by Chris Williams | May 12, 2026 | Blog

It’s Tuesday morning. Caroline pulls up her P&L on the office laptop and stares at the numbers. Revenue looks strong. Margins look fine. Her coffee’s gone cold while she scrolls through the same spreadsheet for the third time. So why does she feel like she’s flying blind every time her senior consultants ask whether they should chase a new account?

Here’s the thing. Her books are clean. Her bookkeeper is great. But the report in front of her tells her exactly one thing — what already happened. It doesn’t tell her whether the next big move is a smart bet or a slow disaster.

This is the gap most consulting firm owners hit somewhere between their fifteenth and fiftieth employee. The numbers come in on time. The reports look professional. But nobody’s sitting next to them helping interpret what those numbers actually mean for next quarter. That’s the difference between bookkeeping and financial advisory. And it’s a difference that, once you feel it, you can’t unfeel.

If you’ve ever closed your laptop at the end of a long day, wondering whether the decisions you’re about to make are the right ones — and whether the numbers you’re staring at can actually tell you — keep reading.

Bookkeeping shows the past. Advisory shapes the future.

Bookkeeping is the rearview mirror. It tells you, with precision and care, where you’ve been. That matters. Without accurate books, you’ve got nothing to plan against. But the rearview mirror doesn’t help you read the road ahead.

A financial advisor — someone who actually knows your business, your industry, and your numbers — does the harder work. They translate ledgers into a language you can use. They turn last month’s numbers into next month’s decisions. They ask the questions you’re too tired or too close to ask yourself.

One System Six client put it perfectly. Working with us, he said, gives him “an outside view, a 35,000-foot look at what you’re doing that isn’t possible from the inside out.” That outside view is the whole point. When you’re elbow-deep in client work, you can’t see the patterns shaping your firm’s trajectory. Someone has to be looking from above. Someone has to be doing that for a living, across dozens of firms like yours, every single week.

Think of it this way. Your bookkeeper builds the dashboard. Your advisor helps you drive the car. Both are essential. Neither replaces the other. But too many firm owners think they only need the dashboard — and then wonder why they keep ending up in the wrong lane.

What a financial advisor actually does for you

So what does this person do, day to day, that earns the title “strategic”?

They forecast. Real forecasting — not a once-a-year budget you stop looking at by February, but a rolling thirteen-week cash flow that updates as reality shifts. They show you when money lands and when it leaves so that you can hire ahead of demand instead of behind it. They build a financial picture that breathes with your business, not one frozen in last quarter’s assumptions.

They model decisions before you make them. Should you take on the multi-state retainer? Open a second office? Bring on two senior consultants and a junior? A good advisor runs the math, surfaces the risks, and walks you through the scenarios. Marcus, one of our clients in the search fund world, put it like this: “I am in good hands with System Six, and I especially appreciate how they are inquisitive, ask follow-on questions, and look around corners.” Looking around corners. That’s the job.

They flag what you missed. They noticed the project that looked profitable but really wasn’t once you factored in partner oversight. They catch the slow drift in utilization before it shows up in the bottom line. Paul, another client, said it best: “S6 has been proactive at catching mistakes I’ve made or seeing challenges coming down the pike and asking me the right questions.”

Right questions. Not magic. Just experience, applied to your situation, before you trip. And it’s experience built across many businesses, not just one — patterns you can’t see from the inside of a single firm, but ones that jump out when you’ve watched dozens of firms scale and stumble.

What this looks like in real life

Back to Caroline. A few months into working with a financial advisor, she’s facing a real decision. A regional health system has offered her firm an eight-month engagement worth $1.4M. The work fits. The team can deliver. The problem? It requires hiring two senior consultants right now, and the engagement won’t start paying out for sixty days.

The old Caroline would have either said yes on instinct and prayed that cash held up, or said no out of fear and watched the opportunity walk away. The new Caroline has someone in her corner.

Her advisor pulls up the rolling forecast. They walk through three scenarios: full hire, phased hire, and contractor blend. They show her exactly which weeks would be tight, where the credit line might need to flex, and when the first invoice clears. They model what happens if the client pays on day forty-five versus day sixty. They flag the payroll cycle that lands right when receivables would be thinnest. By the end of the conversation, Caroline isn’t guessing. She’s deciding with data.

She takes the engagement. She structures the hiring in phases. Cash never wobbles. The firm grows by 22% that year, and she sleeps through the night.

This is the quiet, compounding value of advisory. It’s not flash. It’s not a single big save. It’s the steady, weekly removal of guesswork from the decisions that define your business. Over a year, that adds up. Over five years, it changes the trajectory of the whole firm.

The compounding return of clarity

Here’s the part most firm owners underestimate. Strategic financial guidance isn’t a luxury you graduate to at $10M in revenue. It’s the very thing that gets you there.

The firms that outpace their peers aren’t necessarily the ones with the best consultants or the slickest brand. They’re the ones whose owners spend less time wondering and more time deciding. Less time staring at a P&L and asking “what does this mean?” More time saying “here’s our next move.”

That clarity has a name. It’s the financial advisor in your corner — the one who knows your business deeply enough to spot the trends before you do, and who’s been around enough firms like yours to know which moves work. The one who picks up the phone when you’re not sure whether to take the contract, hire the senior, or restructure the partner draws. Not because they’re cheaper than a full-time CFO, though they usually are. Because they’re often more curious, more honest, and more useful, across more than 175 businesses, our team has watched what works and what doesn’t — and that perspective shows up in every client conversation.

So here’s the question worth sitting with. When you look at your firm’s next big decision — the hire, the office, the new service line — are you guessing, or are you deciding?

If it’s still the first one, it might be time to put someone in your corner.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | May 5, 2026 | Blog

Caroline thought she’d solved her bookkeeping problem.

She runs operations at a 22-person consulting firm in Denver. For the first two years, she handled the books herself, along with everything else. Last spring, she finally hired a part-time bookkeeper — someone good, someone affordable, someone who showed up every Tuesday and reconciled the accounts cleanly.

The reconciliations were perfect. She still missed the 1099 deadline. Payroll questions still landed on her desk at 6 PM. When her CEO asked for a breakdown of project profitability in March, the bookkeeper said it wasn’t really her thing.

Here’s what Caroline learned the hard way: most owners shop for bookkeeping when what they actually need is a finance function. Those are different products. The visible benefits of full-service support — accurate books, on-time payroll — are the surface. The hidden value is what makes it worth paying for. Let’s get into it.

Coverage That Doesn’t Take a Vacation

The first hidden benefit nobody asks about until it bites them: continuity.

When you hire one bookkeeper, you’ve hired one bookkeeper. They get sick. They take their kid to the dentist. They quit. A friend of mine spent three weeks last December trying to find someone to cover her solo bookkeeper’s maternity leave. Payroll went out late. Two vendor invoices got missed. It was a mess.

A full-service team works differently. Multiple people know your books. Somebody is always on. When your primary contact is out, the work doesn’t stop — it shifts. Quietly. Without you having to chase anyone down.

This is partly why System Six clients tend to describe the relationship in family-like terms. Rebecca, who runs operations at a Pacific Northwest services firm, put it this way: “System Six isn’t just a vendor; they’re friends who feel like part of our team.” That kind of language only shows up when continuity is built in. You can’t feel like part of someone’s team if you disappear when one person catches the flu.

The practical version is simple. Caroline eventually switched to a full-service provider. Last August, she went on vacation to Spain for ten days and didn’t check her email once. Payroll ran. Bills got paid. A vendor dispute got handled by someone who knew the account. She came back to a clean inbox. That had never happened before.

What continuity actually buys you is permission to step away. Most owners don’t realize how much of their week is quietly structured around being available — not doing their own finance work, but serving as the backstop in case something goes sideways. A team-based model removes that gravitational pull. The phone stops being something you check at dinner. The Sunday-night dread fades because you know somebody is already on it.

Looking Around Corners

The second hidden benefit is harder to put on an invoice.

A search-funded CEO named Marcus once described his finance team this way: they’re inquisitive, they ask follow-on questions, and they look around corners. That last phrase is the whole game. A transactional bookkeeper records what happened. A full-service team notices what’s about to happen.

The difference shows up in small ways that compound. One System Six client was bleeding $700 a month in overdraft fees nobody had flagged — until somebody did. Another was Paul, who runs a search-fund-backed company. After his 2022 audit, the auditors found exactly zero errors in two years of books. He’s told people more than once that hiring a full-service team was the best decision he made at the start of the business.

Stories like that aren’t about heroic bookkeeping. They’re about the work’s basic posture. When the same team handles your bills, payroll, reporting, and cleanup, they develop a feel for your business. They notice when a recurring vendor charge jumps. They notice when a contractor’s invoice looks off. They notice when your gross margin slips by 2 points and bring it up before you have to ask.

That’s one of the more underrated outsourced finance advantages — you stop being the only person paying close attention to your own numbers. Somebody else is watching, and they’re trained to notice things you wouldn’t.

When Everything Talks to Everything

The third hidden benefit is structural. It’s about what happens when one team owns the whole pipeline.

