation right first. Financial storytelling falls apart without clean, consistent data. That means addressing the boring-but-essential stuff: consistent time tracking, timely expense reporting, and accurate project coding. If your team is logging hours inconsistently or submitting expenses three weeks late, no amount of narrative polish will save your reports.

Once the data is solid, start layering in context. Add variance analysis to your monthly reports. Include trend lines that show three-, six-, and twelve-month trajectories. Write two or three sentences of strategic commentary for each major section. You’d be surprised how much a few lines of “here’s what this means” can transform a dense spreadsheet into a document that actually communicates something.

Then establish a rhythm. Different reports require different cadences: daily cash position checks, weekly utilization reviews, monthly profitability deep dives, and quarterly strategic assessments. This structure isn’t just for investors—it’s for you. It creates the kind of financial clarity that enables confident decisions.

One environmental consulting firm discovered this firsthand. After rebuilding their reporting systems, they finally gained visibility into which parts of their business were actually making money. The result? A 40% improvement in reporting accuracy, a 22% margin improvement, and the confidence to expand into their most profitable service areas. As they put it: “We had no idea which parts of our business were actually making money until we rebuilt our reporting.”

That’s the power of financial storytelling in action. It doesn’t just impress investors. It transforms how you run your firm.

The Story Your Numbers Tell

Let’s go back to that conference room. Same investor, same firm. But this time, you slide across a report that tells a story. Revenue trajectory with clear drivers. KPIs that show a healthy, disciplined operation. Cash flow projections that demonstrate forward thinking. Strategic commentary that connects every number to a decision and a direction.

The investor doesn’t just see data. They see a firm worth backing.

Financial storytelling isn’t about dressing up your books or putting lipstick on a pig. It’s about presenting the truth of your business in a way that builds confidence, earns trust, and reinforces the professional reputation you’ve spent years building. It’s about making sure your numbers work as hard for you as you work for them.

So here’s the question worth sitting with: What story are your financials telling right now? And is it the story your firm deserves?

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Feb 9, 2026 | Blog

Picture this. It’s Sunday evening, and you’re sitting at your kitchen table surrounded by a small mountain of receipts, printed invoices, and bank statements. You’ve got a shoebox of expense slips from last quarter that still need sorting. There’s a filing cabinet in your office that hasn’t closed properly in months. And somewhere in that pile is a vendor receipt you need for client reimbursement—but good luck finding it.

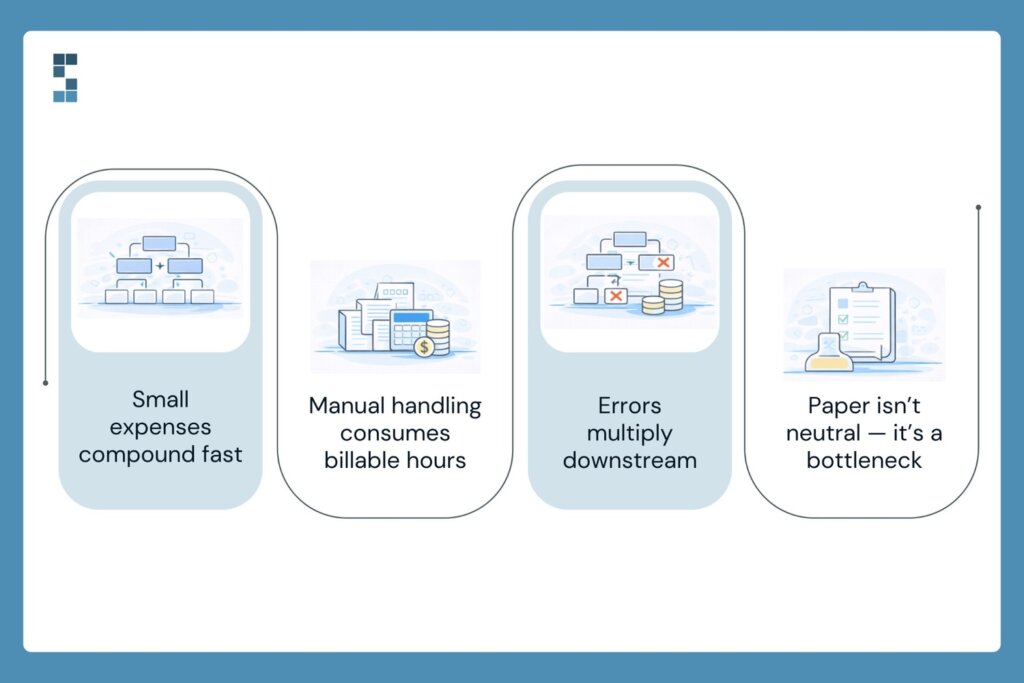

Sound familiar? If you’re running a consulting firm, your financial paperwork looks something like this. And here’s the thing most people miss: all that paper isn’t just cluttering your office. It’s quietly draining your budget, eating your time, and introducing errors you won’t catch until tax season.

Going paperless isn’t some trendy sustainability gesture. It’s a financial strategy. And for consulting firms trying to stay lean and profitable, it might be one of the smartest moves you make this year. Let’s walk through why — and how to actually do it without losing your mind.

The Hidden Price Tag of Paper-Based Processes

The obvious costs of paper are easy to dismiss. Printer ink, copy paper, postage, and filing supplies — none of those line items look alarming on their own. But they add up faster than you’d expect, especially when you factor in the storage space those filing cabinets occupy in your office. Real estate isn’t cheap, and dedicating square footage to old bank statements is a lousy use of it.

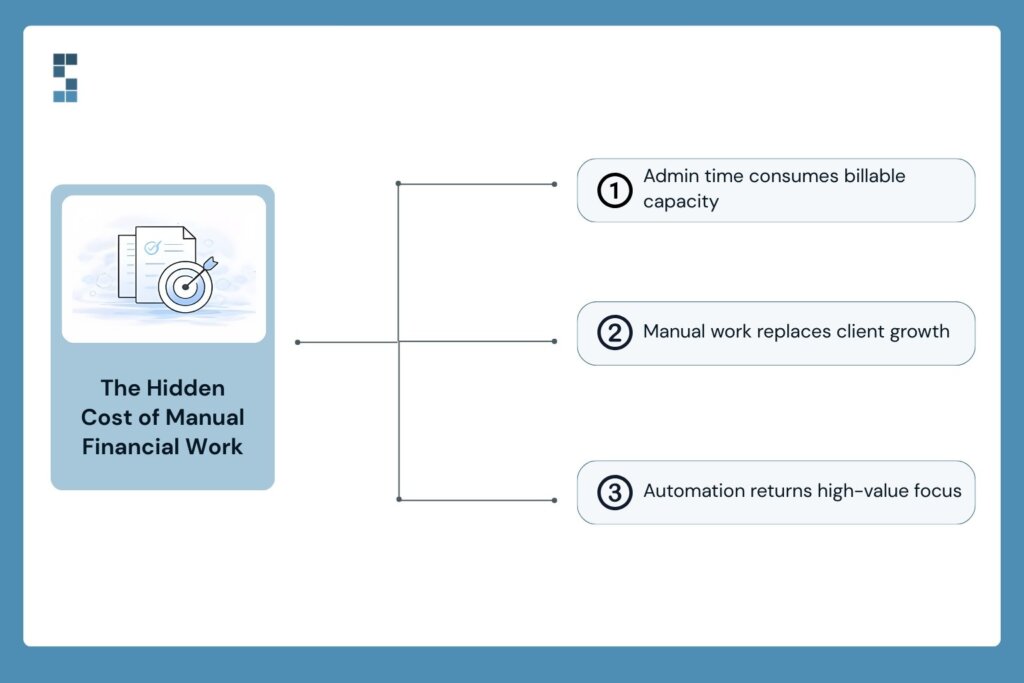

But the real expense? It’s your time.

