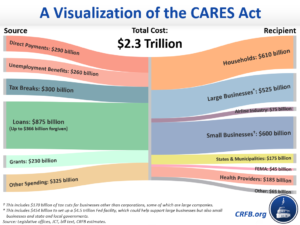

In March our elected leaders finalized the largest package of stimulus/financial aid/disaster recovery in American history. Known as the CARES Act (Coronavirus Aid, Relief, and Economic Security) it contains a staggering 800+ pages of legislation to review, understand, and begin applying to our small business and personal lives. NPR, the NYT, and Forbes all have good summary articles to read-up on. Want to see where the 2.3 trillion-dollar stimulus comes from and how it will be spent? The Committee for a Responsible Federal Budget has an excellent article here explaining this graphic.

In March our elected leaders finalized the largest package of stimulus/financial aid/disaster recovery in American history. Known as the CARES Act (Coronavirus Aid, Relief, and Economic Security) it contains a staggering 800+ pages of legislation to review, understand, and begin applying to our small business and personal lives. NPR, the NYT, and Forbes all have good summary articles to read-up on. Want to see where the 2.3 trillion-dollar stimulus comes from and how it will be spent? The Committee for a Responsible Federal Budget has an excellent article here explaining this graphic.

#1 – To Loan or Not to Loan?

While the SBA loans (EIDL and PPP) are good options to help businesses with emergency funding (if the SBA and banks can get to processing the applications!) one thing to keep in mind is that these are loans and not just free money. While some of the PPP or EIDL funds might be forgiven, we’d encourage clients to ask the question, “Will taking out a loan help continue an already viable business?” Considering failure is never a popular recommendation and is the opposite of the entrepreneurial desire to persevere.

That said, the C19 crisis could be a reasonable time to ask the question, “Will these funds help get us through a few tough months, or will they just delay the inevitable fact that the business needs to close?” If the business or its owners had very little in savings or positive cashflow before the crisis, will an emergency loan change that or just add debt to what wasn’t a healthy business before the crisis? If after asking that question the answer is a resounding, “YES, the business is viable and just needs some funds (and strategy) to help weather the storm,” then by all means, proceed to apply for the PPP and/or EIDL if you haven’t already.

#2 – Your Options

EIDL (Economic Injury Disaster Loan)

Read more about and apply for the EIDL loan here. The SBA has streamlined the process, and added an option to apply for an emergency $10,000 advance that is available within three days of applying for an EIDL. To access the advance, you must first apply for an EIDL and then request the advance. The advance does not need to be repaid.

PPP (Paycheck Protection Program) Loan

The PPP is getting a lot of attention right now and is shaping-up to be one of the best ways for small businesses to access money quickly with a possibility for forgiveness on a portion of the loan. There are some great resources we recommend you read to get a better understanding of the loan.

- The SBA may forgive some part of the PPP loans if certain criteria are met, like all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities.

- The PPP will provide eligible applicants (including non-profits, sole proprietors, self-employed individuals and independent contractors) with loans to cover costs related to payroll expenses, group health care benefits, utilities, rent, mortgage interest payments, and interest on other debt incurred prior to 02/15/2020. It excludes funds for working capital, renovations, equipment, and inventory purchases.

- There are a few web pages with more specifics on the PPP loan and the process for applying. Here are the links we’ve found most helpful. You can quickly read and determine if your business is eligible to apply:

- Contact your banker. Your banker is going to play an important role in obtaining the PPP loan. Many banks are prioritizing existing clients over working with new clients. If you need an introduction to a small business banker, we have a short list of three amazing bankers we’d be happy to introduce you to.

- Gather Supporting Documentation. Several bankers we work closely with have been advising that the following information will most likely be needed along with the PPP application:

- Detailed monthly/annual payroll data and reports for all 12 months of 2019 and possibly the first three months of 2020.

- Copies of 941 payroll tax returns filed with the IRS for the entire year of 2019 and first quarter of 2020 (if available.)

- Documentation reflecting the health insurance premiums paid by the business under a group health plan.

- Documentation of all retirement plan funding paid for by the business for the past 12 months.

- A number of payroll providers say they are working on a single report to help make this easier to access all in one place. We recommend you go to work with your payroll, health insurance, and 401k providers as needed. If System Six processes your payroll, reach out to us and we’ll work to help you gather the payroll reports needed.

#3 – Understanding Loan Forgiveness

PPP Loan Forgiveness

If you were fortunate enough to have received a PPP loan, congratulations! Now that the celebration has worn off, you’re likely in the weeds trying to figure out how to ensure your business receives as much loan forgiveness as possible. While we are learning that it’s tricky and can be complex, we still think the best way forward is to not despair and for each business owner to simply do our best to follow the intention of the PPP program while waiting for guidance to get clearer. Even if all of the loan isn’t forgiven, a 1% interest rate loan is a very helpful tool for us to get our businesses back on track.

Know that the AICPA (American Institute of Certified Public Accountants) and dozens of other groups are working hard to gain further clarity on how PPP loan forgiveness works and to also try and relax the forgiveness requirements.

Top PPP Forgiveness Strategies (as of 5/8/2020):

- Understand the general rules around the PPP loan and how forgiveness works. Do the following within 8 weeks of the PPP loan being deposited to your account:

- Spend at least 75% of the PPP loan amount on payroll costs

- Spend no more than 25% of the PPP loan amount on rent, utilities, and interest

- Restore employee headcount (FTE) back to at least 75% of what it was pre-crisis

- Restore employee payroll back to at least 75% of what it was pre-crisis

- Read a few blog posts from an excellent Seattle area tax-preparing CPA we know and trust

- If you want to nerd-out like we bookkeepers and accountants do, you can also check out the more detailed AICPA “PPP Application and Forgiveness Processes”

- If using a payroll processor like Gusto, reference their helpful PPP forgiveness report. It does most of the heavy calculations needed regarding payroll expenses and potential forgiveness.