Caroline’s old setup had three vendors and four logins. Her bookkeeper handled the books. A separate payroll service handled payroll. A bill-pay tool handled AP. Her CPA handled taxes. Nothing reconciled cleanly because nobody owned the handoffs. Every month-end was a small archaeological dig — figuring out which numbers from which system matched which other numbers. The handoffs were where things broke.

Full-service consolidates ownership. When bookkeeping, payroll, AP, reporting, and controllership all live under one roof, the data is already connected. The team that processes payroll is the team that books it. The team that pays the bills is the team that reports on cash flow. Decisions get faster because nobody has to email three vendors to assemble a clean picture.

This is the part that sneaks up on people. The full-service bookkeeping benefits aren’t just about saving hours — they’re about removing friction. System Six clients typically see a 70-80% reduction in administrative time within 90 days. But the time number only tells half the story. The other half is what disappears: the back-and-forth, the reconciliation gaps, the quarterly scramble to figure out where everything is. All of it goes quiet.

Month-end is where this shows up most clearly. With a fragmented setup, closing the books is a project — chasing down statements, reconciling between systems, and asking three different vendors to confirm the same number. With a full-service team, close happens in the background. You get clean financials on a predictable cadence, and you stop scheduling your life around the second week of every month.

What’s left is a finance function that runs in the background. You stop having to hold the whole picture in your head. That’s a different way to live.

The Shift in How You Think About Finance

Here’s what I’d tell Caroline now, looking back. Full-service financial support isn’t a premium tier of bookkeeping. It’s a different operating model. You’re not buying more hours from a bookkeeper — you’re buying out of an entire category of cognitive load.

The hidden value is what you stop having to think about. The compliance deadline. The missing invoice. The question of whether last month’s numbers can be trusted. The vendor who emailed twice and got ignored. The payroll question your office manager doesn’t know the answer to—all of it. Gone, or at least handed off to people whose job is to handle it.

So the question isn’t really whether you can afford full-service support. It’s whether you can afford to keep running your finance function as a collection of disconnected tasks held together by your own attention. Because attention is the resource you’re actually short on. Everything else is downstream of that.

If you’ve been running the math on what your finance function is costing you in time, distraction, and missed catches — and you’ve decided the answer matters — that’s worth a conversation.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Apr 27, 2026 | Blog

When Nathan started his strategy consulting firm in 2018, he knew exactly where every dollar went. He had to. With four colleagues in a co-working space and a single QuickBooks login, the financial side of his business fit on one Excel tab. He’d reconcile accounts on Sunday nights with a glass of wine. It felt manageable. Almost charming.

Six years later, his firm has 50 employees across 3 states, 14 active client engagements, and a finance function that bears no resemblance to that cozy spreadsheet. The journey from there to here wasn’t a straight line. It was a series of breaking points, each one forcing Nathan to rebuild something he thought was already working.

This is his story. Or really, it’s the story of every consulting firm that’s tried to grow past the boutique stage because the financial systems that get you to ten employees won’t get you to fifty. And the ones that get you to fifty look almost nothing like what you started with.

The Five-Employee Era: When Everything Fits in Your Head

In the early days, Nathan ran his finances by feel. Invoices went out when projects wrapped. Expenses got reimbursed when someone remembered to submit them. Payroll was a Wednesday afternoon ritual. His “cash flow forecast” was a mental note about which clients owed what.

This worked. Not beautifully, but it worked. When you can name every client and remember every contract value, you don’t need infrastructure. You need attention. And Nathan had plenty of that.

But here’s the thing about boutique-stage finance: it’s deceptive. The simplicity isn’t a feature. It’s a function of size. The moment your firm grows past the point where one person can hold every detail in working memory, the cracks start to show. They just don’t show all at once.

The Fifteen-Employee Breaking Point

Nathan’s first reckoning came around employee fifteen.

He was on a call with a prospective client when his office manager texted: payroll wouldn’t run because the operating account was $8,000 short. Two large invoices were stuck in the client’s AP department. A vendor had auto-debited a renewal he’d forgotten about. The math caught up with him.

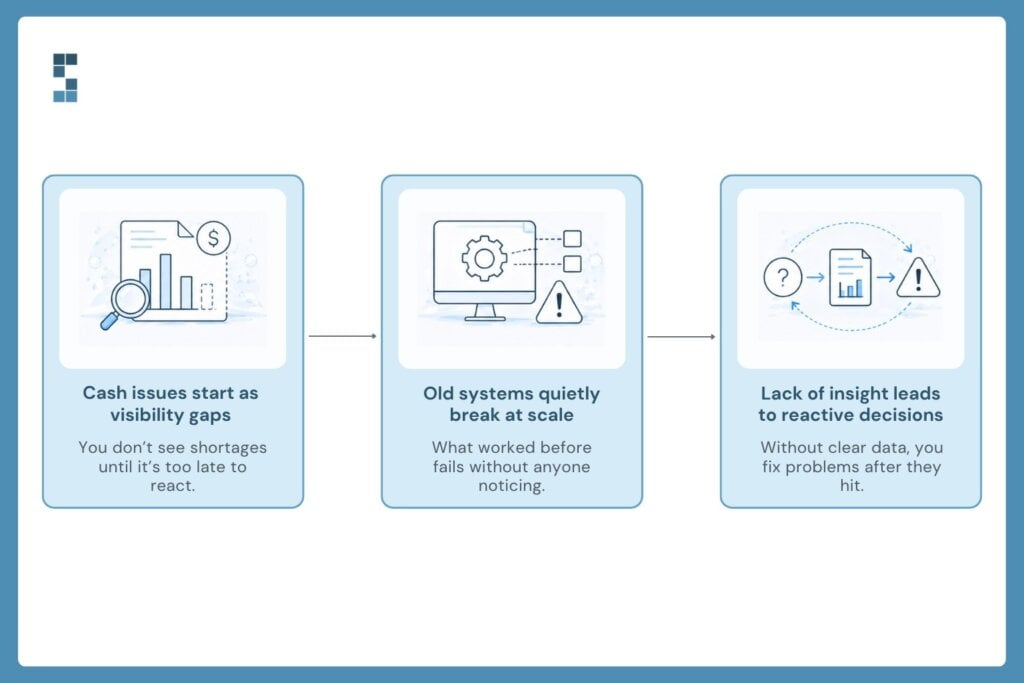

He moved money from his personal savings that day. He’d done it before. But this time, something shifted. He realized he hadn’t just had a cash flow problem. He’d had a visibility problem. By the time he saw the shortfall, it was already happening.

This is the part of the scaling story most owners don’t talk about. The crisis doesn’t announce itself. It hides inside processes that worked yesterday but stopped working sometime last quarter, and nobody noticed because everyone was busy serving clients.

Around the same time, one of Nathan’s senior consultants ran a margin analysis on a project they thought was their crown jewel. Six months of work for a Fortune 500 logistics company. Big logo, bigger billings. When she factored in partner oversight, scope creep, and the proposal time nobody had tracked, the project margin came in at seven percent. They’d been celebrating a loser.

That’s when Nathan called System Six.

Building the Systems for the Firm You’re Becoming

The first thing System Six did was something Nathan hadn’t expected. They didn’t fix his books. They asked about his next two years.

How many employees did he plan to hire? Which service lines was he investing in? What did his ideal client mix look like? The questions felt strange coming from an accounting firm. But the logic was simple: there’s no point building financial infrastructure for the firm you have today. You have to build for the firm you’re becoming.

Over the next twelve weeks, the transformation moved in phases. Real-time project profitability tracking came first, so Nathan could finally see which engagements made money after capturing every cost. Then came twelve-month cash flow forecasting tied to his project pipeline, the kind that would have flagged that payroll shortfall weeks in advance. Automated workflows replaced the manual reconciliation Nathan used to do on Sundays. Multi-state payroll compliance got handled before he hired his first remote employee in Texas.

One System Six client put it this way after a similar transformation: “Hiring them was the best decision I made at the start of the business. We just finished our 2022 audit, and the auditors found exactly zero errors.” Nathan didn’t believe a clean audit was possible until he had one. System Six has run this same kind of transformation for more than 175 businesses, and the firm’s net promoter score sits at 9.5 out of 10. The pattern isn’t an accident.

What Fifty Employees Actually Looks Like

Today, Nathan runs a different kind of business. Not because the work is different. The work is recognizably the same. But the operating system underneath has been rebuilt.

He knows his project margins by Friday afternoon, not three weeks after engagements close. He knows which clients are profitable enough to take more of, and which need contract restructuring before he renews. He knows his cash position twelve months out, with confidence intervals he actually trusts. When a senior consultant pitches him on a new hire, he can model the decision in twenty minutes instead of agonizing for a quarter.

The numbers tell part of the story. Nathan’s firm has reclaimed roughly fifteen hours a month from administrative work, which at his blended rate translates to six figures in recovered billable capacity each year. Project margins are up twenty-two percent because the unprofitable work is finally visible. Cash flow surprises, the kind that used to wake him up at 4 AM, have effectively stopped.

But the part he talks about most isn’t financial. It’s the silence. The mental bandwidth that used to go toward worrying about reconciliations, payroll, and whether that big invoice had cleared. That bandwidth is back. He uses it to think about his clients, his team, and what the firm should look like with a hundred employees.