Think about what happens every time a paper receipt enters your workflow. Someone has to collect it. Someone has to enter the data manually. Someone has to file it in the right folder, match it to the right project, and hope they didn’t transpose a digit somewhere along the way. Multiply that process across dozens of transactions every week, and you’re looking at hours of work that produce zero revenue.

Most consulting firm owners spend somewhere between 10 and 15 hours every week on manual financial tasks. At typical consulting rates, that’s $2,000 to $3,750 in billable time — gone. Every single week. Not because the work is complex, but because the process is inefficient.

And then there’s the error problem. Manual data entry introduces mistakes at predictable rates, and those mistakes don’t stay contained. One wrong number on an expense report cascades into your project profitability calculations, your tax filings, and sometimes your client invoices. Fixing those errors often takes longer than the original task.

Paper isn’t just clutter. It’s a bottleneck that’s costing you more than you realize.

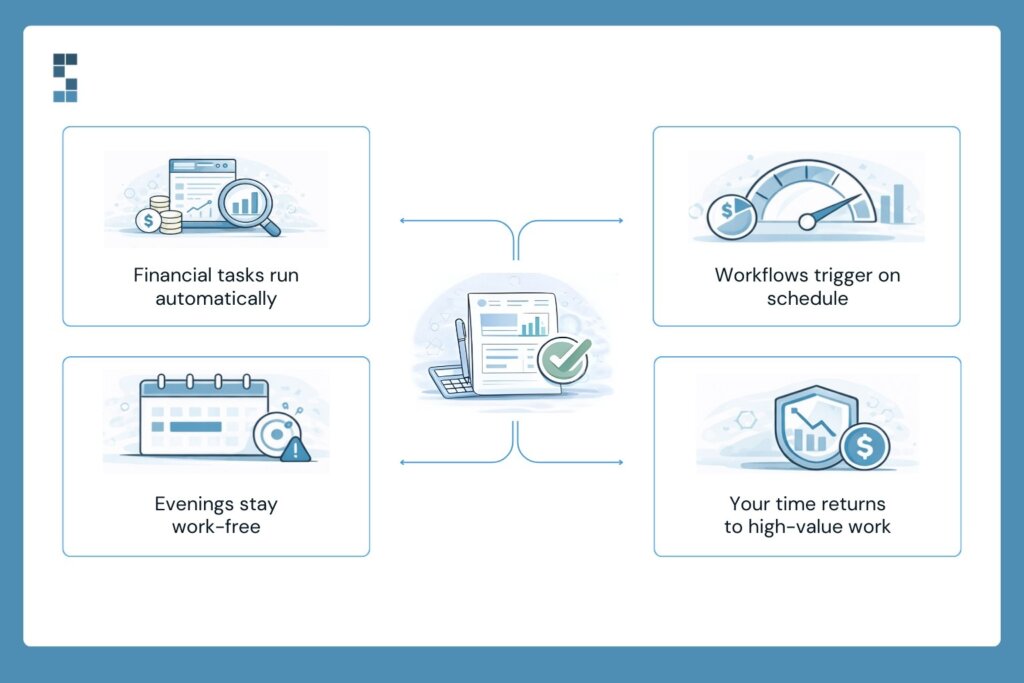

What Paperless Accounting Actually Looks Like

Here’s where people get tripped up. “Going paperless” sounds like flipping a switch — one day you have paper, the next day you don’t. But that’s not how it works, and honestly, that all-or-nothing thinking is what keeps most firms stuck.

Think of it more like installing plumbing. Right now, you’re essentially carrying water from a well every time you need it — manually hauling data from one place to another, printing things so you can look at them, filing documents so you can find them later. Paperless workflows create direct connections between your systems so information flows automatically, without you having to touch it.

In practice, that means a few key changes—first, digital receipt capture. Instead of stuffing paper receipts into envelopes, you snap a photo with your phone, and the system extracts the vendor, amount, and category automatically — with over 90% accuracy. Second, cloud-based document storage replaces your filing cabinets entirely. Every invoice, contract, and statement lives in a searchable digital system. No more digging through folders for twenty minutes to find one document.

Then there’s automated transaction categorization, which handles the tedious work of sorting expenses into the right accounts. Electronic invoicing with built-in payment reminders replaces the old routine of creating invoices in Word, emailing them manually, and then chasing payments with awkward follow-up calls. Digital approval workflows mean expense reports get routed, reviewed, and approved without a single piece of paper changing hands.

One System Six client described the shift perfectly — they went from spending Sunday afternoons wrestling with bookkeeping to reviewing automated reports for about 15 minutes on Monday mornings. That’s not a minor improvement. That’s a fundamentally different way of running your back office.

The ROI of Going Green With Your Books

So what does all this actually save you? Let’s talk numbers, because this is where paperless accounting stops being a nice idea and starts being a no-brainer.

Start with time. Consulting firms that implement automated, paperless financial workflows typically see a 70 to 80 percent reduction in the hours they spend on financial management — and many hit that milestone within 90 days of making the switch. If you’re currently burning 15 hours a week on manual processes, you could realistically get that down to three or four.

Accuracy improves dramatically, too. Automated categorization doesn’t get tired at 9 PM and accidentally code a software subscription as office supplies. It doesn’t transpose numbers. It doesn’t lose receipts. One firm that made the switch to System Six cut its expense processing time by 80% and virtually eliminated lost receipts overnight.

Cash flow speeds up in ways you can feel. When you move from manual invoicing to automated billing with built-in payment reminders, clients pay faster. One consulting firm saw its average collection time drop from 45 days to 22 days. That’s not a marginal improvement — that’s the difference between comfortable cash flow and constantly checking your bank balance.

And the compliance headaches? Gone. Automated deadline tracking handles tax filings, contract renewals, and regulatory requirements without relying on your memory or a spreadsheet you might forget to check. As one business owner put it after working with System Six, they no longer worry about compliance because it’s all handled automatically.

Here’s where the math gets exciting. Say you bill $200 an hour and you’re spending 10 hours a month on manual, paper-heavy financial tasks. That’s $24,000 a year in opportunity cost — revenue you could’ve earned but didn’t. One firm that reclaimed those hours redirected the time toward client work and business development. They grew 40% the following year without adding a single administrative hire.

For most consulting firms, the break-even point for going paperless lies between 2 and 3 months. First-year ROI often exceeds 300%. It’s hard to find many business investments with that kind of return.

Getting Started Without the Overwhelm

I get it — the idea of overhauling your financial processes sounds exhausting when you’re already stretched thin. But here’s the good news: you don’t have to do everything at once.

Pick one area. Expense tracking and receipt management are usually the easiest wins, because the pain is obvious and the improvement is immediate. Master that system, measure your time savings, and then expand from there. Before you start, spend two weeks tracking how much time you actually spend on paper-based financial tasks. That baseline will show you exactly where the biggest opportunities are — and it’ll motivate you when you see the before-and-after.

If you want to accelerate the process, professional implementation makes a real difference. System Six specializes in helping consulting firms build paperless financial workflows, and most firms are fully operational within four weeks. Their automation strategies typically pay for themselves within 60 to 90 days, driven solely by time savings.

Your Paper Trail Doesn’t Have to Be Literal

Going paperless isn’t really about saving trees — though that’s a nice bonus. It’s about reclaiming your time, eliminating the errors that come with manual processes, and building financial systems that actually scale as your firm grows. It’s about spending your Monday mornings on strategy rather than data entry, and your Sunday evenings on whatever you want rather than sorting receipts.

What would you do with an extra 15 hours every month?

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Feb 2, 2026 | Blog

Picture this. It’s Monday morning. You sit down with your coffee, open your laptop, and pull up QuickBooks. But something’s wrong. The screen doesn’t look right. Your data’s gone—or worse, locked behind a ransomware message demanding payment in cryptocurrency. Years of billing records, project profitability data, client payment histories, and payroll files. All of it, inaccessible.

Your stomach drops. You think about the tax filing due next month. The client invoices are waiting to go out. The payroll runs on Friday.

Now ask yourself: how fast could you recover?

If you run a consulting firm and your financial records live in the cloud, you might assume they’re safe. And to a point, they are. Cloud platforms like QuickBooks Online, Gusto, and Ramp are far more reliable than the filing cabinet in your back office. But “in the cloud” doesn’t automatically mean “protected from disaster.” There’s a gap between cloud storage and true disaster recovery—and that’s where consulting firms get hurt.

Let’s close it.

“Cloud” Doesn’t Mean “Covered”

Here’s the thing most consulting firm owners don’t realize: cloud platforms protect against their failures—server outages, hardware problems, platform-level issues. They don’t necessarily protect against yours.

What does that mean in practice? It means your data is still vulnerable to plenty of real-world threats. A team member accidentally deletes a critical account category, and no one notices for 3 weeks. A ransomware attack encrypts your local machine and spreads to connected cloud syncs. An integration between your expense management tool and your accounting platform glitches, corrupting transaction data across both systems. Or a former employee with lingering access makes unauthorized changes.

These aren’t hypotheticals. Nearly half of all small businesses have experienced some form of data loss, and a significant percentage of those that suffer a major data event never fully recover. For a consulting firm with complex project billing, multi-state payroll, and client-sensitive financial information, the stakes are even higher.

So what actually protects your financial records when things go wrong?

Three Pillars of a Cloud Disaster-Recovery Plan

You don’t need a degree in IT to build a solid disaster-recovery plan for your financial data. You need three things working together: reliable backups, strong access controls, and a tested recovery process. Think of them like the legs of a stool. Remove one, and the whole thing tips over.

Pillar 1: Automated Backups That Actually Run

This sounds obvious, and yet it’s where most firms stumble. They assume their cloud platform handles backups automatically. And it does—to a point. But platform-level backups are designed to protect the platform, not necessarily your specific data configuration, custom reports, or integration settings.

What you need is a separate, automated backup system that captures your complete financial picture at regular intervals. For consulting firms running active billing cycles with retainer payments, milestone invoices, and expense reimbursements flowing through every week, daily backups aren’t overkill. They’re the minimum.

And those backups need to live somewhere independent of your primary cloud environment. If everything sits on the same platform and that platform has a bad day, your backup goes down with it. Redundancy isn’t a luxury. It’s the whole point.

Pillar 2: Access Controls and Security Layers

The best backup in the world won’t help if someone walks in the front door and messes up your records before you notice. Access controls are your first line of defense—and most consulting firms don’t treat them that way.

Think about how many people can currently access your financial systems. Your office manager, your accountant, a partner or two, a contractor helping with special projects. How many of those people have full admin access? How many use the same password for their email and their accounting login?

A strong disaster-prevention strategy includes bank-level security with encrypted data transmission, restricted access protocols that limit who can see what, and comprehensive confidentiality agreements with anyone who touches your financial data. It also means two-factor authentication on every account, regular access audits, and immediate offboarding when someone leaves the firm.

This is especially critical for consulting firms serving regulated industries. Your clients trust you with sensitive information. If your financial systems get compromised, it’s not just your problem—it becomes theirs, too.

Pillar 3: A Tested Recovery Process

Here’s where things get real. Having backups is one thing. Knowing you can actually use them is another.

Imagine a firm that diligently backs up its QuickBooks data every night. Feels great. Then one day, a corrupted file wipes out two months of transaction data. They go to restore the backup and realize—nobody on the team actually knows how. The backup files are in a format no one recognizes. The person who set up the system left the company last year. And now everyone’s scrambling while the clock ticks toward a payroll deadline.

A disaster-recovery plan without regular testing is just a document gathering digital dust. Run fire drills. At least once a quarter, walk through the actual recovery process. Verify that backups are complete, that someone on your team knows how to restore them, and that the restored data matches what you’d expect. The time to discover a problem with your recovery plan is during a drill—not during a crisis.

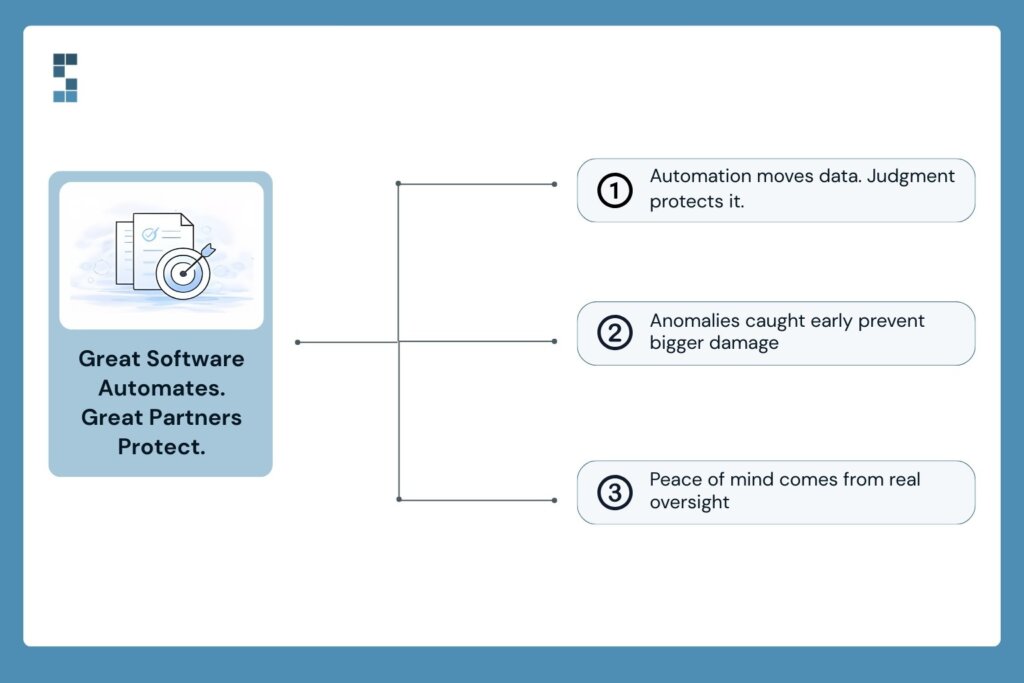

Why Your Financial Partner Matters More Than Your Software

Software handles automation. People handle judgment. And when something goes wrong with your financial records, you need both—but you really need people who know your specific setup inside and out.

A dedicated financial team doesn’t just process your transactions and move on. They monitor data integrity. They catch anomalies before they become disasters. They notice when something looks off in your reconciliation and dig in before a small discrepancy becomes a large one.

One business owner put it this way: “Hiring them was the best decision I made at the start of the business. We just finished our audit, and the auditors found exactly zero errors. Not only have they been mistake-free, but they’ve also been proactive at catching mistakes I’ve made and seeing challenges coming down the pike.” That kind of vigilance—the kind that looks around corners—is what separates a service provider from a genuine partner.