One System Six client said something that stuck with Nathan: he appreciated how the team was inquisitive, asked follow-up questions, and looked around corners. That phrase, look around corners, captures something important. Good financial infrastructure isn’t reactive. It’s anticipatory. It catches the problems before they become emergencies.

The Lesson Hidden in the Story

Here’s what Nathan would tell you if you caught him on a good day. Every consulting firm that scales past the boutique stage hits the same wall. The wall isn’t a market problem. It isn’t a talent problem. It’s a financial visibility problem dressed up as something else.

You can either rebuild your systems before you hit the wall, or rebuild them while you’re hitting the wall. Both options eventually get you through. Only one of them lets you sleep.

So if you’re somewhere on the path between five employees and fifty, and your finances still fit on a spreadsheet, ask yourself an honest question. What’s your version of Sunday night reconciliation? What’s the cash flow surprise that hasn’t happened yet? What’s the project you think is profitable that isn’t?

The answers are worth more than you think. And the firm you’re trying to build is counting on you to find them.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialise in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Apr 22, 2026 | Blog

It’s 9:47 on a Thursday night. Rachel, who runs a 22-person consulting firm in the Pacific Northwest, has the kids asleep, a glass of wine poured, and QuickBooks open on her laptop. Again. She’s reconciling with June. It’s October. Her current bookkeeper is fine, technically. Nothing’s on fire. But nothing’s clean either, and Rachel has been thinking about switching for almost a year.

She hasn’t pulled the trigger. Why? Because switching feels like surgery. You’re convinced the operation will fix the thing that’s been bothering you, but you’re equally convinced it’ll leave you worse off before it leaves you better.

Here’s the secret nobody tells you: that story is mostly wrong. The real switch looks nothing like the disaster you’ve been picturing. Let’s walk through what actually happens, week by week, so the next time you find yourself at the kitchen table at 10 p.m., you can stop debating and start deciding.

The Fear Is Doing Most of the Work

Ask ten consulting firm owners why they haven’t switched bookkeepers yet, and you’ll hear some version of the same thing. “It’ll take forever to get them up to speed.” “What if they mess up payroll?” “My current person knows all our weird stuff — the retainer math, the expense reimbursements, the contractor 1099s.” Sound familiar?

None of these worries is crazy. They’re just bigger in your head than they are in reality. A well-handled switch looks more like hiring a new operations lead than like demolishing your house. Your data doesn’t disappear. Your vendors don’t get confused. Your team keeps getting paid. And the “weird stuff” you’ve been explaining for years? A good bookkeeping team has seen it all before, usually in ten other firms just like yours.

One System Six client, Manish G., described his experience bluntly. After his previous freelance bookkeeper left him with misfiled payroll taxes and an invoicing mess, he was convinced things couldn’t get worse, and certain switching would at least be painful. Instead, the new team — in his words — literally saved my business from falling into operational ruins. The part he expected to hurt turned out to be the easiest step he’d taken all year.

So what does that step actually look like?

Weeks One Through Four: Foundation and Stabilization

The first month has one job: take the weight off your shoulders. On day one, a dedicated team takes over your monthly bookkeeping, bank reconciliations, and payroll processing. You don’t hand over a thumb drive and hope for the best. You get a kickoff call, a document checklist, and someone who actually owns the migration from end to end.

The kickoff itself is less dramatic than you’d expect. Usually, a 45-minute call, a shared folder, read-only access to your existing systems, and a short list of things they need from you — bank statements, a copy of your current chart of accounts, a list of vendors and contractors, and any payroll history. That’s most of it. You’re not spending your weekend pulling files.

Behind the scenes, a lot happens quickly. If you’re already on QuickBooks Online, the transition typically wraps up in 2 to 3 weeks. If you’re migrating from desktop QuickBooks, Xero, or — let’s be honest — a spreadsheet held together with hope, expect about four weeks. Your chart of accounts gets optimized for how consulting firms actually work: projects, retainers, milestone billing, and expense reimbursements. Bank feeds connect. Bill-pay tools like Ramp get wired up. Payroll moves onto whichever platform makes the most sense for your team, whether that’s Gusto or something you already use.

Here’s the part that surprises most firm owners. While all of this is happening, almost nothing about your day changes. Your team still gets paid on time. Your vendors still get their checks. Clients still get invoices. You just stop being the bottleneck.

If your books have been messy for a while — most are — there’s also a cleanup phase happening in parallel. Prior-month reconciliations get caught up. Miscategorized expenses get sorted. Orphaned transactions get chased down. None of this lands on your desk. You get a summary at the end of the month showing what was found and fixed, and the books quietly become something you can actually trust.

By the end of week four, you have clean books, automated workflows humming quietly in the background, and — maybe for the first time in years — a dashboard that shows you where you actually stand.

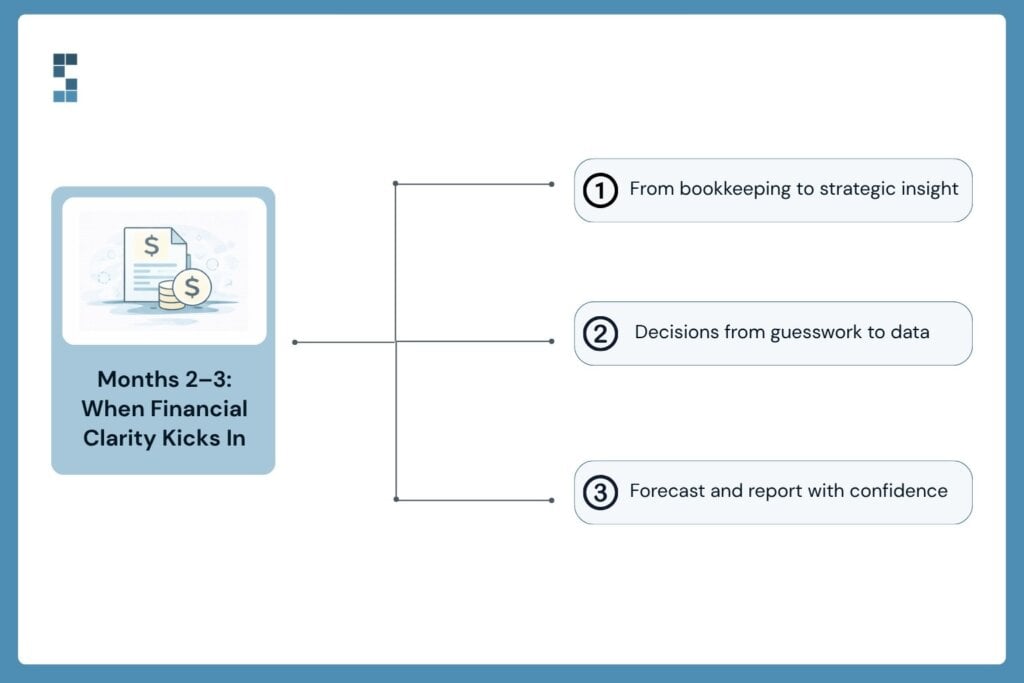

Months Two and Three: The Good Part

Once the foundation’s in, the real value shows up. This is where the firm you hired stops feeling like a vendor and starts feeling like a finance team.

Project-based profitability tracking gets layered in. If you use Harvest or Asana for time and project management, they integrate with your accounting, so you can finally see which engagements make money and which quietly eat partner hours. Cash flow forecasting extends out twelve months. Monthly reporting starts arriving on a schedule you don’t have to chase.

One environmental consulting firm went through exactly this sequence. By month three, they could see — for the first time — that their mid-sized engagements were 40% more profitable than the big flagship projects they’d been chasing. That single insight reshaped their entire business development strategy. It also, as the founding partner put it, paid for the service several times over in the first year alone.

What does this mean for you? You stop making strategic decisions on gut feel. You know what to price higher. You know who to hire next. You know when to say no.

What It Actually Costs to Not Switch

Here’s the part nobody likes to talk about. Every month you don’t make the change, you’re paying for it, just not in invoices.

Consulting firms working with System Six save roughly 15 hours a month on financial administration. At a partner billing rate of $250 an hour, that’s $45,000 a year in reclaimed time. Multiply that by the years you’ve been thinking about switching. The number gets uncomfortable fast.

And it’s not just hours. It’s the client proposal you didn’t write because you were chasing a missing receipt. It’s the hire you delayed because you couldn’t tell whether the firm could afford the new seat. It’s the Friday nights.

JT C., a long-time client, put it this way: had I only switched sooner, I am sure my business outcomes would have been substantially different. Over 95% of System Six’s consulting clients renew year after year, which tells you something important. Once firms feel what clean books and reclaimed evenings actually feel like, going back isn’t on the table.

The Real Takeaway

Switching bookkeeping providers isn’t the operation you’ve been picturing. It’s four weeks of structured, mostly invisible work that ends with your evenings back, your data clean, and your strategic questions finally answerable.

The question isn’t whether the switch will hurt. It won’t. The question is how many more Thursday nights at the kitchen table you’re willing to trade for a decision that, six weeks from now, you’ll wish you’d made a year ago.