At System Six, this is built into how we work. Our cloud-based infrastructure employs bank-level security, including encrypted data transmission and restricted access protocols. Our team of 35+ U.S.-based professionals, each averaging over 10 years of accounting experience, operates as an extension of your business—not a faceless vendor you email and hope for the best. When our clients say they feel like we’re “part of the team,” that’s not marketing language. It’s what a 9.5 out of 10 NPS score looks like in practice.

As another client shared, “System Six has done wonders for my stress level to feel like this is all now taken care of with a professional partner.” That peace of mind? It comes from knowing someone’s watching the details you can’t afford to miss—including the integrity of your financial data and the systems protecting it.

The Bottom Line: Hope Is Not a Recovery Strategy

Disaster recovery isn’t an IT problem. It’s a financial survival strategy. For consulting firms juggling project billing across multiple clients, managing multi-state payroll for remote consultants, and handling sensitive financial data that clients trust you to protect, the stakes are too high for a “hope for the best” approach.

The good news? You don’t have to figure this out alone. The right financial partner will already have these protections in place—automated backups, bank-level security, tested recovery protocols, and a team that treats your data with the same care they’d give their own.

So here’s the question worth sitting with: if your financial records disappeared tomorrow, how fast could you get back to business?

If the answer makes you uncomfortable, it might be time to talk.

Schedule a complimentary consultation with System Six to assess your current financial infrastructure and identify gaps in your data protection and disaster recovery strategy, because the best time to plan for a crisis is before you’re in one.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Jan 28, 2026 | Blog

Picture this: You’ve just landed the contract you’ve been chasing for months. A major client, prestigious work, and it’s going to double your firm’s workload overnight. You should be celebrating. Instead, you’re sitting at your desk at 10 PM, staring at a tangle of spreadsheets and sticky notes, wondering how your financial systems will handle the surge.

Sound familiar? You’re not alone. I’ve talked with dozens of consulting firm owners who’ve faced this exact moment—the terrifying realization that the growth they worked so hard to achieve might break the very systems that keep their businesses running.

Here’s what separates firms that scale smoothly from those that collapse under their own success: It’s not more software. It’s not hiring faster. It’s having documented, repeatable financial processes (SOPs) in place before growth hits. Most firms try to scale first and systematize later. That’s backwards, and it’s expensive.

Why Chaos Scales Faster Than Growth

Most consulting firms outgrow their financial systems but never upgrade. They’re running a $5 million company with the same spreadsheets they used at $500K. The invoicing process that worked when you had three clients? It buckles under thirty. The expense tracking that lived in your head? It creates chaos when five people need access to it.

I spoke with Mark, whose environmental consulting firm hit this wall hard. “We thought we were making money on every project until we dug into the numbers,” he told me. “We had no reliable way to track time against projects, so we couldn’t see which engagements were profitable. Turns out our large regulatory projects were actually break-even when you factored in all the partner time.”

The common mistake? Trying to automate chaos rather than documenting transparent processes first. You can’t systematize what you haven’t defined. And when growth hits, undefined processes don’t just stay messy—they multiply the mess.

Here’s the real cost: Most consulting firm owners spend 15-20 hours monthly on financial administration. At typical consulting rates of $200-300 per hour, that’s $3,000-6,000 in lost billable time every month—or up to $72,000 annually. That’s not just time lost. That’s a new hire—a significant marketing push. Revenue sacrificed to wrestling with spreadsheets.

The Four Non-Negotiable Finance SOPs for Scalability

Think of SOPs like the foundation of a house. Nobody sees them once the building’s up, but try adding a second story without one. These four financial SOPs form the foundation that lets you scale without cracking.

Project Profitability Tracking. Time is your inventory. You’re not selling widgets—you’re selling hours and expertise. Your SOP must connect time tracking directly to profitability reporting. Document who logs time, how frequently, what categories to use, and how it maps to client billing. Without this, you’re flying blind. One System Six client put it simply: “They revamped our whole accounting system into accurate and dependable practices. Now I can pull up real-time insights about project profitability from my phone between client meetings.”

Expense Management and Categorization. The old way involves collecting receipts in a shoebox, entering them manually on weekends, and hoping you don’t miss anything important. The documented way creates clear rules: who approves what, how expenses get categorized, and when receipts must be captured. One consulting firm owner reported cutting their expense processing time by 80% after implementing a documented workflow. No more lost receipts. No more delayed reimbursements. No more Sunday afternoon data entry.

Invoice and Collections Workflow. Document the entire lifecycle: what triggers invoice generation, who approves before sending, when invoices go out, and the exact cadence for follow-ups on overdue accounts. This SOP paid off dramatically for one firm whose average payment time dropped from 45 to 22 days after implementation. That’s not just faster money—it’s predictable cash flow that lets you plan with confidence.

Compliance Calendar and Tax Documentation. Map every deadline across state and federal requirements. Create systematic documentation collection so you’re not scrambling at tax time. As one client shared, “System Six has done wonders for my stress level. They’ve created automated systems that track every deadline and requirement. I no longer worry about compliance—it’s all handled automatically.” That peace of mind doesn’t happen by accident. It happens because someone documented the process.

From Your Head to the Page—and Into Practice

Having SOPs isn’t about creating bureaucracy. It’s about making yourself unnecessary for day-to-day financial tasks so you can focus on client work and business development when growth hits. But documentation that lives in a forgotten folder helps no one. Here’s how to create SOPs that actually survive contact with reality.

Start with your pain points. Where are you spending the most time each month? What causes the most stress? Those pressure points tell you exactly where documentation will yield the most significant dividends. Map the actual workflow before you try to improve it—you can’t fix what you haven’t captured honestly.

Write it so someone else can follow it without asking you questions. Build in triggers and decision points: “If X happens, do Y.” The test isn’t whether you can follow it. The test is whether a new hire could follow it on day one.

The common pitfalls? Creating SOPs only you understand. Over-documenting to the point of paralysis. And the worst one: documenting but never training or enforcing. As one reviewer described working with System Six: “They take on the entire setup and effectively act as consultants until your accounting operations run smoothly.” That’s the goal—building systems that work without you hovering over them.

Consider Lisa, whose environmental consulting firm grew from eight to twenty-five employees in eighteen months. “Our financial system scaled seamlessly with us,” she explains, “so I never worry about operational capacity limiting our growth anymore.” That seamless scaling didn’t happen by accident. It happened because the processes were documented before the growth arrived.

From Sunday Night Spreadsheets to Monday Morning Strategy

What does life look like on the other side of documented financial SOPs? Monthly close takes hours, not days. Cash flow forecasting updates in real-time as invoices get paid and expenses get recorded. Project profitability data is always up to date because your time-tracking, billing, and reporting systems are connected.

One client described the transformation this way: “I don’t have to think about my accounting anymore. It’s just taken care of seamlessly. Great service, great value.” Another reported, “Since automating our finances, I’ve landed three new major clients. Those deals happened because I could focus on relationships instead of reconciliations.”

The psychological shift is massive. When you’re not constantly putting out financial fires, you can think strategically about growth rather than just surviving it. You can say yes to bigger opportunities because you’re not worried about whether your back-office can handle the load. The bandwidth you recover isn’t just time—it’s mental energy for the work that actually requires your expertise.

Building Before You Need It

Let’s go back to that scenario—you’ve just doubled your workload with a significant contract win. The difference between thriving and drowning isn’t luck, talent, or even hustle. It’s preparation. It’s having built the financial infrastructure that amplifies your competitive advantages rather than creating limitations you have to work around.