Ready to see what your transition would actually look like? A complimentary consultation walks you through your current setup, identifies what changes are needed, and shows you a realistic timeline. No pressure, no surprises. The hardest part really is deciding to have the conversation.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialise in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Apr 13, 2026 | Blog

You spent weeks vetting your bookkeeping provider. You compared pricing, checked reviews, and asked about software integrations. But here’s the question most consulting firm owners never think to ask: who else can see your books?

Think about what’s actually sitting in your financial management system. Payroll records with every employee’s salary. Client invoices that reveal your billing rates and biggest accounts. Bank feeds with your cash position laid bare. Tax filings. Expense reports. The full financial anatomy of your business, open and readable — somewhere on someone’s server.

Most business owners scrutinize pricing before they scrutinize security. That’s understandable. Pricing is easy to compare; security practices take a few more questions. But the wrong provider — one with lax access controls, no formal compliance standards, or vague data policies — can expose your firm to breaches, regulatory liability, and the kind of reputational damage that doesn’t go away quickly.

The good news: you don’t need to become a cybersecurity expert to protect yourself. You just need to know which questions to ask.

What’s Actually at Risk

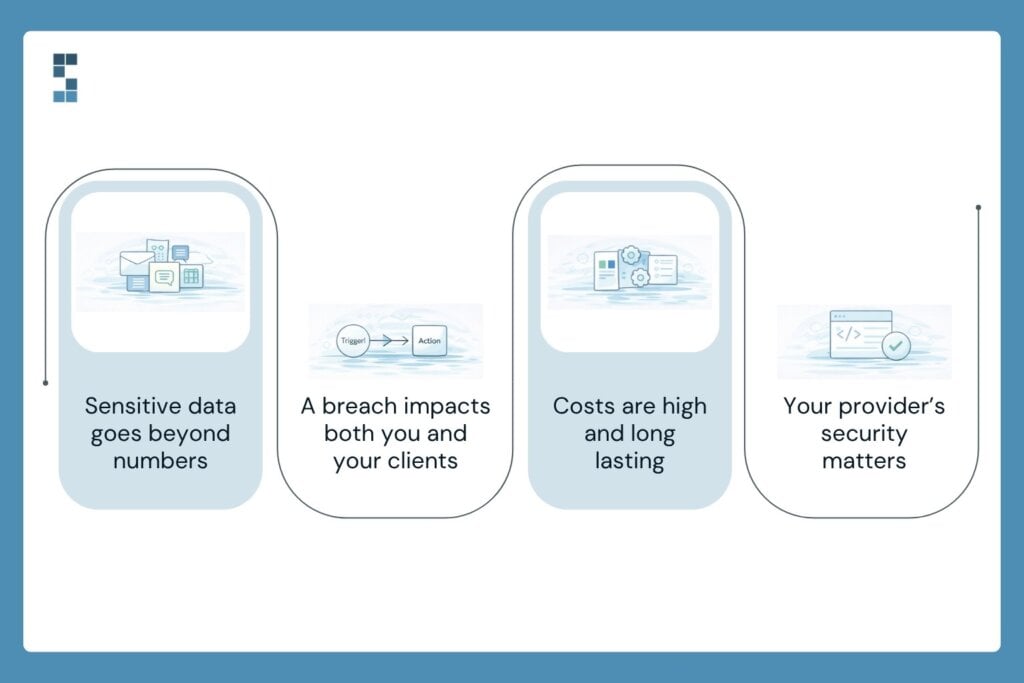

“Financial data” sounds abstract until you list out what it actually contains. Payroll files. Employee tax IDs. Vendor contracts. Bank account numbers. Profit margins. Cash flow projections—client billing history.

For a consulting firm, the stakes go beyond your own exposure. Your clients trust you with their business, and your financial records often reflect that relationship — engagement fees, scope of work, duration of contracts. A breach doesn’t just hurt you. It ripples outward.

And the costs aren’t theoretical. According to IBM’s Cost of a Data Breach Report, the average breach for a small business now runs well into six figures when you factor in forensics, notification requirements, regulatory fines, and lost business. For a firm operating in a trust-driven industry — and consulting is exactly that — the reputational toll can outlast the financial one.

The question isn’t whether your data is worth protecting. It obviously is. The question is whether your current provider takes that seriously.

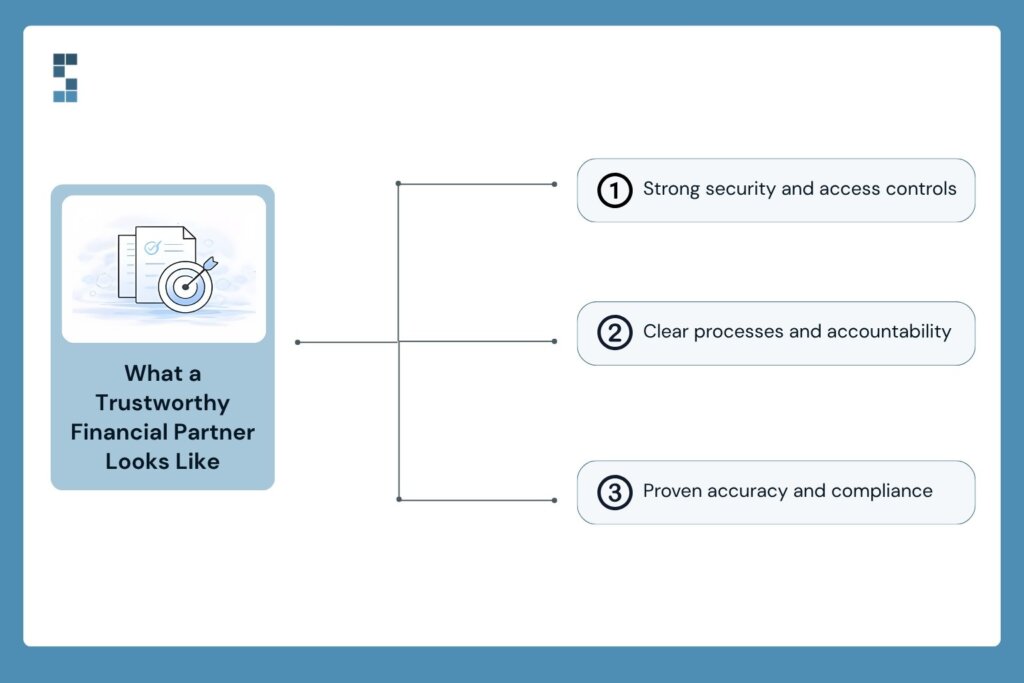

The Questions You Should Be Asking (But Probably Aren’t)

Most providers won’t volunteer this information upfront. You have to ask. Here’s what to put on your list.

How is my data encrypted — in transit and at rest? This is the baseline. Data in transit means information moving between your systems and theirs; data at rest means information stored on their servers. You want encryption at both stages. If a provider can’t give you a clear answer here, that tells you something.

Who on your team has access to my accounts, and how is that controlled? The biggest security risks are often internal, not external. A well-run provider restricts access on a need-to-know basis — only the team members actually working on your account should be able to see your data. Ask whether they use role-based access controls and whether access is logged and audited.

Are you SOC 2 compliant, or do you follow an equivalent security standard? SOC 2 compliance — developed by the American Institute of CPAs — is the gold standard for service organizations handling sensitive client data. It requires third-party audits of a firm’s security, availability, and confidentiality controls. Not every bookkeeping provider will be SOC 2 certified. Still, the question itself is useful: a provider who understands what it means and has given it serious thought is a different animal from one who’s never heard of it.

What happens to my data if I decide to leave? This one surprises people. A surprising number of firms have no clear policy on data offboarding — meaning your financial records might sit on their servers indefinitely after you’ve moved on. You want a provider who can give you a clean data export and confirm deletion within a defined timeframe.

How do you handle a breach or security incident? No system is perfectly immune. What matters is how a provider responds when something goes wrong. Ask whether they have an incident response plan, how quickly they notify clients, and what remediation looks like. Vague answers here are a red flag.

What Good Answers Look Like

Ask those questions, and you’ll quickly learn to read the room. A provider worth trusting will answer them without hesitation — and often with specifics.

Bank-level encryption for data in transit and at rest. Role-based access controls so your account isn’t visible to everyone on a 40-person team. Signed confidentiality agreements for every staff member who touches client data. A clear, documented process for data export and deletion when an engagement ends. And some form of formal security framework guiding how they operate.

System Six, for instance, uses bank-level security with encrypted data transmission, secure cloud infrastructure, and comprehensive access controls. Every team member signs a strict confidentiality agreement. These aren’t marketing bullet points — they’re the baseline that any firm managing six-figure payrolls and sensitive financial records should be able to demonstrate.

The outcomes speak for themselves. Paul, a search fund operator who uses System Six, put it plainly:

“We just finished our 2022 audit, and the auditors found exactly 0 errors by S6. Not only have they been mistake-free, but S6 has also been proactive at catching mistakes I’ve made or seeing challenges coming down the pike and asking me the right questions to keep the books updated.”

Zero errors in an external audit isn’t just an accuracy story — it’s a compliance story. It means the systems are clean, the controls are working, and nothing is being glossed over. That’s what security and accuracy look like in practice.