The best time to build these SOPs was before you needed them. The second-best time is now, before the next growth surge catches you unprepared.

Start with an honest audit of your current pain points. Which financial tasks consume the most time each month? Where do bottlenecks emerge when you’re busy? What keeps you up at night during tax season? Those pressure points tell you exactly where documentation and systematization will yield the most significant dividends.

The consulting firms thriving in 2025 won’t necessarily have the fanciest offices or the most significant marketing budgets. They’ll have something better: financial systems that scale as fast as their ambitions. And that starts with four documented SOPs and the discipline to follow them.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Jan 21, 2026 | Blog

Picture this. You’re reviewing your quarterly numbers, feeling pretty good about things. Your biggest client—the one you’ve poured countless hours into—looks like it should be your most profitable relationship. Then you dig deeper. Factor in the partner’s time on those “quick” status calls. The proposal revisions that weren’t billed. The scope creep you absorbed to keep them happy. Suddenly, that flagship engagement is barely breaking even.

Sound familiar? You’re not alone. Most consulting firms are flying blind when it comes to true project profitability. They track time in one system. They run accounting in another. And somewhere in the gap between those two systems, profit quietly leaks out.

Here’s the thing: when time tracking and accounting actually talk to each other, you stop guessing and start knowing. You see which projects genuinely make money—and which ones are slowly eating your margins while looking healthy on the surface.

The Expensive Gap Between Time and Money

Your inventory, as a consulting firm, is time. That’s it. Unlike product businesses with warehouses full of widgets, you sell hours and expertise. Yet most firms treat time data and financial data as completely separate worlds. They log hours in Toggl or Harvest, run invoices through QuickBooks, and never quite connect the two in any meaningful way.

The costs that slip through this gap are insidious. Partner time on “quick reviews” that somehow stretch into hours. Proposal development that nobody thinks to track. Scope management conversations. Unbilled client calls. Internal meetings about the project that never make it onto anyone’s timesheet. These aren’t dramatic line items anyone notices. They accumulate quietly, like water damage behind a wall.

This profit blindness typically costs firms 15-25% of their potential margins. That’s not a typo. A quarter of your profits, potentially, vanishes into the space between two systems that don’t communicate.

One founding partner at a consulting firm put it bluntly after finally connecting their systems: “We had no idea our large regulatory projects were actually break-even when you factored in all the partner time.” Their most significant, most prestigious engagements—the ones they’d been proudly featuring in marketing materials—were barely keeping the lights on.

And there’s another cost beyond the profit leakage: your time. Most consulting firm owners spend 15-20 hours monthly on financial administration. That’s the late nights cross-referencing Toggl exports with QuickBooks reports, trying to figure out why the numbers don’t quite match. Phones ringing. Spreadsheets multiplying. The nagging feeling that something’s off, but you can’t pinpoint what.

What Real Integration Actually Looks Like

Let’s be clear about what we mean by integration. We’re not talking about exporting a CSV file from your time-tracking tool and importing it into your accounting software once a month. That’s manual data transfer with extra steps. Real integration means seamless, automatic flow between operational reality and financial truth.

Modern systems can sync directly with tools like Harvest, Toggl, Clockify, and TimeCamp. Every hour, your team’s logs are automatically logged into project profitability calculations. No exports. No imports. No reconciliation headaches.

This transforms time tracking from a billing function into a costing function. Instead of just knowing what to invoice, you know what the project actually costs—including the hours that weren’t billable but were definitely real—the senior consultant who reviewed deliverables. The admin time spent coordinating schedules—the project manager’s weekly check-ins.

The difference between real-time visibility and month-end reporting is the difference between steering a ship and reading about where it went. When your systems are integrated, you see margin erosion in real time. You catch the project that’s running hot before it becomes a problem, not thirty days after the damage is done.

Proper integration also means accurate overhead allocation. Non-billable time—admin work, marketing, and professional development—is appropriately spread across projects. You stop pretending these costs don’t exist and start understanding their real impact on each engagement.

One client described the shift this way: “System Six revamped our whole accounting system into accurate and dependable practices. Now I can pull up real-time insights about project profitability from my phone between client meetings.” That’s not a nice-to-have. That’s the information you need to make wise decisions in the moment—whether to push back on scope creep, when to have a pricing conversation, and which opportunities deserve your best people.

The Ripple Effects of Margin Clarity

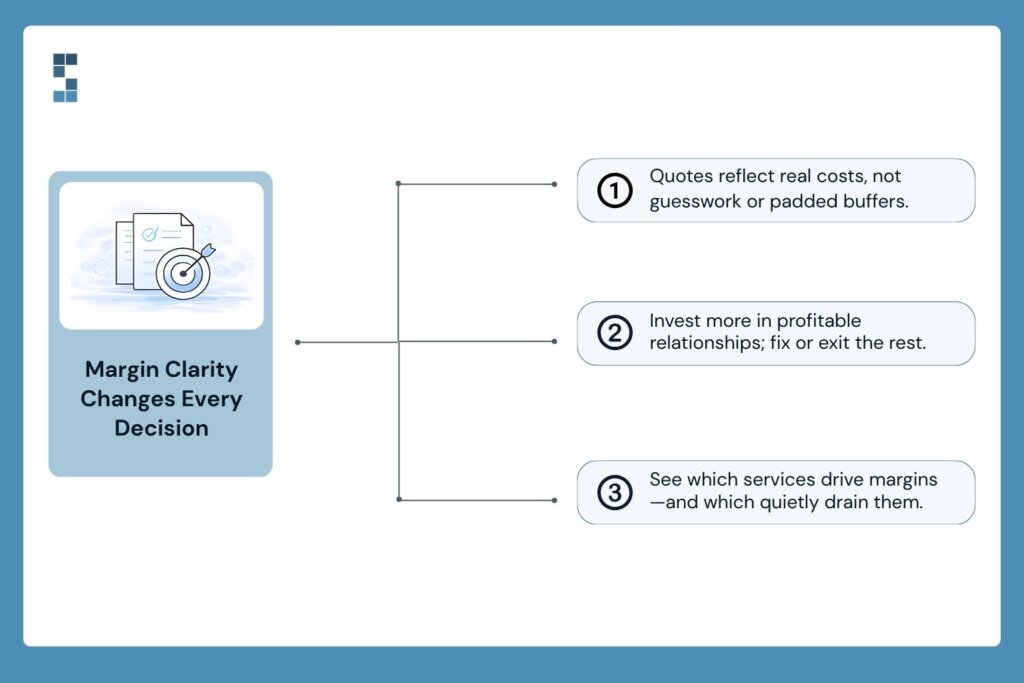

Knowing your proper project margins isn’t just about understanding the past. It transforms how you make decisions about the future.

Start with pricing. When you know your actual costs, you quote with confidence instead of hope. No more underpricing because you forgot to account for all the invisible work. No more padding estimates with arbitrary buffers because you’re not sure what things really cost. You price based on reality.

Then there’s client portfolio optimization. Which relationships deserve more investment? Which ones need a frank conversation about scope or rates? Without accurate margin data, these decisions are gut feelings. With it, they’re strategic choices backed by numbers.

Service line analysis becomes possible, too. You might discover that your strategy work generates twice the margin of your implementation projects—or the opposite. You find out which consulting offerings actually drive profits and which ones you’ve been subsidizing without realizing it.

And hiring? Hiring decisions grounded in data rather than anxiety. One firm gained such clear visibility into project profitability that they saw a 22% increase in average project margin simply by making better decisions about which work to pursue. That clarity gave them the confidence to open a second office and hire three new consultants. They knew exactly which project types to chase and had the cash flow visibility to make bold moves without holding their breath.

Here’s a quick gut check: can you answer “which of my projects had the best margin last quarter” within thirty seconds? If you’re reaching for a spreadsheet or mentally calculating, your systems aren’t integrated. That information should be at your fingertips.

Making It Happen

So how do you move from disconnected systems to genuine integration? Start with the process before the technology. Document your current workflows. Identify where time data and financial data diverge. Understand the gaps before you try to bridge them.

When evaluating tools, prioritize those that connect time tracking directly to financial reporting—not just export capabilities, but real-time sync. The difference matters more than you might think.

Be wary of the DIY trap. Improperly configured integrations often create more problems than they solve. You end up with data that looks connected but tells conflicting stories, which is arguably worse than having separate systems that you know don’t talk to each other. Working with experts who understand consulting firm economics—who know what project costing should actually look like in this industry—saves months of trial and error.

As one client put it: “I don’t have to think about my accounting. It’s just taken care of seamlessly.” That’s the goal. Not another system to manage, but one less thing demanding your attention so you can focus on the work that actually generates revenue.

The Bottom Line

Imagine walking into the next quarter knowing—with confidence—exactly which projects deserve your best people. Which clients merit a pricing conversation? Which service lines are worth expanding, and which need rethinking?? No more late-night spreadsheet archaeology. No more nagging uncertainty about whether you’re actually making money on your biggest engagements.

Your competitors aren’t necessarily more intelligent or more talented than you. Some of them have just built systems that show them the truth about their business. They see profit leaks before they become crises. They price with precision instead of hope. They make hiring decisions based on data, not anxiety.

For consulting firm owners ready to stop guessing and start knowing, connecting time tracking and accounting isn’t just an efficiency play. It’s a margin multiplier. And in an industry where your only inventory is time, knowing precisely what that time is worth might be the most valuable insight you can have.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Jan 14, 2026 | Blog

It’s Sunday evening. You’re sitting at the kitchen table with your laptop open, spreadsheets glowing in the dim light. Your kids are watching a movie in the next room. Your partner keeps glancing over, wondering when you’ll finally close that screen. But you can’t. Not yet. Payroll is due tomorrow, and you’re still reconciling hours, double-checking tax withholdings, and praying you didn’t miss anything for your remote consultant in California.

Is this really why you started your consulting firm?

You launched your business to solve problems, serve clients, and build something meaningful. Somewhere along the way, payroll became your second job. And it’s quietly stealing more than just your time—it’s draining the energy you need, actually, to lead your team.

The Hidden Cost of DIY Payroll

Payroll seems simple enough. Until it isn’t.

Most consulting firm owners spend between 5 and 10 hours per month wrestling with payroll-related tasks. That includes calculating wages, tracking deductions, filing taxes, and fixing the inevitable mistakes that crop up when you’re rushing through the process at 11 PM. Ten hours might not sound catastrophic. But multiply that by your hourly consulting rate, and suddenly you’re looking at thousands of dollars in opportunity cost every single month.

Then there’s the complexity. Maybe you started with a handful of local employees, and payroll was genuinely manageable. But consulting firms grow in unpredictable ways. That brilliant strategist you hired works remotely from Texas. Your new project manager lives in New York. And now you’ve got consultants scattered across multiple states, each with different unemployment insurance requirements, workers’ compensation rules, and tax withholding regulations.

Multi-state payroll isn’t just complicated—it’s a minefield. One misstep, and you’re facing penalties from agencies you didn’t even know existed.

But here’s what nobody talks about: the mental load. Even when you’re not actively doing payroll, it’s lurking in the back of your mind. Did I file that quarterly report? Did I classify that contractor correctly? Is someone going to call me about a discrepancy I missed three months ago? This low-grade anxiety follows you into client meetings, disrupts your focus during strategic planning, and keeps you checking email at midnight. Payroll errors don’t just cost money—they erode employee trust. Nothing damages morale faster than a missed paycheck or incorrect withholding. Your team shouldn’t have to wonder whether they can count on you for something this fundamental.

Why Payroll Delegation Changes Everything

Here’s the thing about delegating payroll: the benefits extend far beyond reclaiming those five to ten hours.

Yes, you get time back. That’s the apparent win. But what you really get is headspace—mental clarity. The ability to walk into Monday morning focused on landing that new client instead of fixing Friday’s payroll crisis.

When you hand payroll to professionals who live and breathe employment regulations across all fifty states, you’re not just outsourcing a task—you’re buying expertise you could never develop on your own. These are people who track legislative changes, understand nexus rules, and know precisely how to handle that tricky contractor classification question that’s been keeping you up at night.

The improvement in accuracy alone is worth the investment. One business owner working with System Six shared that when auditors reviewed their books, they found “exactly zero errors.” Zero. That’s not just impressive—it’s the standard you deserve when your professional reputation is on the line.

And then there’s the stress relief. Betsy, who runs an investor-backed business, put it simply: “System Six has done wonders for my stress level to feel like this is all now taken care of with a professional partner.” That feeling of having a professional partner—someone who genuinely has your back on compliance—is hard to quantify but impossible to overstate.

So let me ask you: what would you do with an extra ten hours a month? Land one more client? Finally, take that Friday afternoon off? Actually be present at your kid’s soccer game without your phone buzzing with payroll questions?

From Administrator to Leader—A Real Transformation

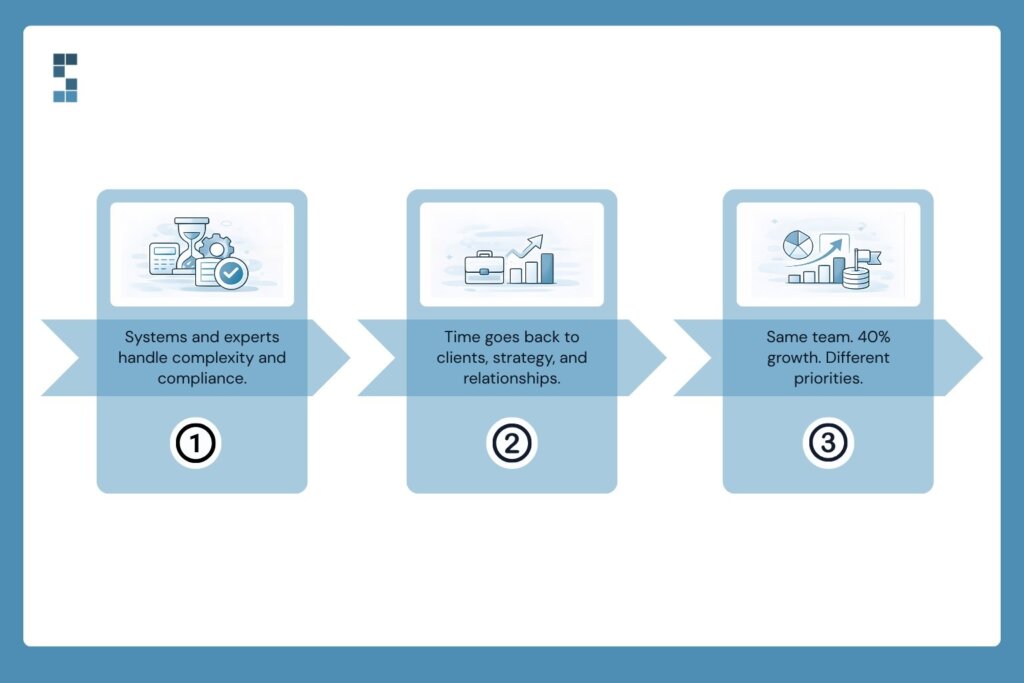

Delegation isn’t abdication. It’s strategic leadership.