It’s worth noting that System Six earns a 9.5 out of 10 NPS from its clients — and more than half of new clients come from referrals. In a trust-driven industry, that number doesn’t happen by accident.

The Foundation Is Trust

Here’s the thing about financial data security: it’s not just an IT issue. It’s a trust issue. Your clients trust you. You should be able to trust the people managing your finances.

The firms that ask these questions before signing are the ones that avoid the firms that deserve to be avoided. You now have the questions. Use them in your next provider conversation—or to evaluate the one you already have.

And if you’re looking for a provider who’s already thought through the answers, we’d be glad to walk you through how System Six approaches security, compliance, and client confidentiality—no long-term contracts. No runaround. Just straight answers.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialise in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Apr 6, 2026 | Blog

The invoice arrives on a Tuesday morning, right when you’re prepping for a client call. You open it expecting the usual number — the one you’ve mentally budgeted for — and it’s $380 more than last month. No explanation. Just more hours. You pay it, because what else are you going to do? But somewhere in the back of your mind, a question starts forming:

Is this really the best way to handle my books?

If you’ve been running a consulting firm for more than a year or two, you’ve probably wrestled with this. The question of how your bookkeeper charges you might seem like a minor operational detail. It isn’t. The engagement model you’re on shapes your cash flow predictability, your incentive alignment with your financial team, and — critically — whether your back-office infrastructure can actually keep pace as your firm grows. Fixed fee or hourly? It’s worth thinking through carefully.

How Hourly Billing Works – And Where It Starts to Break Down

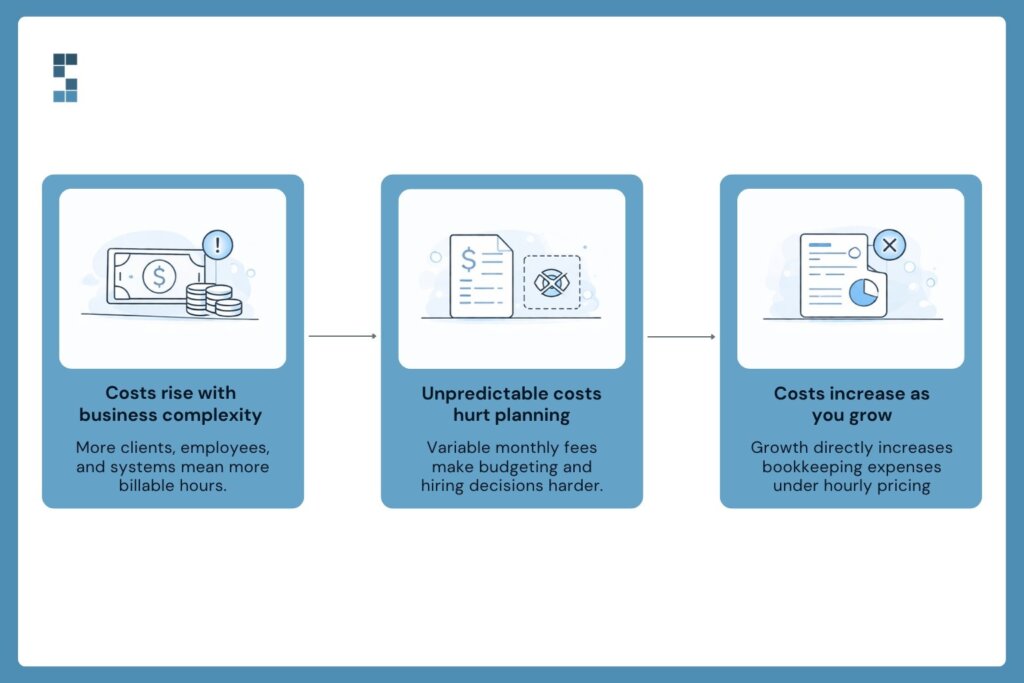

Hourly billing is simple enough in theory. Your bookkeeper logs time, and you pay for what they use. At the start, especially when your transaction volume is modest and your needs are straightforward, it can feel like the sensible option. You’re not locked in. You’re not paying for more than you need.

But here’s the thing about consulting firms: they don’t stay simple. You land a new retainer client, your revenue model shifts from pure project-based to a mix of retainers and milestones, you add your third full-time hire, and suddenly, you’re navigating payroll in a new state. Each of those changes adds complexity to your books. And under an hourly model, every added layer of complexity translates directly into a bigger bill.

The real problem isn’t the cost itself — it’s the unpredictability. When you can’t reliably forecast your bookkeeping costs, they become noise in your financial planning. You start making overhead decisions based on a number that shifts month to month. And when you’re trying to model whether you can afford that next hire or take on a lower-margin engagement, noise is the last thing you need.

There’s also an incentive misalignment worth naming. Under an hourly model, efficiency isn’t rewarded. A faster bookkeeper earns less. That’s nobody’s fault — it’s just how the structure works. But it means you and your bookkeeper aren’t necessarily pulling in the same direction.

The Case for Fixed-Fee Bookkeeping

Fixed-fee bookkeeping flips the dynamic. You pay a set amount — typically weekly or monthly — tied to the scope and complexity of your books, not the clock. Your bookkeeper is now incentivised to be efficient, because their fee doesn’t change whether a task takes them two hours or five.

For a growing consulting firm, this matters in a few specific ways. First, your monthly overhead becomes predictable. You know what bookkeeping costs. You can build around it. Second, when you call with a question or ask for a quick report, you’re not quietly watching the meter tick. The relationship changes. It becomes less transactional and more collaborative.

System Six operates on a fixed weekly fee model with no long-term contracts — a combination that’s rarer than it should be. The no-contract piece is important. It reflects a straightforward premise: the firm should earn your continued business by consistently delivering value, not by locking you into an agreement. Hourly billing is reserved for one-time project work like system onboarding, cleanups, or implementation — situations where the scope is genuinely variable and time-based billing makes sense. For ongoing recurring work, the fee is fixed.

With a 9.5 out of 10 NPS across 175+ clients and a US-based team averaging more than 10 years of accounting experience, that model clearly resonates. Clients aren’t staying because they have to. They’re staying because it works.

The Scalability Question Nobody Asks Early Enough

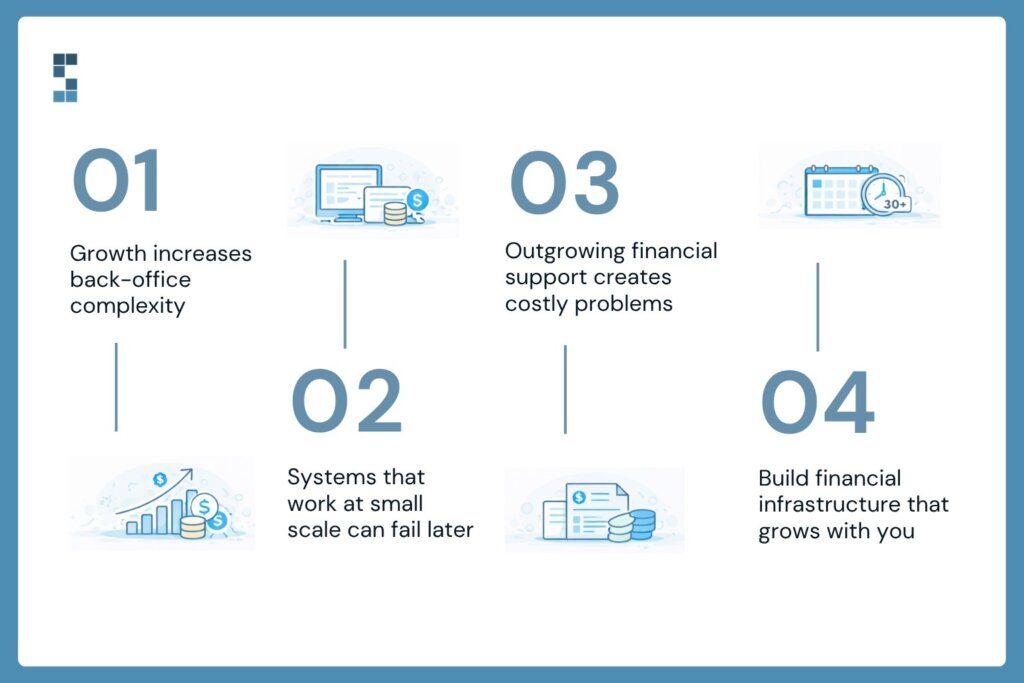

Most firm owners choose an engagement model based on their current situation. That’s understandable. But the smarter question is whether the model holds up when you’re twice the size you are today.

Think about what scaling actually means for a consulting firm’s back office. More clients mean more invoicing cycles. More staff means payroll across potentially multiple states, each with its own compliance requirements. A bigger operation means more vendor relationships, more expense categorisation, and more month-end complexity. The financial infrastructure that served you at $900K in revenue isn’t automatically equipped to serve you at $2.5M.

Manish G., a client who learned this the hard way, described what happened when he relied on a freelance bookkeeper who couldn’t keep up with the firm’s growth: “Most of our payroll taxes were filed incorrectly, and there was no easy way for a non-expert to figure out how to solve that mess.” Rebuilding from that — fixing misfiled taxes, restoring vendor relationships, regaining employee trust — took time and money that should have been spent growing the business.