Consider Mark’s story. He runs an environmental consulting firm, and before he made the switch, he was spending twelve to fifteen hours every week on financial tasks—payroll included. That’s almost two full workdays. Every single week. Disappearing into spreadsheets instead of serving clients or growing his business.

After partnering with a professional team to handle his finances and payroll, everything changed. Automated systems took over the tedious work. Multi-state compliance became someone else’s expertise. And Mark? He redirected all that reclaimed time toward what he does best: building client relationships and developing new business.

The result? His firm grew by forty percent the following year. Same administrative headcount. Dramatically different outcomes.

“Working with System Six to automate our finances changed everything,” Mark shared. “Now I can pull up real-time insights from my phone between client meetings. We’ve grown 40% this year because I can focus on clients instead of paperwork.”

That’s the fundamental transformation here. When you stop being the payroll administrator, you can finally start being the leader your team needs. The visionary who sets direction. The relationship builder who lands new accounts. The strategist who sees opportunities others miss. You didn’t hire yourself to process W-2s. You hired yourself to build something remarkable.

Making the Transition

Getting started is simpler than you might think.

Most consulting firms are fully operational with a new payroll partner within four weeks. That includes data cleanup, system integration, and getting everyone comfortable with the new workflow. If you’re already using QuickBooks Online, the timeline often shrinks to two or three weeks.

A good partner will coordinate seamlessly with your existing CPA. They’ll handle the multi-state complexity that’s been giving you headaches. And here’s the key: you maintain visibility without the burden of execution. You can still see everything happening with your payroll—you just don’t have to be the one making it happen.

Want a practical first step? Take fifteen minutes right now to calculate how many hours you spent on payroll last month. Be honest. Include the time you spent worrying about it, researching compliance questions, and fixing errors. Now multiply that number by your hourly consulting rate.

That figure represents the actual cost of DIY payroll to your business. Not just in dollars, but in opportunities you never had time to pursue.

Reclaim Your Role as Leader

You didn’t start your consulting firm to become a payroll administrator. You started it to solve problems, serve clients, and build something meaningful. Somewhere along the way, the administrative burden piled up until it threatened to bury the vision that got you here in the first place.

Delegating payroll isn’t about admitting you can’t handle it. It’s about recognizing that your time and energy are finite resources—and they deserve to be invested where they’ll generate the greatest return. For most consulting firm owners, that means client work, team development, and strategic growth. Not tax withholding calculations.

Stop spending evenings and weekends on payroll. Start focusing on what you do best: leading your team and growing your practice.

What would your business look like if you finally reclaimed those hours for actual leadership?

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

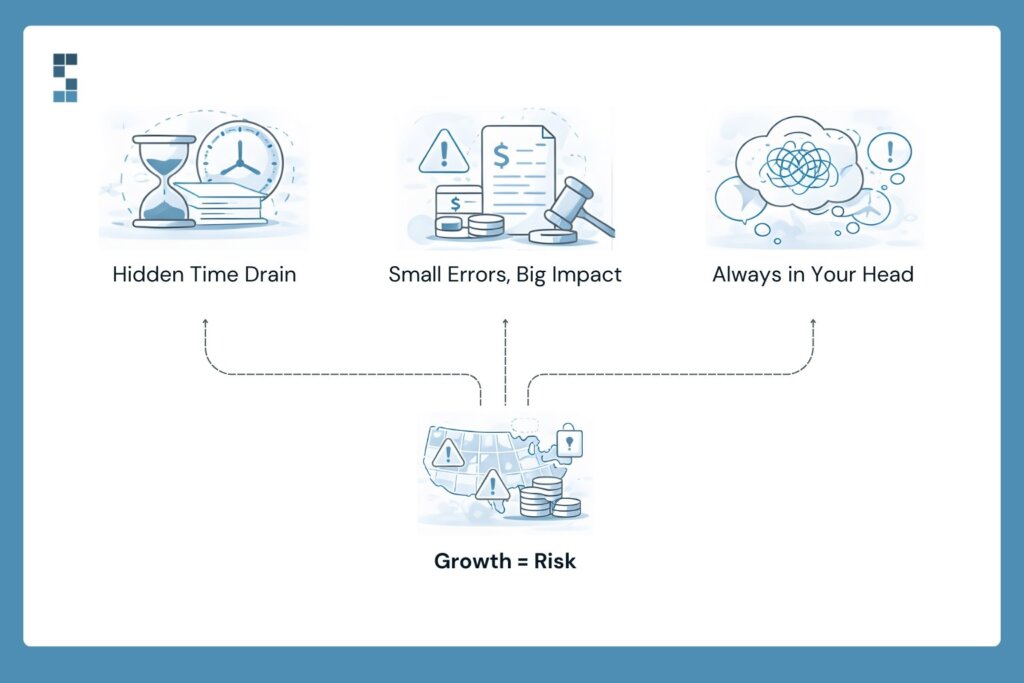

by Chris Williams | Jan 7, 2026 | Blog

It’s 11 PM on a Thursday, and your phone buzzes. It’s a client—one of your biggest—asking if you’ve seen the news about the data breach at a firm similar to yours. “Our board wants to know about your security protocols,” they say. “Can you send documentation by morning?”

Your stomach drops. Not because you’ve done anything wrong, but because you’re not entirely sure you can answer their questions with confidence.

Here’s the thing about running a consulting firm: you spend your days advising clients on risk management, strategic planning, and operational excellence. You know their businesses inside and out. But when’s the last time you took a hard look at your own financial data security?

You’re handling incredibly sensitive information every day. Client strategies that could move markets. Financial projections for acquisitions that aren’t public yet. Proprietary methodologies that took you years to develop. Your payroll data. Their billing details. All of it sitting somewhere in the cloud, accessed by your team from coffee shops, home offices, and airport lounges.

And in 2025, with AI tools and automation becoming standard practice in consulting operations, the questions around data privacy aren’t just theoretical anymore. They’re operational. Every time you or your team inputs financial data into a new platform or AI tool, you’re making security decisions—whether you realize it or not.

Protecting client confidentiality isn’t just about checking compliance boxes. It’s about preserving the trust that makes your consulting relationships possible in the first place.