A flexible bookkeeping engagement isn’t just about price structure. It’s about working with a partner whose service scope can expand alongside yours — from core bookkeeping to payroll processing, bill pay, cash flow forecasting, and financial reporting — without forcing you to switch providers every time you hit a new growth threshold. The goal is infrastructure that grows with you, not infrastructure you outgrow.

A Simple Way to Think About the Decision

So which model is right for your firm? Here’s a practical way to frame it.

Hourly billing probably makes sense if you’re pre-revenue, running genuinely minimal books with very few monthly transactions, or if you need a one-time project — a cleanup, a system migration, an onboarding process. For defined, bounded, variable-scope work, time-based billing is fair.

Fixed-fee billing makes more sense the moment your financial operations become consistent and ongoing. If you have regular payroll, monthly close, recurring invoicing, and any meaningful transaction volume, a fixed fee gives you what you actually need: cost certainty, aligned incentives, and a predictable line item in your operating budget.

One more thing worth considering: the no-contract piece. One of the most common objections to switching financial providers is the perceived switching cost — the disruption of changing systems and relationships. A fixed-fee model with no long-term contract removes that friction almost entirely. You’re not locked in. You can leave if it stops working. That changes the risk calculus significantly.

If your firm has grown since you set up your current bookkeeping arrangement and you’re still on hourly, it’s worth doing the math. Add up your last six months of bookkeeping invoices, average them, and ask yourself: Would a fixed monthly fee in that range feel more manageable? For most growing firms, the answer is yes — and the predictability alone is worth the switch.

Your Bookkeeping Setup Is Infrastructure

Think of your engagement model the way you’d think about your project management software or your CRM. It’s not glamorous, but it shapes how everything else runs. Infrastructure built for where you are today is fine — until it isn’t. The firms that scale smoothly are the ones that think about this before they hit the wall, not after.

The model that fits your firm at $800K in revenue probably isn’t the one that serves you at $3M. The question is whether you’re going to figure that out proactively — or on a Tuesday morning when an invoice shows up and it’s $380 more than you expected.

What would it mean for your firm to know, exactly, what bookkeeping costs every month — and to trust that the number won’t change unless your needs do?

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialise in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Mar 23, 2026 | Blog

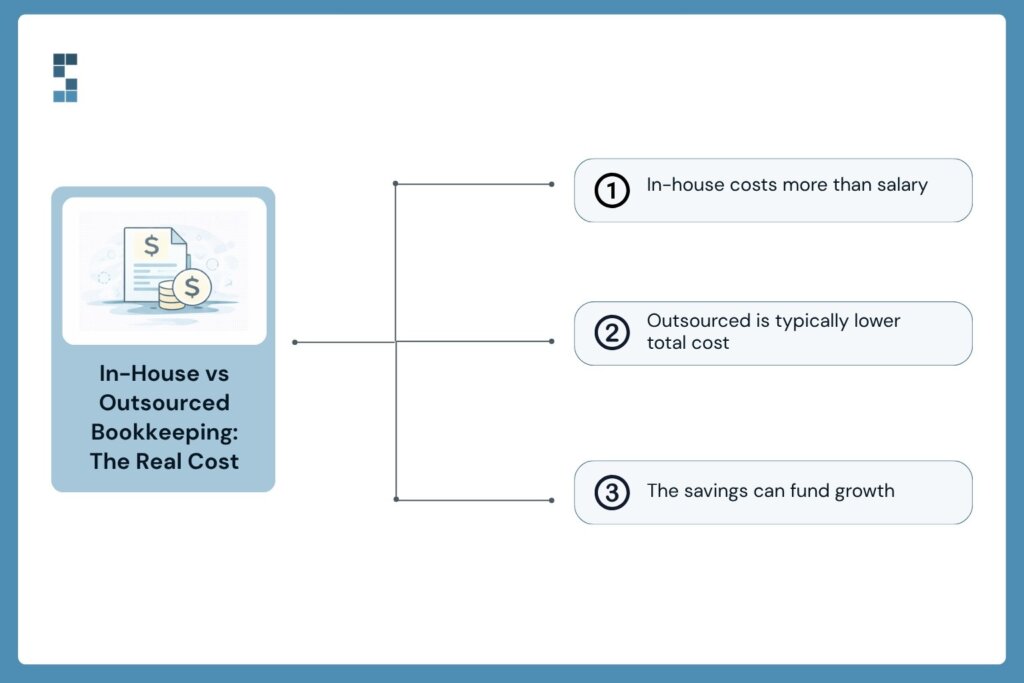

Elena thought she was being smart. She’d just hired her first in-house bookkeeper — $50,000 salary, tidy desk by the window, problem solved. Six months later, she sat across from her accountant, staring at a number that didn’t add up. What she’d budgeted for and what she was actually spending were two different things entirely.

Sound familiar? The in-house vs. outsourced bookkeeping debate sounds straightforward. You put a salary on one side, a monthly fee on the other, and pick the smaller number. But that math is missing most of the equation. The real cost of in-house bookkeeping isn’t the salary line — it’s everything underneath it.

Let’s run the actual numbers.

The Comparison Most People Make — and Why It’s Incomplete

Here’s how the typical thought process goes: a bookkeeper costs $50,000 a year. An outsourced service costs $1,500 a month, or $18,000 a year. In-house wins by $32,000. Done.

Except that’s not remotely how it works. The $50,000 salary is just the starting point. What gets added to it — quietly, incrementally — is where the real cost lies. And for a 10 to 50-person consulting firm, those additions can push a $50K hire well past $75,000 before the person has filed their first reconciliation.

The outsourced fee, meanwhile, is the fee. No surprises. No add-ons. Just a fixed, predictable number every month.

The True Cost of an In-House Bookkeeper

Start with payroll taxes. Employers pay 7.65% in FICA on top of every salary — that’s $3,825 on a $50K base, before anything else. Then add health insurance. Depending on your plan, employer contributions typically run $5,000 to $8,000 per year for a single employee. Paid time off — two weeks of vacation plus federal holidays — adds another $2,000 to $3,000 in salary cost for days not worked.

Now layer in recruiting. Hiring a bookkeeper takes time and often money. Job board listings, hours spent reviewing resumes, interview rounds, potential recruiter fees — it’s not unusual for a hire to cost $3,000 to $5,000 before the first day of work. And if the hire doesn’t stick? You run that process again.

There’s also software. Your bookkeeper needs a license for your accounting platform, possibly for expense management tools, and for payroll software if they’re handling that too. Add $1,500 to $3,000 annually.

Then there’s the management overhead that nobody budgets for: onboarding time, training, answering questions, reviewing work, and handling performance issues. For an owner or office manager already stretched thin, supervising a direct report is a real-time cost, and for a consulting firm owner, it isn’t free.

Add it all up. A $50,000 bookkeeper realistically costs $68,000 to $80,000 per year once you factor in taxes, benefits, PTO, recruiting, software, and management time. That’s not a worst-case scenario. That’s just the math.

What Outsourcing Actually Costs — and What You Get

For a consulting firm with $1M to $5M in revenue, outsourced bookkeeping typically costs $10,000 to $25,000 per year, depending on the scope of services. That covers bookkeeping, payroll processing, financial reporting, and compliance support — often more than a single in-house hire would handle anyway.

There’s no employer tax. No benefits package. No recruiting cycle. No software licenses. No management overhead. The monthly fee is the monthly fee.

And when your bookkeeper goes on vacation — or quits — you don’t scramble. With a firm like System Six, you get a full team behind your account, not a single person whose absence brings your financial operations to a halt.

Manish G., a business owner who learned this the hard way, described what happened when he went the solo-contractor route: payroll taxes filed incorrectly, invoicing falling apart when the contractor left, and no one left to process payroll. “If you’re thinking about going the cheap route with a freelancer,” he said, “it is likely to hurt you in the long term.” He found System Six after that experience and didn’t look back.

The Side-by-Side You Actually Need to See

Let’s put real numbers next to each other. In-house bookkeeper: $50,000 salary, plus $3,825 payroll taxes, plus $7,000 health insurance, plus $2,500 PTO, plus $4,000 recruiting, plus $2,000 software, plus management time. Conservative total: $69,000 to $80,000 per year.

Outsourced bookkeeping: $10,000 to $25,000 per year, all-in.

The gap is $44,000 to $70,000 annually. That’s not a rounding error. For a 15-person consulting firm, that delta could fund a business development role, a marketing push, or be retained as margin.

But here’s what the numbers still don’t fully capture: depth of expertise. A single in-house hire brings one person’s knowledge. A good outsourced partner brings a team — experienced bookkeepers, controllers, compliance specialists — all available without the overhead of employing them.

Ann D., a business owner in Seattle, put it this way: “I found the right level of service at the right price. I own a business and can delegate all bookkeeping, payables, receivables, tax preparation, projected budgeting, and monthly financial reporting over to them. I don’t want to run my business without them.”