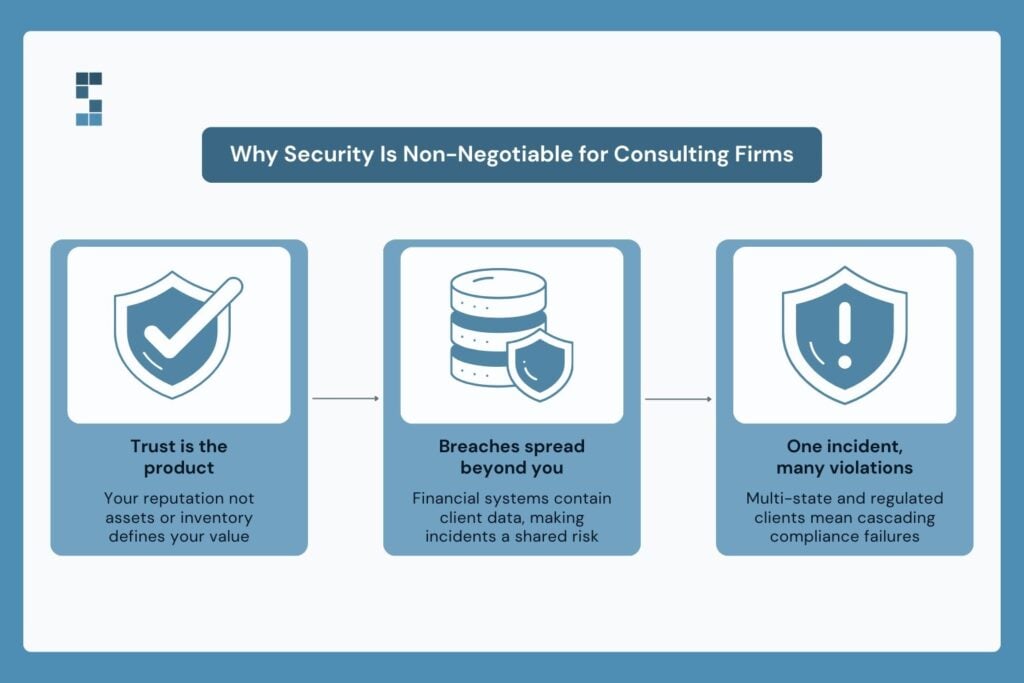

The Stakes Are Higher for Consulting Firms

Let’s be honest about what you’re really selling. Unlike product businesses, you don’t have inventory, patents, or physical assets that define your value. Your reputation IS your business. And that reputation is built entirely on trust—the kind of trust that lets clients reveal their competitive vulnerabilities, their expansion plans, their financial weaknesses.

Think about what’s in your financial systems right now. Not just your own firm’s data, but the interconnected web of client information embedded in project billing, expense reports, and invoices. A breach of your financial data isn’t just your problem. It’s potentially their problem too.

The regulatory landscape makes this even more complex. If you’re operating across multiple states—and most growing consulting firms are—you’re navigating a patchwork of different data protection laws. Got clients in healthcare? Financial services? Government contracting? Each of those industries brings its own security requirements that flow down to you. One breach doesn’t just trigger direct costs like forensic investigations and legal fees. It triggers a cascade of compliance violations across multiple jurisdictions and industries.

Then there are the costs most firms don’t see coming. Sure, you can calculate what cyber insurance might cover. But what about the proposals you don’t win because prospects chose a competitor with more robust security? The clients who quietly move on after learning about your weak data controls? The competitive disadvantage of not being able to answer security questions in RFPs confidently?

And here’s what keeps security experts up at night: consulting firms are increasingly attractive targets. You’re handling data from larger clients but often without enterprise-level security budgets. Cybercriminals know this gap exists. They’re counting on it.

Where the Gaps Usually Hide

Most consulting firm owners fall into what I call the DIY trap. Your financial data lives scattered across spreadsheets for projections, QuickBooks for accounting, separate systems for payroll, and maybe some PDFs floating around in email. Multiple team members access these systems from personal devices. Passwords get shared informally. And suddenly you’ve got a dozen potential entry points for problems.

There’s this persistent myth that small businesses are “too small to target.” Wrong. Automated cyberattacks don’t discriminate by firm size. They’re looking for vulnerabilities, not company headcount. Your financial software isn’t isolated—it’s a gateway to everything else in your operation, including client project data.

Walk through your current setup honestly. Do you have unsecured cloud storage where financial documents live? Are team members emailing sensitive payroll information as attachments? How many people have admin access to your accounting software—and do they all still need it? Is your data encrypted when it’s transmitted? Can you track who accessed which client’s billing information last Tuesday?

These aren’t theoretical questions. I’m talking about the consultant who discovered a former employee still had full access to their financial systems four months after leaving. Or the firm that couldn’t answer basic questions about data access during a client’s security audit and lost a $500K project because of it.

And now there’s the AI question. Consulting firms are rushing to adopt AI tools for efficiency—and they should. The technology can genuinely free you up to do more valuable work. But are you thinking through the security implications before you start feeding confidential financial data into these platforms? Many firms aren’t. They’re so focused on the productivity gains that they haven’t established clear policies on what data can go into AI systems and what can’t.

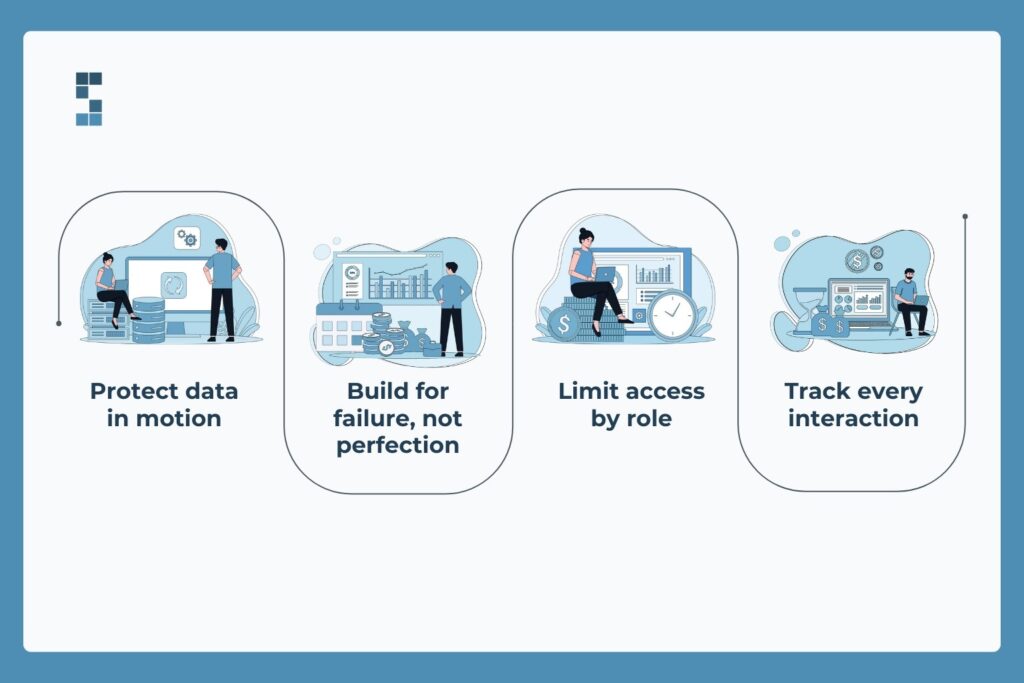

What Bank-Level Security Actually Means

You’ve probably seen vendors promise “bank-level security.” But what does that actually mean when you translate it from marketing jargon into operational reality?

Start with encrypted data transmission. Your financial data should be scrambled when it moves between systems—think of it like sending a locked safe instead of a postcard. This matters tremendously for remote teams accessing systems from wherever they happen to be working. That coffee shop WiFi? If your data isn’t encrypted in transit, you’re vulnerable.

Secure cloud infrastructure isn’t just about having data “in the cloud.” It’s about using infrastructure with real redundancy, automatic backups, and regular security audits. Your data should be recoverable if something goes wrong, not just accessible when everything works perfectly.

Restricted access protocols mean different people see different things based on their roles. Your bookkeeper doesn’t need access to strategic client data. Project managers don’t need to see everyone’s payroll. Multi-factor authentication should be standard, not optional. Sessions should timeout automatically. And someone should be reviewing who has access to what at least quarterly, removing access that’s no longer needed.

Comprehensive audit trails give you the ability to answer the question “who accessed this data, when, and from where?” in real time. This isn’t paranoia—it’s essential for compliance and investigation if something goes wrong. Consulting firms that work with clients in regulated industries know this firsthand. One firm noted they’re “experienced with consulting firms serving regulated industries” precisely because they understand these requirements aren’t negotiable.