The Cost You’re Probably Not Counting: Your Own Time

For many consulting firm owners, the bookkeeper decision is moot — because they’re the bookkeeper. They’re the ones reconciling accounts on Sunday nights. They’re the backup when something goes wrong. They’re the person who gets cc’d on every financial question, even when they’d rather be doing literally anything else.

At $200 to $300 an hour — a conservative estimate for most consulting principals — even 10 hours a month spent on financial oversight represents $2,000 to $3,000 in opportunity cost, per month. That’s $24,000 to $36,000 a year in time you’re spending on bookkeeping instead of client work, business development, or growth.

John D., a small business owner who was skeptical about outsourcing before he tried it, admitted he didn’t think he needed the help. He “somewhat skeptically” made the move to System Six — and was “incredibly glad” he did. The skepticism is understandable. The math, once you look at it honestly, usually isn’t.

The Real Question

The question was never whether you can afford to outsource bookkeeping. Once you run the true cost analysis — salary fully loaded, turnover risk, management time, your own hours — the question flips. Can you afford not to?

For consulting firms spending $1,500 to $2,000 a month on outsourced services and getting back their Sundays, their peace of mind, and a team of experts instead of a single point of failure, the ROI isn’t even close.

If you’ve been doing the math on in-house vs. outsourced and something still isn’t adding up, it might be time to run the complete numbers. System Six works with consulting firms exactly like yours — fixed weekly pricing, no long-term contracts, and a US-based team that already knows your industry. The conversation is free. The spreadsheet might surprise you.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Mar 17, 2026 | Blog

David stared at his bookkeeping invoice for a long moment. Forty-three hundred dollars. He ran a 14-person management consulting firm, and the business was doing fine, but every month that number nagged at him. Was he paying for someone to keep the lights on? Or was there a real return buried somewhere in those spreadsheets?

Here’s the thing: David wasn’t asking the wrong question. He was calculating the wrong way.

Most consulting firm owners evaluate bookkeeping the same way they’d evaluate a coffee subscription, as a flat monthly cost to be tolerated or negotiated down. But that framing misses almost everything that matters. When you learn to measure the true ROI of your bookkeeping investment, the math tends to look very different from what you expected. Usually better. Sometimes dramatically so.

So let’s do the math. Properly.

Stop Counting What You Pay. Start Counting What You Lose.

The invoice is the easy number. What’s harder to see — but far more expensive — are the costs hidden beneath your current approach to financial management.

The first hidden cost is time. Take an honest look at how many hours per month you personally spend on financial tasks: reviewing reports, chasing down receipts, reconciling accounts, answering questions from your bookkeeper, and preparing for tax season. Now multiply that by your effective hourly rate. If you’re billing clients at $250 an hour and spending 15 hours a month on financial admin, that’s $3,750 in opportunity cost — every single month. That’s $45,000 a year in time that isn’t going toward client work or business development.

The second hidden cost is errors. They’re sneaky. One System Six client was unknowingly paying $700 a month in unnecessary bank fees because poor cash flow tracking kept triggering overdraft thresholds. That’s $8,400 a year — enough to fund a solid bookkeeping engagement with money left over. The painful part? He had no idea it was happening. You can’t catch what you can’t see.

The third cost is the hardest to quantify but often the most expensive: missed growth opportunities. Consider a consulting firm that gets the chance to take on a $200,000 contract — their biggest ever. The project requires detailed milestone billing, multi-phase budget management, and financial reporting that their existing systems can’t handle. So they pass. That’s not just lost revenue. It’s lost momentum, lost credibility, and a ceiling they didn’t know they’d built for themselves.

Add those three categories together before you start complaining about your bookkeeping bill.

The ROI Formula That Actually Works

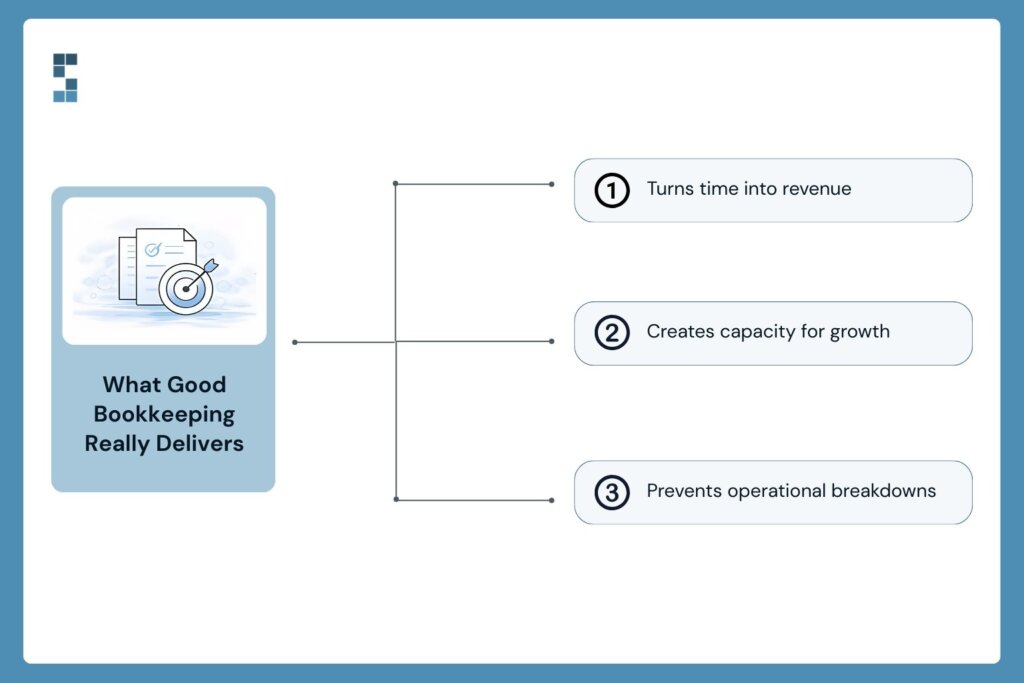

True ROI isn’t just about what you pay. It’s about what you gain, what you save, and what you stop losing. Here’s a simple framework with three components.

Component one: direct cost savings. This is time and operational efficiency. When you stop doing manual invoice creation, account reconciliation, and expense categorization yourself, you recover hours — and those hours have a dollar value. Calculate it based on your own rate, not some abstract concept of ‘time saved.’

Component two: risk mitigation value. What’s the cost of the errors and penalties you avoid? A missed payroll tax deadline triggers automatic fines plus interest. A simple bookkeeping error compounds quietly for months. Professional, consistent financial management dramatically reduces the probability of these events.

Component three: growth enablement value. This is the one most firms miss entirely. Better financial infrastructure doesn’t just save time today — it unlocks revenue that wasn’t accessible yesterday.

Here’s what this looks like in practice. A strategy consulting firm was spending 20 hours a month on financial administration. At the owner’s $200 hourly rate, that’s $4,000 a month in opportunity cost. After systematizing their financial processes, that dropped to 3 hours of reviewing automated reports — a $600 monthly time investment. They were paying $800 a month for the service. The math: $3,400 in recovered time, minus $800 in cost, equals a 325% return on investment. And that’s before accounting for the compliance errors they stopped making or the larger clients they could now serve.

The break-even point for a well-designed bookkeeping engagement is typically 2 to 3 months. After that, you’re in positive territory — and the returns compound.

What Good Bookkeeping Actually Unlocks

Numbers are one thing. But the people who’ve lived this tend to describe it differently.

Betsy, a System Six client who runs an investor-backed business, put it this way: “System Six has done wonders for my stress level to feel like this is all now taken care of with a professional partner.” That’s not an accounting outcome. That’s cognitive bandwidth returned — energy quietly consumed by worry, now redirected toward the work that actually matters.

Manish G., another client, was even more direct. After a freelance bookkeeper left his accounts in disarray — payroll taxes filed incorrectly, invoicing halted, operations on the edge of collapse — he turned to System Six. He later wrote: “I can’t begin to describe how thankful I am… they have literally saved my business from falling into operational ruins.” He also noted something that gets to the heart of the ROI question: “I would pay for this expertise without hesitation, given the pricing is so fair for the value.”

That last part is worth sitting with. When the value is real and visible, the cost stops feeling like a cost.

What does that look like in practice for a growing consulting firm? It means you can take on bigger clients because your financial infrastructure can handle the complexity. It means you stop passing on opportunities because your reporting can’t keep up. It means that 15 hours a month you used to spend hunched over QuickBooks becomes 15 hours of business development, strategic thinking, or simply leaving the office before 7 pm.

One extra client meeting per week, made possible by reclaimed time, can translate into tens of thousands of dollars in additional annual revenue. The bookkeeping investment doesn’t just pay for itself — it starts funding growth.

The Only Number That Actually Matters

Here’s the reframe: bookkeeping isn’t a cost center. It’s an investment with a measurable return — one most firms have never actually sat down to calculate.

If you’re paying $800 a month for a service that saves you $3,400 in time, prevents $700 in monthly errors, and positions you to take on clients you couldn’t have handled before, you’re not spending money. You’re multiplying it.

The firms that struggle with this question are usually those that’ve never done an audit. They don’t know how many hours they’re spending. They haven’t added up the bank fees, the penalty notices, the hours their office manager spends chasing down receipts. They’re measuring the invoice and ignoring everything else.

So before you decide whether your bookkeeping investment is worth it, figure out what your financial admin is actually costing you right now. That’s the first number you need. And for most consulting firm owners, it’s the number that changes everything.

What could your firm do with 15 extra hours a month and complete clarity on your cash flow? That’s not a rhetorical question. It’s your ROI calculation waiting to be filled in.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

by Chris Williams | Mar 9, 2026 | Blog

Elena had been talking about automating her books for eight months. She finally pulled the trigger in January, connected her bank feed, and waited. By February, she was still manually correcting misfiled transactions, and her bookkeeper was still spending hours every week cleaning things up. She felt cheated. “Wasn’t this supposed to save time?”

It was. It will. But nobody told Elena that automation implementation isn’t an event — it’s a process. And without a clear picture of what that process actually looks like, many consulting firm owners either give up too early or set themselves up for frustration right out of the gate.

Here’s the honest timeline. No hype, no hand-waving. Just what to expect, week by week, as you transition your financial systems from manual to automated.

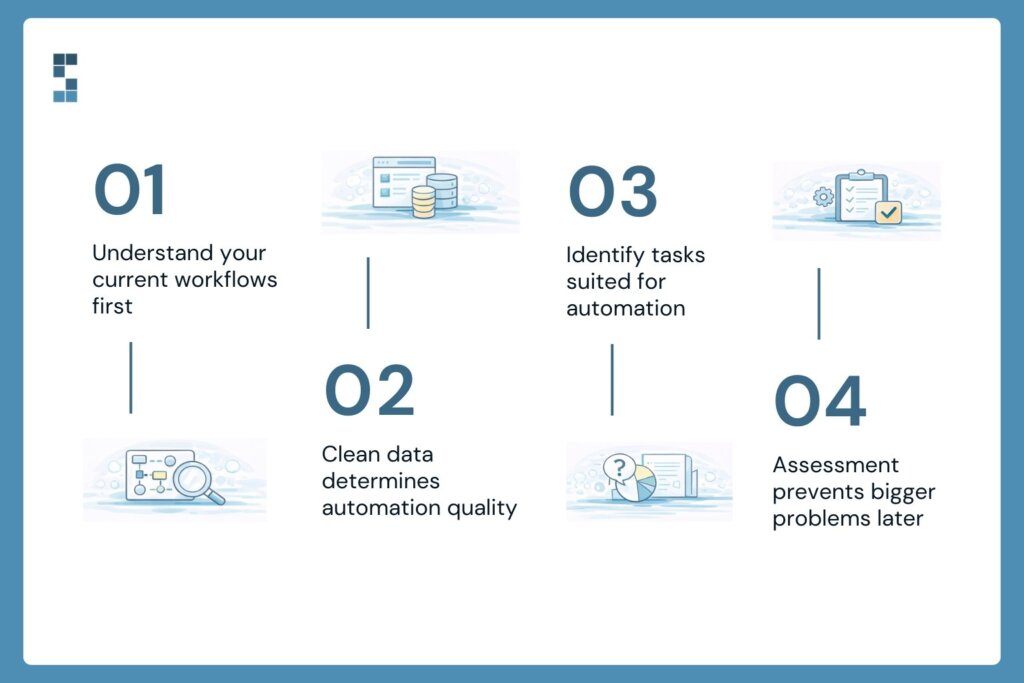

Before You Touch a Single Tool: The Assessment Phase (Weeks 1–2)

Everyone wants to skip this part. Don’t.

Before any automation implementation can work, you need a clear map of what you’re actually doing right now. Where does your money come from? How do transactions enter your system? What categories do you use, and are they consistent? What software are you already running — QuickBooks, Gusto, a payroll processor, a time tracker?

This isn’t glamorous work. It feels like measuring twice before cutting. But here’s why it matters: automated systems learn from your existing data. If that data is messy — inconsistent categories, duplicate vendors, a chart of accounts that grew organically over five years — the automation inherits the mess. Garbage in, garbage out.

Most consulting firms spend one to two weeks here. You’re documenting your current workflows, identifying which processes are good candidates for automation (hint: anything repetitive and rule-based), and figuring out where the real time drains are. The payoff isn’t immediate, but this phase prevents weeks of backtracking later.

Weeks 1–4: Foundation First

This is when things start to feel real—and when expectations tend to collide with reality.

Bank feeds connect. Categorization rules go in. Payroll integrations link up to your accounting platform. Invoicing workflows get templated. If you’re migrating to a new system entirely, data from the old one starts flowing over.

Expect hiccups. A transaction is assigned to the wrong category. A vendor gets duplicated. A bank feed throws an error because of a password change you forgot about. This is completely normal. The system is learning your business, and so are you. The goal in this phase isn’t perfection — it’s establishing a reliable foundation you can build on.

One thing that makes this phase significantly smoother is expert implementation support. As one System Six client put it: “They take on the entire setup and effectively act as consultants until your accounting operations are running like a well-oiled machine.” That’s the difference between spending four weeks troubleshooting alone and having someone who’s done this for 175+ clients guide you through it.

By the end of week four, your basic financial workflows should be running automatically in the background. You’re not done — but you’re off manual life support.

Weeks 5–12: The System Learns, So Do You

This is the phase nobody talks about, and it’s honestly the most interesting one.

Automation gets smarter as it accumulates transaction history. Categorization accuracy climbs. The system starts recognizing patterns — this vendor always goes to software, that one always goes to travel — and the exceptions you’re manually correcting get fewer every week. Your financial reports are starting to click into place. Real-time dashboards stop feeling like a promise and become a tool.

Your role shifts, too. You move from doing to reviewing. Instead of entering data, you’re checking that the automated system entered it correctly. Instead of building reports, you’re reading them. That’s a fundamentally different relationship with your finances — and a much better use of a consulting firm owner’s time.

There’s a common fear in this phase: “What if I’m doing it wrong?” It’s worth naming directly. The answer is that small errors now are far less costly than the hours you’ve been spending on manual work. If a category is wrong, you fix the rule and move forward. Automation doesn’t demand perfection on day one. It improves incrementally, and so does your confidence with it.

“System Six has done wonders for my stress level,” says Betsy, a System Six client. “I feel like this is all now taken care of with a professional partner.” That feeling — that background hum of financial anxiety going quiet — tends to arrive somewhere in this phase, once the systems have had enough time to prove themselves.

90 Days In: What Your Mornings Look Like Now

Picture a Monday morning three months from now. You open your laptop, pull up your financial dashboard, and spend fifteen minutes reviewing what the system surfaced over the past week. A flagged transaction. An overdue invoice. A cash flow note your bookkeeper left. Then you close the laptop and run your business.

That’s not a fantasy. It’s what properly implemented financial automation actually delivers. Most consulting firms hit a 70–80% reduction in financial management time within ninety days of going live. The hours that used to disappear into receipt sorting, manual reconciliation, and spreadsheet updates get redirected to client work, business development, or — novel concept — not working on weekends.

The math compounds fast. If you’re currently spending fifteen hours a month on financial administration — a conservative estimate for most firms in the $1M–$5M range — that’s 180 hours a year. At a $200 consulting rate, you’re looking at $36,000 in time that could be generating revenue instead of reconciling bank statements.

Paul, a System Six client, put it plainly: “I told people that hiring them was the best decision I made at the start of the business. They’ve crushed it. Not only have they been mistake-free, but they’ve been proactive at catching mistakes I’ve made and seeing challenges coming down the pike.”

That’s the real payoff. Not just time back. Better information, fewer errors, and a financial partner who’s watching your numbers so you don’t have to.

Three Months Is a Short Trade for Years of Time Back

The timeline from start to fully humming automation is roughly ninety days. Two weeks of assessment. Four weeks building the foundation. Six weeks of system learning, and you’re learning with it. That’s it.

Three months can feel like a long time when you’re in the middle of running a consulting firm. But measure it against what comes after: a financial system that runs in the background, books that are always current, and Monday mornings that start with a fifteen-minute review instead of a four-hour catch-up session. Measured that way, ninety days is a very reasonable price.

The firms that make this transition successfully tend to have one thing in common: they don’t try to do it alone. The difference between a smooth automation implementation and a frustrating one almost always comes down to expert setup — someone who knows which pitfalls to avoid, which integrations actually work, and how to configure the system for a consulting firm specifically.

If you’re sitting there wondering what your first step looks like, start with that assessment. Map your current processes. Find out where the time is really going. And if you’d like a partner who’s done this for over 175 consulting firms and counting, System Six would be glad to walk you through it.

About System Six

System Six is a Seattle-based bookkeeping and financial services firm that helps small and mid-sized businesses streamline their financial operations. We specialize in providing technology-driven financial management solutions for consulting firms, enabling owners to focus on growing their businesses without worrying about cash flow, payroll, or compliance. Our team of over 40 professionals brings an average of 10+ years of accounting experience to every client relationship, serving more than 175 businesses across the U.S. With a 9.5/10 NPS score, we deliver the financial clarity and peace of mind that consulting firm owners need to thrive. Learn more at www.systemsix.com.

Page 2 of 12«12345...10...»Last »